Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

ExpertSpotlight: The History of Labor Day

What began as a modest parade in New York City has grown into a national holiday that honors the contributions of American workers and continues to spark conversations about labor rights today. Observed on the first Monday of September, Labor Day is both a tribute to the workforce and a cultural milestone marking the close of summer. From Parade to Holiday The first Labor Day celebration took place on September 5, 1882, when roughly 10,000 workers marched through New York City in a demonstration organized by the Central Labor Union. The parade, followed by a picnic and speeches, was designed to showcase the unity and strength of trade and labor organizations. The origins of the idea remain contested. Some credit Peter J. McGuire, co-founder of the United Brotherhood of Carpenters, while others point to Matthew Maguire, a machinist and secretary of the Central Labor Union. Regardless of its champion, the concept spread quickly. By the late 1880s, states began adopting Labor Day as an official holiday. In 1894, following a wave of labor unrest that included the Pullman Strike, President Grover Cleveland signed legislation declaring the first Monday in September a federal holiday. Labor Day vs. May Day Unlike May Day (May 1)—which became closely associated with international labor movements and the more radical legacy of the Haymarket Affair of 1886—Labor Day was intended as a uniquely American holiday. Its September placement emphasized unity and recognition without the confrontational overtones of May Day. Over time, this distinction gave Labor Day a broader cultural resonance in the United States. A Living Tradition While barbecues, parades, and retail sales now dominate many Labor Day weekends, the holiday’s deeper meaning endures. It is a reminder of the hard-won gains of the labor movement, from the eight-hour workday to workplace safety protections, as well as the continuing debates over wages, unionization, and economic fairness. Even traditions like the etiquette rule of not wearing white after Labor Day reflect how the holiday shaped cultural norms at the turn of the 20th century. Today, beyond its role as summer’s unofficial finale, Labor Day continues to honor the dignity and achievements of working people across the country. Connect with our experts about the History of Labor Day. Check out our experts here : www.expertfile.com

MSU team develops scalable climate solutions for agricultural carbon markets

Why this matters: Builds trust in carbon markets. This science-based baseline system dramatically improves accuracy, helping ensure carbon credits are credible and truly reflect climate benefits. Enables real climate impact by accounting for both soil carbon and nitrous oxide emissions, the approach delivers a full, net climate assessment. Scales across millions of acres. Tested on 46 million hectares in 12 Midwest states, this approach is ready for large-scale adoption, helping farmers transition to regenerative practices with confidence and clarity. New research from Michigan State University, led by agricultural systems scientist Bruno Basso, addresses a major problem in agricultural carbon markets: how to set an accurate starting point, or “baseline,” for measuring climate benefits. Most current systems use fixed baselines that don’t account for the soil carbon changes and emissions that would occur if business-as-usual practices were maintained on fields. Such inaccuracies can distort carbon credit calculations and undermine market trust. “The choice of baseline can dramatically influence carbon credit generation; if the model is inaccurate, too many or too few credits may be issued, calling market legitimacy into question,” said Basso, a John A. Hannah Distinguished Professor in the Department of Earth and Environmental Sciences, the Department of Plant, Soil and Microbial Sciences and the W.K. Kellogg Biological Station at MSU. “Our dynamic baseline approach provides flexible scenarios that capture the comparative climate impacts of soil organic carbon, or SOC, sequestration and nitrous oxide emissions from business-as-usual practices and the new regenerative system.” The research, published in the journal Scientific Reports, covers 46 million hectares of cropland across the U.S. Midwest, provides carbon market stakeholders with a scalable, scientifically robust crediting framework. It offers both the investment-grade credibility and operational simplicity needed to expand regenerative agriculture. Regenerative agriculture and carbon markets Regenerative agriculture includes practices like cover cropping, reduced or no tillage, diversified rotations, adaptive grazing and agroforestry. These methods restore soil health, enhance biodiversity, increase system resilience and help mitigate climate change by building SOC and reducing greenhouse gas emissions. Carbon markets offer a promising financial mechanism to accelerate regenerative transitions. By compensating farmers for verified climate benefits, they can act as either offset markets (for external buyers) or inset markets (within agricultural supply chains). However, the integrity of these markets hinges on reliable, science-based measurement, reporting and verification systems that integrate modeling, field data and remote sensing. A breakthrough multi-model ensemble approach To overcome limitations in traditional modeling, the MSU scientists and colleagues from different institutions in the U.S. and Europe deployed a multi-model ensemble, or MME, framework, using eight validated crop and biogeochemical models across 40,000 locations in 934 counties spanning 12 Midwestern states. The MME avoids model selection bias, lowering uncertainty in soil carbon predictions from 99% (with single models) to just 36% (with the MME). “This is a game changer for carbon markets,” said Basso. “It delivers a level of accuracy and scalability — from individual fields to entire regions — that current systems lack.” The MME platform also enables the creation of precalculated, practice-based dynamic baselines, reducing the burden of data collection and easing participation for producers. Improved mitigation assessments Unlike many approaches that consider only SOC, the MSU lead team’s study evaluates both SOC sequestration and nitrous oxide emissions to determine net climate impact. “This comprehensive assessment ensures that carbon credits represent true climate mitigation,” said Tommaso Tadiello, postdoctoral fellow in MSU’s Department of Earth and Environmental Sciences and co-author of the study. “A practice that increases soil carbon may improve soil health,” added Basso, “but it may not deliver actual climate benefits if it simultaneously increases nitrous oxide emissions. Our method provides a full accounting of the net climate effect.” The research team found that the combination of no-till and cover cropping delivered an average net mitigation of 1.2 metric tons of carbon dioxide-equivalent per hectare annually, potentially abating 16.4 teragrams of carbon dioxide-equivalent across the study area. This research was supported by the Michigan Department of Agriculture and Rural Development, U.S. Department of Energy’s Great Lakes Bioenergy Research Center, National Science Foundation Long-Term Ecological Research, Builders Initiative, The Soil Inventory Project, Generation IM Foundation, Walton Family Foundation, Morgan Stanley Sustainable Solutions Collaborative and MSU AgBioResearch.

Inflation: It’s Not Just for Prices Anymore

Lately, headlines are full of talk about inflation — a response to the economy and the looming tariffs. I’ve experienced many inflationary periods, but it feels different in retirement. When I was earning a paycheque, inflation was just an annoyance, something I needed to pay attention to and maybe buy a cheaper cut of steak. Now, as someone on a “fixed income,” it feels like a real threat. Recently, Ben McCabe, CEO of Bloom Financial, appeared on Breakfast Television and delivered a truth bomb: “We’re approaching a perfect storm. Longer life expectancy, fewer defined benefit pensions, and rising inflation.” Well, that storm has arrived — and it’s inflating more than just prices. It’s also expanding our waistlines, prescription lists, and emotional baggage. Inflation, at its core, means “the condition of being inflated.” And it turns out that definition applies to more than the grocery bill. So, grab a cup of green tea (or a celery stick if you’re feeling virtuous). Let’s explore the three sneaky forms of inflation threatening your retirement — and what you can do about them. This blog will appeal to individuals who have retired or aspire to retire in the future. Let’s light this candle! 1. Financial Inflation: The Usual Suspect Let’s start with the obvious: inflation means your money won’t stretch as far as it used to. In 2022, Canada’s Consumer Price Index increased by 6.8% — the highest rise in 40 years. Although it slowed down a bit in 2023, essentials such as food, rent, and fuel continue to grow. Your retirement income might be fixed, but prices definitely aren’t. Retirement Risks from Financial Inflation: • Longer lives mean longer bills. A 65-year-old woman today has a 50% chance of living past 90 years old. That’s over 25 years of expenses. • Vanishing pensions. Defined benefit pensions are disappearing faster than good manners on Twitter. • Healthcare creep. Public healthcare doesn’t cover everything, especially if you want care that wasn’t designed in 1978. As Ben McCabe aptly put it: “We need to stay healthy so our health span matches our lifespan,” huh?— “otherwise, inflation will affect us through the cost of medications, home care, and long-term care facilities.” What You Can Do: • Review your income sources. Prioritize indexed income sources, such as CPP, OAS, and annuities with COLA (Cost of Living Adjustment) riders. • Use home equity sensibly. If you’re house-rich but cash-poor, consider a reverse mortgage or other equity release products. • Adjust your spending habits. Host themed nights, like “Tuna Tuesdays” — a nostalgic, fun, and budget-friendly option. How to Support Others: • Discuss money matters with kindness. Many retirees feel ashamed of their finances. Show compassion, listen more, talk less. • Bring food, not judgment. A regular Saturday brunch with Sadie can make a significant difference, not just financially. • Foster social connections. Financial stress can cause isolation. Encourage hosting potlucks, card nights, or joining a community group. 2. Physical Inflation: The Expanding Middle Retirement brings more free time… and more room. Waistlines, cholesterol, and prescriptions all seem to rise in tandem. Signs you’re experiencing physical inflation: • Pants that used to be snug are now aspirational • Your Fitbit died months ago — and so did your motivation • Your pharmacy knows you by name... and birthday The bad news? Poor physical health is expensive. Chronic illness can deplete savings faster than a grandchild with your credit card. What You Can Do: • Keep moving. Walk, garden, spin — whatever gets you vertical and vibrant. • Lift weights. Muscle mass starts declining at 40. Resistance training isn’t just for 20-somethings. Strong is the new sexy, pass it on! • Meal plan smart. Grocery inflation peaked at 8.9% — eat better, waste less, save more. Consider shopping daily and buying only the amount of food needed for that day. Your health span should align with your lifespan. Stay strong, stay mobile, and yes, stretching counts — but not if you’re reaching for the TV remote. Inflammation — The Silent Saboteur If inflation is bad, inflammation is worse. Chronic inflammation contributes to: • Heart disease and stroke • Type 2 diabetes • Alzheimer’s disease and brain fog • Arthritis, osteoporosis, and varicose veins • Mood disorders such as anxiety and depression • Certain Cancers Even CNN and Al Jazeera recently reported that Donald Trump was diagnosed with chronic venous insufficiency (CVI) — a common, often overlooked condition among those over 55. Small veins, big problem. (Insert your own “tiny vein, tiny…” joke — I’m staying classy.) Inflammation is the unwelcome guest that never departs. If inflammation had a personality, it would be the dinner guest who drinks all your wine, insults your cat, and brings up politics at dessert. Whether it's fueling joint pain, causing swelling in your ankles, or messing with your metabolism, chronic inflammation is one of the biggest saboteurs of aging gracefully. It often hides in plain sight, presenting itself as: • Low-grade fatigue • Weight gain (especially belly fat) • Mood swings or brain fog • Increased pain and stiffness • Slow healing. What You Can Do: • Eat anti-inflammatory foods, such as leafy greens, whole grains, and healthy fats. Cut out the sugar. • Move each day. Yes, again. It’s that important. • Lower stress to improve sleep. Stress and poor sleep fuel inflammation. • Maintain social and emotional bonds. Loneliness and inflammation are frequently connected — break the link. De-Inflation — The Great Slowdown • So, we’ve discussed inflation... but what about its quieter, sneakier cousin: deflation? • No, not the economic kind. We’re talking about the physical “poof” that occurs when we reach our late 70s and 80s — when the padding diminishes, posture declines, and everything else… well, just seems a little less buoyant. • Suddenly, you’re shrinking. Your weight drops — but not in a sexy, "I’ve been intermittent fasting" kind of way. More like "my pants are falling down and my doctor says I’m 2 inches shorter" sort of vibe. Welcome to the gravitational pull of aging. Signs of De-Inflation: • Pants fit strangely, but not in a bragging way • You’re hunched over as if you’re forever bowing to the Queen • Your arms and legs have that crepey, crinkly look — like tissue paper with a gym membership • And let’s not forget the wrinkles on your face — a stunning topographical map of your life Let’s be honest: gravity always wins. Biology always wins. And yes, our skin thins — insert your own joke about being “thin-skinned” here. But we are not entirely powerless. Here’s How to Push Back (Gently — you don’t want to break a hip): • Check your posture monthly. Have a friend take a quick side photo. Are you upright and confident — or resembling a question mark? • Stretch regularly. Yoga, fascia stretching, and massage can help combat the hunch. • Move intentionally. Gentle strength training and balance exercises can maintain muscle and stability. • Moisturize and hydrate. For your skin, your joints, and your soul. • Celebrate your lines. They’re not “flaws” — they’re proof you’ve felt joy, sorrow, surprise, and a few good martinis. They’re not signs of aging; they’re signs you’ve been living. Remember: frowning only causes more wrinkles. So, smile — or better yet, laugh. Loudly. Often. Preferably at inappropriate moments. Oh — and take my advice on this: never (and I mean never) open your eyes during downward-facing dog. Some things just can’t be unseen. 3. Emotional Inflation: When Grudges Accumulate Like Interest Here’s the sneaky one. Emotional inflation appears as: • Bitterness over who got what in Mom’s will • Inflated egos and “right-titis” (a chronic need to be right) • Replaying 1983 arguments in your head like they’re Oscar contenders. • Giving not-so-nice nicknames to your former coworkers (and using them… publicly) • Keeping a mental spreadsheet of injustices — now colour-coded for quick reference (who says seniors are not tech-savvy?) Here’s the thing: emotional inflation isn’t just about what others have done. It’s also about how we interpret our role in those stories. Ready for a bold idea that can free you from decades of emotional baggage? What if we stopped keeping score and instead focused on how we want to show up in our relationships? What if you chose, intentionally, to be a generous sister, a supportive friend, a gracious parent, or a collaborative co-worker — not because they "deserve it," but because that's who you want to be? It’s not easy. It may require deep breathing and the occasional muttering in the car. However, for those willing, this mental reframe can be a total game-changer. What to do: • Let go. You can’t carry joy and a grudge at the same time — and joy is lighter. Lighten the emotional load. You don’t need to wait for someone to say sorry to feel free. • Choose your character. Think of it as casting yourself in the movie of your life. Be the wise one, the peacemaker, the person who breaks the cycle, not the one still angry about a forgotten birthday in 1996. • Write your own story. Present yourself as the person you want to be, even if others haven’t read the same script. You can’t control other people, but you can control how much space they occupy in your mind (especially if they’re not even paying for snacks). • Reframe your perspective. Instead of keeping score, focus on who you want to be: a generous sibling, a gracious friend, or a person at peace. Let go of the scorekeeping. It rarely results in a tie, and even if you win… You still feel empty. • Define your role. Be the big-hearted sibling, the calm presence, the one who lets go, not the person who stores bitterness in Tupperware containers. • Invest in joy. Dance classes, martinis, laughter — choose your remedy. • Talk it out. Therapy is more affordable than wine-fuelled Facebook rants and far more effective. Take the high road. There’s less traffic and better scenery. You can’t always avoid emotional hurt, but you can avoid living in a constant state of emotional inflation. And trust me, nothing deflates retirement faster than a bloated list of resentments. And if you’re feeling weighed down by the bloat of what life has thrown at you, remember: you can’t control inflation, but you can choose your response. Choose grace over grudges. Choose strength over stagnation. Choose the version of yourself that makes you proud. Because guess what? You’re still becoming who you are. Trust me — it’s better than a juice cleanse and more affordable than therapy. Some people age like fine wine; others age like vinegar. Emotional inflation is the burden you carry that doesn't show on the scale, but it weighs everything down. You can’t rewrite someone else’s story, but you can decide how to present yourself in your own. Taking the high road is less crowded and provides better perspectives. Inflation May Be Inevitable — But Misery? That’s Optional. Inflation has seeped into our lives like glitter at a craft table — impossible to contain and popping up in the most unexpected spots. It’s not just your budget that’s swollen (thanks to blueberries and Botox), but also your belly, your prescription drawer, and — if you’re not careful — your resentment list. But here’s the good news: While you can’t control how high prices go, how slow your metabolism becomes, or how long Uncle Jerry holds a grudge… You can control your response. So, here’s your call to calm, intentional, fabulous action: 1. Reclaim your power — in your spending, your body, and your mindset. 2. Choose curiosity instead of crankiness. Move more instead of staying still. Salad rather than salt (well… sometimes). 3. Be the kind of person who ages like disco — a little dramatic, slightly sparkly, and always ready to dance. And if you absolutely must inflate something… make it your sense of humour. Because in the grand game of Retirement Inflation Nation, laughter is your best hedge — and it’s fully indexed to joy. Oh — and if you're wondering whether I practice what I preach: I'm a certified fitness instructor and teach 5 jam-packed fitness classes a week at Canada’s largest gym. Movement isn’t just medicine — it’s music, community, and yes, a fabulous way to earn the right to your next martini. So, take it from someone still riding the rhythm of life — gravity is real, but so is joy. And we’re still dancing under the stars. (Here’s proof from the Coldplay concert — yes, I was the one yelling “Fix You” with both hands in the air and not a single regret.) Keep inflating the things that matter: your laugh lines, your playlist, and your purpose. With love, lunges, and a little glitter, Sue Don’t Retire... Rewire!

Georgia Southern researchers survey flood-stricken area of Bangladesh

Cox’s Bazar is a bustling tourist destination located on the southeastern coast of Bangladesh. It’s home to more than 3 million people living along the longest naturally occurring sea beach in the world, extending into the Bay of Bengal. But during the monsoon season, the area is prone to flooding and frequent landslides due to its geographical location and low altitude. More than 7,000 people living in the region were displaced in 2024 after a particularly severe season that destroyed thousands of shelters, leaving three dead. Georgia Southern University Assistant Professor Munshi Rahman, Ph.D., knows the dangers and devastation monsoon season can bring to this area. As a native of Bangladesh, he has witnessed firsthand how environmental changes, urbanization and deforestation contribute to the devastation. This is why he is actively working to help his home country identify the most disaster-prone areas through the use of geographic information systems and surveys. In January, Rahman and junior geoscience major Emma Robinson traveled to Cox’s Bazar to survey and identify the areas most prone to landslides and flooding with a goal of providing data to local government and nongovernmental organizations that could help address disaster risks. Robinson says she was thrilled to gain experience in field research and engage in work she’s passionate about. “Dr. Rahman’s project really inspired me because I’ve always had a drive to help the environment,” she said. “I thought this would be a great first step into research, especially since geology and geography are so closely related.” The two used geographic information systems, GPS and community input to pinpoint vulnerable spots near residential areas and population centers. Specifically, they found that many homes and refugee camps were built on slopes. Aside from being geographically vulnerable, they observed that many of these dwellings, built from bamboo poles, tarps, and corrugated metal, lacked the infrastructure to withstand flooding. “The key findings reveal a serious environmental degradation on local landscapes exacerbating the frequency and severity of landslides and flooding events in the region,” Rahman said. He added that these insights highlight the urgency for sustainable ecosystem management and the adoption of inclusive disaster management to reduce social and environmental vulnerabilities Rahman and Robinson suggest that their findings, combined with additional socioeconomic research, could provide a more comprehensive understanding of the situation on the ground. This would enhance disaster preparedness while promoting sustainable land use. “Not too many undergrads have opportunities like this,” she said. “I know this will help me get a jump-start on my senior thesis and give me a whole new perspective for future research projects. It’s made me more confident overall as a student and researcher.” Rahman is similarly grateful for the opportunity to give his students experience in the field. “As a professor, I’ve always wanted to give my students as much real-world experience as possible,” he said. “I also give Emma full credit. Prior to this trip, she had never traveled outside the U.S. She showed incredible courage and a real talent for research.”

School will soon be out for the summer, and many young families are opting to explore the beauty of their own country, travelling to top destinations like Toronto, Vancouver, and Halifax rather than heading south. While many travellers prioritize insurance for international trips, a recent CAA survey found that many people overlook the necessity of travel insurance for domestic travel, often assuming provincial healthcare will have them covered. "Exploring Canada’s breathtaking landscapes is an adventure worth taking, but unexpected travel hiccups don’t stop at the border,” says Susan Postma, regional manager, CAA Manitoba. “Whether it’s a sudden medical emergency or trip disruptions, having the right travel insurance ensures you can focus on making memories." A new national travel survey conducted for CAA reveals that nearly four in ten Canadians (39 per cent) travelled outside their home province without any form of travel insurance during their last trip. Some believed it was unnecessary (45 per cent), others worried about the cost (22 per cent), and 19 per cent took their chances, hoping nothing would go wrong. The reality? Provincial health insurance programs typically cover only basic emergency medical services when travelling in another province. “Many Canadians assume they’re fully protected when travelling within the country, but that’s simply not the case,” says Postma “A minor mishap can become a major expense, whether a broken ankle on a hike or a last-minute interruption.” Here are two unexpected ways travel insurance can help: You break your ankle while hiking on one of Canada’s beautiful nature trails and now need an ambulance or an airlift, crutches, and medication. You’re on vacation but must return unexpectedly because someone at home gets seriously ill. In stressful situations, like when a family member falls ill, it helps to have support when you need it. Trip Cancellation Insurance would cover the flight change fee and help get you back home. According to Orion Travel Insurance, part of the CAA family, the average medical claim cost has risen by 15 per cent annually since 2019, with everything from ear infections to air ambulance services becoming significantly more expensive. Here are ten additional tips to help your trip go smoothly, no matter where you travel. Know the cancellation policies and check limits or restrictions for everything you booked. Make sure you understand any key dates related to cancellations or changes. This includes accommodation, flights, car rentals, tours, and cruises. Check limits or restrictions on credit cards, employee benefits, and pensions to determine if you need additional travel insurance coverage. Make sure all your documentation is in order before you book. It is recommended that passport renewals be completed six months before your planned trip. Your passport should still be valid six months after your travel date, as this is required in several countries. There are varying documentation requirements, so make sure you fully understand what information you need to have ready and in what format. Read up on Government of Canada travel advisories for your destination. Understand the risk level associated with travel to a particular destination by checking the Government of Canada Travel Advice and Advisories website. Individual travel advisories remain on a country-by-country basis. It is important that Ontarians/Manitobans understand the ongoing uncertainty associated with international travel. Speak with your physician to discuss your travel plans. It is important that you speak to your physician to ensure you are up to date with needed travel vaccines and have them prescribe enough medication for the length of your trip. Ensure all the medication you take is packed in your carry-on and in its original bottles with labels intact. Consider purchasing travel insurance at the time of booking your trip. To lock in the best protection, book your travel insurance at the same time you book your trip. Booking Trip Cancellation or Interruption insurance will give you peace of mind that you and your investment are protected. Insurance must be in place before things go wrong for you to benefit from coverage. Get to the airport early. The old standby of being at the airport one hour before takeoff for domestic flights and two hours before international flights no longer apply. CAA recommends arriving at the airport at least two hours before domestic flight departures and at least three for international flights. Stay connected. It is important to have access to trusted, up-to-date information while travelling so you can monitor changing conditions and requirements and adapt accordingly. Bookmark the Global Affairs Canada website before departure and check it regularly while abroad. It is also a good idea to sign up for Registration of Canadians Abroad and stay in touch with a family or friend who knows your travel plans. Find these and more information at caamanitoba.com/travelwise Note emergency contact numbers. Provide your travel agent with contact details while travelling abroad and keep all important phone numbers handy; this includes how to call for help and your travel insurance assistance phone number. It is also a good idea to keep a physical copy of all their reservation information and leave those details with a friend or family member. Protect your ID. Ensure you have a digital and paper version of your Travel insurance wallet card, tickets to various events and attractions, and even your passport. You may also want to leave a copy of the necessary paperwork with family members or friends. Pack your carry-on wisely. Include the most important items, such as your passport/ID, boarding pass, travel itinerary, wallet, phone, charger, medications, toiletries, glasses/contacts, noise-canceling headphones, book/e-reader, snacks, empty water bottle, travel pillow, change of clothes, sweater, socks, pen, and reusable bags, in your carry-on bag. For more information on travel insurance and how to stay protected, visit caamanitoba.com/travelwise Based on the sample size of n=2,005 and with a confidence level of 95%, the margin of error for this research is +/- 2%.)

School will soon be out for the summer, and many young families are opting to explore the beauty of their own country travelling to top destinations like Vancouver, Calgary and Halifax rather than heading south. While many travellers prioritize insurance for international trips, a recent CAA survey found that many people overlook the necessity of travel insurance for domestic travel, often assuming provincial healthcare will have them covered. "Exploring Canada’s breathtaking landscapes is an adventure worth taking, but unexpected travel hiccups don’t stop at the border,” says Kaitlynn Furse, Director Corporate Communications, CAA SCO. “Whether it’s a sudden medical emergency or trip disruptions, having the right travel insurance ensures you can focus on making memories." The national travel survey conducted for CAA reveals that four in ten Ontarians (41 per cent) travelled outside their home province without travel insurance during their last trip. Some believed it was unnecessary (43 per cent), others worried about the cost (24 per cent), and 20 per cent took their chances, hoping nothing would go wrong. “Many Canadians assume they’re fully protected when travelling within the country, but that’s simply not the case,” adds Furse. A minor mishap can become a major expense, whether a broken ankle on a hike or a last-minute interruption.” Here are two unexpected ways travel insurance can help: You break your ankle while hiking on one of Canada’s beautiful nature trails and now need an ambulance or an airlift, crutches, and medication. You’re on vacation but must return unexpectedly because someone at home gets seriously ill. In stressful situations, like when a family member falls ill, it helps to have support when you need it. Trip Cancellation Insurance would cover the flight change fee and help get you back home. According to Orion Travel Insurance, part of the CAA family, the average medical claim cost has risen by 15 per cent annually since 2019, with everything from ear infections to air ambulance services becoming significantly more expensive. Here are ten additional tips to help your trip go smoothly, no matter where you travel. Know the cancellation policies and check limits or restrictions for everything you booked. Make sure you understand any key dates related to cancellations or changes. This includes accommodation, flights, car rentals, tours, and cruises. Check limits or restrictions on credit cards, employee benefits, and pensions to determine if you need additional travel insurance coverage. Make sure all your documentation is in order before you book. It is recommended that passport renewals be completed six months before your planned trip. Your passport should still be valid six months after your travel date, as this is required in several countries. There are varying documentation requirements, so make sure you fully understand what information you need to have ready and in what format. Read up on Government of Canada travel advisories for your destination. Understand the risk level associated with travel to a particular destination by checking the Government of Canada Travel Advice and Advisories website. Individual travel advisories remain on a country-by-country basis. It is important that Ontarians/Manitobans understand the ongoing uncertainty associated with international travel. Speak with your physician to discuss your travel plans. It is important that you speak to your physician to ensure you are up to date with needed travel vaccines and have them prescribe enough medication for the length of your trip. Ensure all the medication you take is packed in your carry-on and in its original bottles with labels intact. Consider purchasing travel insurance at the time of booking your trip. To lock in the best protection, book your travel insurance at the same time you book your trip. Booking Trip Cancellation or Interruption insurance will give you peace of mind that you and your investment are protected. Insurance must be in place before things go wrong for you to benefit from coverage. Get to the airport early. The old standby of being at the airport one hour before takeoff for domestic flights and two hours before international flights no longer apply. CAA recommends arriving at the airport at least two hours before domestic flight departures and at least three for international flights. Stay connected. It is important to have access to trusted, up-to-date information while travelling so you can monitor changing conditions and requirements and adapt accordingly. Bookmark the Global Affairs Canada website prior to departure and check it regularly while abroad. It is also a good idea to sign up for Registration of Canadians Abroad and stay in touch with a family or friend who has knowledge of your travel plans. Find these and more information at caasco.com/travelwise Note emergency contact numbers. Provide your travel agent with contact details while travelling abroad and keep all important phone numbers handy; this includes how to call for help and your travel insurance assistance phone number. It is also a good idea to keep a physical copy of all their reservation information and leave those details with a friend or family. Protect your ID. Ensure you have a digital and paper version of your Travel insurance wallet card, tickets to various events and attractions, and even your passport. You may also want to leave a copy of important paperwork with family members or friends. Pack your carry-on wisely. Place the most important items like passport/ID, boarding pass, travel itinerary, wallet, phone, charger, medications, toiletries, glasses/contacts, noise-canceling headphones, book/e-reader, snacks, empty water bottle, travel pillow, change of clothes, sweater, socks, pen, and reusable bags in your carry-on bag. For more information on travel insurance and how to stay protected, visit caasco.com/travelwise Based on the sample size of n=2,005 and with a confidence level of 95%, the margin of error for this research is +/- 2%.)

Lending Survey Results Reveal Recent and Dramatic Concern Due to Tariff Policy

Global consulting firm J.S. Held releases its proprietary “Lending Climate in America” survey results from Phoenix Management, a part of J.S. Held. The second quarter survey results highlight lenders’ views on important issues, including policy decisions along with their national and global impact. Each quarter, Phoenix Management, a part of J.S. Held, surveys lenders to identify important trends focused on the latest economic issues, business drivers, and credit trends in the current lending climate. The “Lending Climate in America” survey provides valuable information to lenders, attorneys, private equity sponsors, and the financial news media, exploring topics like: What factors do lenders see as most likely to impact the US economy in the next six months? Phoenix’s Q2 2025 “Lending Climate in America” survey asked lenders which factors could have the strongest potential to impact the economy in the upcoming six months. Sixty-seven percent of lenders are paying the most attention to the possibility of a U.S. recession, while 40% of lenders believe overall political uncertainty has the strongest potential to impact the economy. Lenders also expressed moderate concern regarding the possibility of constrained liquidity in capital markets. To see the full results of Phoenix’s “Lending Climate in America” Survey, please visit: https://www.phoenixmanagement.com/lending-survey/ What shifts do lenders observe in their customers’ hiring and capital improvement plans? Lenders revealed what actions their customers may take in the next six months. Over half of the surveyed lenders believe their customers will raise additional capital. Most telling was that lenders believe only 3% of their customers have plans to hire new employees (down from 56% in 1Q) and only 23% have plans for capital improvements (down from 67% in 1Q). Which industries are expected to see the most volatility over the next six months? For the first time in recent memory, the 3 industries that respondents identified as most likely to experience volatility in the next six months were different from the prior quarter - consumer products (60.0% versus 20.7%), retail trade (43.3% versus 31.0%), and manufacturing (33.3% versus 20.7%). How do lenders plan to adjust their loan structures? Additionally, Phoenix’s “Lending Climate in America” survey asked lenders if their respective institutions plan to tighten, maintain, or relax their loan structures for various sized loans. For larger loan structures (greater than $25M), the plan to maintain loan structures remained relatively constant from Q1 to Q2, decreasing by 8 percentage points. As loan sizes decrease, the percentage of lenders that plan to maintain (as opposed to increase) their loan structures increased – quite dramatically in the under $15M range. How has lender sentiment toward the US economy changed from Q1 to Q2? Lender optimism in the U.S. economy decreased for the near term, moving from 2.33 in Q1 2025 to 2.10 in Q2 2025. In this current quarter, there is heavy expectation of a C level performance (63%), with the remainder split between D and B levels. More telling, lender expectations for the U.S. economy’s performance in the longer term increased sharply from 2.11 to 2.53. Of the lenders surveyed, 57% believe the U.S. economy will perform at a B level during the next twelve months, a hefty increase from the prior quarter. The “Lending Climate in America” survey is administered quarterly to lenders from various commercial banks, finance companies, and factors across the country. Phoenix Management, a part of J.S. Held, collects, tabulates, and analyzes the results to create a complete evaluation of national attitudes and trends. To view the full results, click on the button below: To connect with Michael Jacoby or for any other media inquiries, please contact: Kristi L. Stathis, J.S. Held +1 786 833 4864 Kristi.Stathis@JSHeld.com

Why Paying Cash Can Hurt Your Credit

Earlier this week, Rosa Marchitelli from CBC’s Marketplace recently profiled a Calgary man whose credit score shockingly dropped to zero—not because he was reckless with debt, but because he paid cash for everything. No missed payments. No defaults. Just a lifetime of financial caution that, ironically, made him invisible in the eyes of Canada’s credit system. It’s the kind of story that stops you in your tracks—because it turns everything we’ve been told about “good financial behaviour” on its head. In this post, we’ll break down the surprising logic behind Canadian credit scores, why living debt-free can actually hurt your financial profile, and how to play the credit game without compromising your values. If you’ve ever thought, “I don’t need credit because I’m responsible,” this might just change your mind. Back when I taught the Mortgage Agents Licensing Course, offered by Mortgage Professionals Canada, I always looked forward to my session on credit. Why? Because most people don’t really understand how credit scores work—or how to protect and build a healthy one. So, you’ve always paid cash, avoided debt like the plague, and proudly told your kids you don’t even own a credit card. Congratulations! You’re a responsible citizen… but your credit score is probably dreadful. Wait—what? Yes, the wonderful world of Canadian credit scoring is one of life’s mysteries. It rewards behaviour that may seem risky to the debt-averse but is actually just good financial practice in disguise. So, let’s lift the curtain and decode the quirky logic behind your credit score. Credit Scores 101: It’s Not About Your Morals. It’s About Your Habits In Canada, credit scores range from 300 to 900—the higher, the better. Your score reflects your ability to manage borrowed money based on your past use of credit products such as credit cards, lines of credit, and loans. Here’s the twist: not using credit at all doesn’t make you look smart; it makes you look suspicious. Credit bureaus assume that if you don’t have credit, it’s because you can’t get it—not because you’re a thrifty minimalist growing kale and paying cash. Meet the Scorekeepers: Equifax vs. TransUnion Canada has two major credit bureaus: • Equifax – Favoured by banks and mortgage lenders. • TransUnion – Commonly used by credit card and auto lenders. Each bureau calculates your score slightly differently, so the numbers may vary, like having two referees at the same game. Expect some disagreement on the calls. Pro tip: check both reports annually (for free) to spot any errors early. The Government of Canada has more information for you here. Credit Score Bands Score Range 800–900 - Excellent Access to the best rates and financial products. 740–799 - Very Good Qualifies for most products with favourable terms. 670–739 - Good Solid score; ~35% of Canadians are here. 580–669 - Fair May qualify but at higher rates. 300–579 - Poor High risk. Harder to get approved. Minimum Scores for Common Credit Products Credit Cards: 600+ Premium cards usually require 700+ Auto Loans: 620+ Higher rates if below 700 Consumer Loans: 640+ Lower scores = shorter terms/higher rates Mortgages: 680+ CMHC-insured loans often require a 680+ Pro Tip: Paying cash may make Grandma proud, but lenders can’t assess you without credit activity. No credit = no score = no loan Decoding Credit Codes: The ABCs and 1- 9s of Credit Credit accounts are coded using a letter for the type of credit and a number for how well you manage it. Letter Codes: R – Revolving (e.g., credit cards) I – Instalment (e.g., auto loans) M – Mortgage O – Open (e.g., lines of credit) Number Ratings: 1 – Paid on time 2–5 – Late by 30 to 120+ days 6 – Not used 7 – Making regular payments via credit counseling 8 – Repossession 9 – Sent to collections or bankruptcy A trade line is a record of your credit account. Each shows the credit type, lender, balance, and payment history. Think of it as a financial resume—each tradeline is like a job entry listing your past and present “performance” with a particular creditor. How Long Does Negative Info Last: Bankruptcy (R9); Equifax (7 Years) TransUnion (6 years) Late Payments: Equifax (6 Years) TransUnion (6 years) Collections: Equifax (6 Years) TransUnion (6 years) Consumer Proposal: Equifax (3 years post-payment) TransUnion (3 years post-payment) Credit Counselling (R7): Equifax (7 years after the final payment) TransUnion (6 years after the final payment) Pro Tip: Keep in mind that after falling off your credit report, bankruptcies may still appear in public records. Here's How Your Score Is Calculated Factor Weight and Why It Matters Payment History 35% Late payments are like bad breath—unforgettable. Credit Utilization 30% Use less than 30% of your limit. Length of Credit 15% Longer credit history is more trustworthy. Credit Mix 10% Variety of products = balanced borrower. New Credit Inquiries 10% Too many apps = desperation sniffed by lenders. Source: TransUnion Canada - Credit Score Factors Utilization: More Credit, Used Sparingly = Better Score Yes, it’s weird—but true: someone with five credit cards and a $50,000 limit who uses only $2,000 will likely have a better score than someone with a single $2,000 credit card which is nearly maxed out. Why? Utilization is calculated as a percentage. The more room you leave untouched, the more responsible you appear. Ghosts & Abstainers: No Credit is a Red Flag So, back to the Marketplace story we mentioned earlier. As we consider all the factors involved in credit scoring, is it surprising that this man in Calgary, who paid cash for everything, had his score drop to zero after a long period of inactivity? Not really. Credit bureaus don’t reward abstinence—they penalize it. If you haven’t borrowed in a while, you may be “credit invisible.” It’s like trying to get hired without a resume. No record? No offers. Building (or Rebuilding) Credit What if you need to fix a low score due to missed payments, bankruptcy, or simply a lack of credit history? Getting your credit score up is entirely possible—with patience, consistency, and the right strategy. Here’s a practical framework I use. 1. Get Credit – A secured card works just fine. 2. Use It – Buy groceries, gas, Netflix—whatever you usually pay for. 3. Pay on Time – Even the minimum. Set a reminder …or three. 4. Stay below 30% – Don’t max it out. Do this, and your score should rise like a perfectly baked soufflé. When Credit Counselling is the Better Option Struggling with debt? Credit counseling might be your best path forward. These services consolidate all unsecured debts into one monthly payment and negotiate with creditors to reduce or eliminate interest. It’s a couple-of-year commitment that avoids bankruptcy, and you pay something back. However, your credit will reflect an R7 status for 3 years after your final payment or 6 years after you sign the contract, whichever comes first. Pro Tip: Credit counseling is the more noble route, but remember that it still significantly affects your score. (Source: Credit Counselling Canada) What If There’s an Error—or You’ve Been Hacked? If you spot a mistake on your report—or worse, see signs of identity theft—don’t panic. Here’s what to do: 1. Request a copy of your report from Equifax and TransUnion. 2. Highlight the error and contact the bureau to initiate a dispute. 3. Provide supporting documents. 4. Follow up regularly—bureaus must investigate within 30 days. If you’re a victim of identity theft: • Contact your bank and credit card issuers immediately. • File a police report. • Consider placing a fraud alert or credit freeze on your credit file. Here are important links with more details on how to work with both <Equifax> and <TransUnion> The final statement (get it?) Your credit score doesn’t care if you’re a good person. It only cares if you’re a predictable borrower. So don’t take it personally—play the game smartly. Because in the wild world of credit, it’s not about morals. It’s about whether you paid your $9.99 Netflix bill on time. Now go forward and charge responsibly. Don’t Retire … Re-Wire! Sue

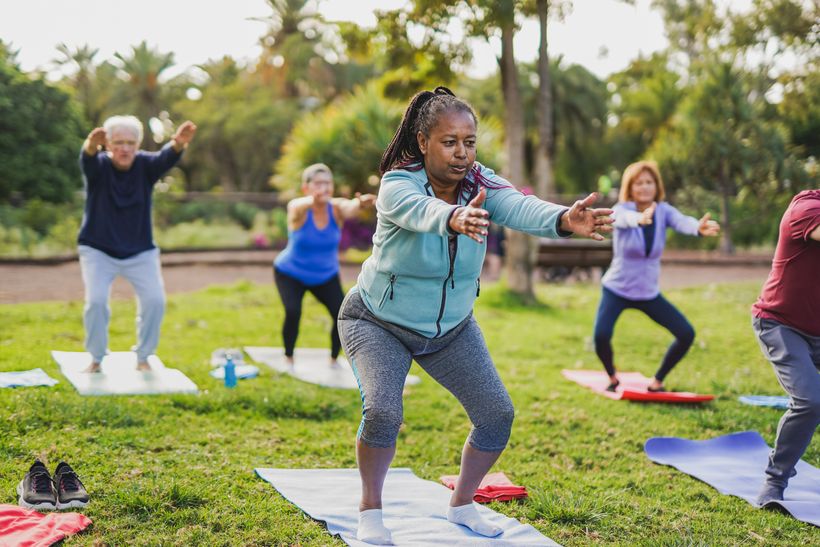

Have you ever dreamed of being an Olympic athlete? Perhaps you have wondered what it would feel like to stand on that podium in front of the world as your national anthem plays. For most Olympic athletes, the journey begins very early in life. But imagine what it would be like if you started training for this event in your 60s? Read on if you want an edge to discover how to win the Retirement Games and still pass the drug test (let’s face it, peeing is not an issue for many at that age)! Here is your chance to get on the podium at the most crucial game of your life. On Your Marks, Get Set, Ready, Go! Retirement was more like a coffee break five decades ago—brief, predictable, and over before your muffin cooled. In 1975, the average Canadian could expect to live about 73.53 years. Fast forward to 2025; we're clocking in at nearly 83.26 years. Even juicier? The lastest research shows half of today's 20-year-olds in Canada are expected to live past 90. That’s why we need to think of retirement these days, not as a sprint; instead, it’s an ultramarathon with hills, potholes, and the occasional pulled hamstring. Most of us never expected to be training for it in our sixties, but here we are—so pull up your compression socks and move. The starter's pistol is about to fire, whether you're ready or not! Surprise! You're Retired While you may dream of selecting your retirement date like a fine wine, many face the reality of a boxed kind instead. Approximately 6 in 10 Americans retire earlier than they planned. Research from the Transamerica Center for Retirement Studies shows that many individuals experience unexpected early retirement due to personal health issues, employer discretion, or family-related circumstances. https://www.cbsnews.com/news/retirement-age-in-america-62-claiming-social-security-early/ Sometimes, it's a health scare, a loved one’s illness, or a harsh employer downsizing. Nobody whispers the term "ageism," but when companies replace senior employees with younger, more affordable talent (or AI bots), it’s not subtle—it’s math.As Morgan Housel reminds us in his bestseller, The Psychology of Money, "The most important part of every plan is planning for your plan, not going according to plan." Expect the unexpected. Train as if retirement could sneak up on you—because it just might. Get Fit, Stay Sharp: Health is the First Leg of the Race Physical and mental health are the fuel for your retirement. The rest doesn’t matter without them; we’re not just talking about lifting weights. (Though, yes, lift some weights.) Regular physical activity provides numerous benefits for older adults, including a reduced risk of dementia and enhanced cognitive function. Exercise can help maintain brain health, reduce mental decline, and even reverse some age-related brain shrinkage. Additionally, physical activity can improve mood, reduce anxiety, and enhance balance and coordination, leading to a better quality of life. • Strength training enhances bone density, metabolism, and mental health. (Source: Mayo Clinic) • Flexibility and balance? Try yoga or tai chi. Harvard Health says they reduce pain and stiffness. • Mental fitness? Cue up Wordle, Canuckle (the Canadian cousin), or Sudoku. • Dancing? It's beneficial for your brain and your swagger • Listening to music or playing an instrument can reduce stress and boost memory. Gold Medal Tip: Motivation is overrated; action is everything. Don’t be a couch potato. A new study conducted at the University of Pittsburgh School of Medicine shows that older adults who spend more time sedentary — such as sitting or lying down — may be at a higher risk for lower cognition and in areas linked to the development of Alzheimer’s disease, no matter how much they exercise! So make sure you show up, move, and the motivation will catch up. Wealth Training: Stop Hoping, Start Budgeting Here's a shocker: Retirement doesn't mean your expenses magically disappear. According to Steve Willems' podcast “10 Retirement Myths You May Not Want to Believe,” most retirees don’t spend less. Aside from the mortgage, spending remains surprisingly consistent, especially during the Go-Go years (ages 55-75)”. We like what we like: groceries, entertainment, travel, and stylish or comfortable clothes are still on our shopping lists. That’s why many of us in retirement will need to pay more attention to spending and budgeting. Check Obligation Spending Retirement is the perfect time to reevaluate expenses from obligation rather than genuine need or joy. Here's a thoughtful way to frame that idea: Retirement is the season of freedom, so why are you still paying for things that feel like a burden? Now that you’re no longer earning a regular paycheck, every dollar matters more than ever. This means it’s time to take a closer look at obligatory expenses. These might include: • Helping adult children financially (even when it stretches your budget) • Donating to every fundraiser or cause just because someone asked • Hosting large family gatherings that leave you exhausted and over budget • Maintaining memberships, subscriptions, or traditions that no longer bring you joy. (We talk a lot more about this in a previous post What’s your Retirement Plan B While generosity is admirable, it shouldn’t jeopardize your financial security or peace of mind. Retirement should focus on investing in what truly matters to you now, rather than keeping up appearances or adhering to outdated expectations. Here’s a gentle mantra to adopt: “I’ve earned the right to say no with love and confidence.” Freeing yourself from obligation spending doesn’t mean becoming stingy; it means becoming intentional. Give where your heart feels full, not where your guilt feels heavy. After all, you didn’t work all those years to keep writing checks out of habit. Balance Beam- Budget What’s your plan when overtime isn’t an option and the budget doesn’t balance? Start with a good old-fashioned reality check: • Write down ALL expenses. • Tally up your income. • Look for a surplus (yay, trip!) or a shortfall (boo, time to pivot). Look at Canadian Government Pensions • Here's the math. Old Age Security (OAS): Max is about $713/month or $8,556/year. And don’t forget the dreaded government clawback (formally known as the Old Age Security Pension Recovery Tax which starts at ~$90,997. • Canada Pension Plan (CPP): The average monthly payment is $758, while the maximum is $1,364 per month or $16,368 per year. So with these two programs combined, provided you meet requirements, as a senior, you're looking at somewhere between $17,000–$25,000/year before tax. If your lifestyle needs a bit more jazz hands, here’s how to bridge the gap: DIY Income Builders: • Slash debt. Every dollar you don't spend is one you keep. • Downsize and bank the equity. • Buy or build an ADU and rent it. I have written more about ADU's here. • HELOC or Reverse mortgage (borrow strategically). • Withdraw from investments (4% rule). • Monetize your skills: consulting, tutoring, or writing that novel you started in 1993. Gold Medal Tip: Track your joy per dollar. If you’re going to spend, make it worth it. Rewire, Don’t Retire: Finding Purpose The biggest myth of retirement? That doing nothing feels good forever. (Spoiler alert: it doesn’t.) Passion is your GPS. It guides you towards what fills your heart. Whether you write poetry, walk dogs, or paint birds wearing tiny hats, your joy matters. And legacy? That’s just purpose with staying power. There’s science to support the benefits of this lesson. A study in JAMA Psychiatry found that people with a sense of purpose had a lower risk of mortality and disability Purpose-Driven Paths: • Volunteer: Look for a cause that fires you up. • Get a part-time job: Perhaps you can fill in at a local bookstore, garden center or be a barista? • Hobbies: Take up painting, pottery, or poetry. • Go Back to School: Many Universities such as The University of Toronto offer free, non-credit courses through programs as part of their community outreach. Seniors (over 60) enrolled at York University may have all or part of their academic fees waived at the domestic fee rate for York University degree credit courses as part of their mature student program. • Spend real time with people you love, maybe your grandkids or elderly parents. • Reconnect with old friends – not just on Facebook, but in person • Get out of your backyard and see the world Gold Medal Tip: You're never too young (or too old) to chase what lights you up. Start a business, get that degree you always wanted, and write that book. Go. For. It. Support: No One Trains Alone Retirement can be lonely. As we age, friends pass, routines fade, and isolation creeps in. That’s why your squad matters more than ever. Find Your Pod: • Family & Friends: Set expectations. Ask for help. Host Sunday dinners. Stay connected. • Fitness & Social Clubs: Join a walking group or participate in a gym class, followed by regular post-sweat coffee. • Faith Communities: Spirituality and structure in one. Sing in the choir. Serve at events. • Third Places: As sociologist Ray Oldenburg says, these are neutral hangouts like libraries, community centers, or your local café. They’re tied to lower loneliness and better mental health. Think of Cheers: “Where everyone knows your name!” Gold Medal Tip: Your local pickleball court or knitting circle might just be your new training ground. Attitude Training: Stop Acting Your Age Here’s a radical thought: Maybe we feel old because we act old. Want to stay young? Stay curious, try new things. Try line dancing, pickleball, bird watching, improv, or learning to code. Yes, code. What was the worst advice our mothers gave us? “Act your age.” Nonsense! Whoever said, “You’re only as old as you feel” was on to something – but let’s take it up a notch: How about you’re only as old as your playlist! The Power of a Youthful Attitude in Retirement A successful retirement isn’t just about savings accounts and spreadsheets — it’s about mindset. A positive, youthful attitude is one of the most powerful (and overlooked) assets you can carry into retirement. Even if you don’t feel youthful or optimistic, “fake it ‘til you make it” is more than just a catchy phrase—it’s a strategy. The goal isn't to accurately describe your aches, fears, or fatigue but to set yourself up for success! Science backs it up: a positive outlook boosts health, sharpens cognition, and increases longevity. From a practical perspective, optimism makes it easier to try new things, adapt to change, and enjoy the present—all essential in retirement. So, if the voice in your head says, “I’m too old for that,” try responding with, “This is my time.” You begin to build because what you tell yourself matters, as does what you believe. Retirement is your reward. Approach it like the vibrant, capable, unstoppable human you are because attitude, not age, sets the tone. Gold Medal Tip: You’re only as old as the last thing you tried for the first time. Try something ridiculous, I double dare you! Final Stretch The Retirement Games are here, and let me be crystal clear: this isn’t amateur hour. This is your Olympic moment, with medals awarded for stamina, strategy, and a solid sense of humour. Whether you're rounding the first turn at 45 or doing your victory lap at 75, now is the time to train. You’ve built strength, stretched your budget, flexed your purpose muscle, assembled your dream team, and rebooted your mindset. Now it’s time to lace up, lean in, and live life to the fullest. This isn’t about perfection; it’s about preparation. You won’t achieve a podium finish through wishful thinking; you’ll attain it through action, adaptation, and a great deal of repetition. So, put on your metaphorical tracksuit (or actual tracksuit if it's laundry day) and begin training with determination. The gold medal retirement isn’t just possible—it’s within reach. Cue the confetti cannon. You’re not just aging—you’re advancing. And champions, as we know, don’t retire… they rewire, recharge, and rewrite the playbook. On Your Marks, Get Set, THRIVE! Don’t Retire … Re-Wire! Sue

UD researchers launch open-source tool to boost global food security and water sustainability

Efficient water usage in agriculture is crucial for sustaining a growing human population. A better understanding of the systems that support agriculture, farmers and farmlands allows for food production to become more efficient and prosperous. That's what makes the Monthly Irrigated and Rainfed Cropped Areas Open Source (MIRCA-OS) dataset so important. MIRCA-OS offers high-resolution data on 23 crop classes — including maize, rice and wheat — and helps researchers, students and farmers examine irrigation, rainfall and croplands and how they interact with global water systems. Co-authored by Endalkachew (Endi) Kebede, a doctoral student in University of Delaware’s Department of Geography and Spatial Sciences, a recent paper focused on MIRCA-OS was published in Nature Scientific Data. Kyle Davis, assistant professor in the Department of Geography and Spatial Sciences and the Department of Plant and Soil Sciences, served as a co-author on the paper and coordinated the study. “We first developed a comprehensive data library of crop-specific irrigated and rainfed harvested areas for all countries,” Kebede said. “This involved two years of gathering data from a wide range of international, national and regional sources. Through this process, we produced a tabulated crop calendar, annual harvested area grids and monthly harvested area grids for all irrigated and rainfed crops.” “The amount of effort that Endi put in to gather, process and harmonize all of this data is truly incredible,” Davis said. “His effort is a very important contribution to the scientific and development communities.” Doctoral student Endalkachew Kebede (left) and Assistant Professor Kyle Davis. (Photo credit: University of Delaware) Cropland accounts for 13% of Earth's total habitable land, and the preservation of cropland is important in feeding the growing global population. “Crop production has been a widespread human activity for a few thousand years, and it has a huge role in global food security,” Kebede said. “But it also has unintended impacts on the environment, such as overutilization of water resources, pollution through rivers or the effects on soil and the environment.” MIRCA-OS can play a crucial role in helping to better understand croplands and agriculture, allowing the global population to be successfully fed while minimizing the agricultural effects on the environment. In addition to the data included on cropland and water resources, MIRCA-OS allows researchers to view social aspects like poverty and unemployment through an agricultural lens, creating a better understanding of the interconnectivity of agriculture and social issues. MIRCA-OS is an updated version of the earlier MIRCA2000 dataset. Kebede said the MIRCA2000 was released nearly two decades ago, so renewing the data gives users more accurate and timely information. Both datasets specialized in examining irrigation and rainfall, but the MIRCA-OS added two new complexities to their data. First, MIRCA-OS is open source, meaning it is publicly available for anyone to use, download, or modify. Kebede said the added accessibility allows the technology to contribute to anyone's work, whether it be a student, a researcher or a farmer. “Anybody can use, update it, or upscale it to the special skill they’re interested in,” Kebede said. “Some might use it for research, some might use it to create policies and some might use it to practice agriculture.” To arrange an interview with Davis, visit his profile and click on the contact button.