Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

Ninety-three percent of patients with a new cancer diagnosis were exposed to at least one type of misinformation about cancer treatments, a UF Health Cancer Center study has found. Most patients encountered the misinformation — defined as unproven or disproven cancer treatments and myths or misconceptions — even when they weren’t looking for it. The findings have major implications for cancer treatment decision-making. Specifically, doctors should assume the patient has seen or heard misinformation. “Clinicians should assume when their patients are coming to them for a treatment discussion that they have been exposed to different types of information about cancer treatment, whether or not they went online and looked it up themselves,” said senior author Carma Bylund, Ph.D., a professor and associate chair of education in the UF Department of Health Outcomes and Biomedical Informatics. “One way or another, people are being exposed to a lot of misinformation.” Working with oncologists, Bylund and study first author Naomi Parker, Ph.D., an assistant scientist in the UF Department of Health Outcomes and Biomedical Informatics, are piloting an “information prescription” to steer patients to sources of evidence-based information like the American Cancer Society. The study paves the way for other similar strategies. Most notably, the study found the most common way patients were exposed to misinformation was second hand. “Your algorithms pick up on your diagnosis, your friends and family pick up on it, and then you’re on Facebook and you become exposed to this media,” Parker said. “You’re not necessarily seeking out if vitamin C may be a cure for cancer, but you start being fed that content.” And no, vitamin C does not cure cancer. Health misinformation can prevent people from getting treatment that has evidence behind it, negatively affect relationships between patients and physicians, and increase the risk of death, research has shown. People with cancer are particularly vulnerable to misinformation because of the anxiety and fear that comes with a serious diagnosis, not to mention the overwhelming amount of new information they have to suddenly absorb. While past research has studied misinformation by going directly to the source — for instance, studying what percentage of content on a platform like TikTok is nonsense — little research has looked at its prevalence or how it affects people. The team first developed a way to identify the percentage of cancer patients exposed to misinformation. UF researchers collaborated with Skyler Johnson, M.D., at Huntsman Cancer Institute, an internationally known researcher in the field. The survey questions were based on five categories of unproven or disproven cancer treatments — vitamins and minerals, herbs and supplements, special diets, mind-body interventions and miscellaneous treatments — and treatment misconceptions. The myths and misconceptions were adapted from National Cancer Institute materials and included statements like “Will eating sugar make my cancer worse?” The team surveyed 110 UF Health patients diagnosed with prostate, breast, colorectal or lung cancer within the past six months, a time when patients typically make initial treatment decisions. Most had heard of a potential cancer treatment beyond the standard of care, and most reported they had heard of at least one myth or misconception. The most common sources were close friends or family and websites, distant friends/associates or relatives, social media and news media. The findings mark a shift in misinformation research, with major implications for the doctor-patient relationship, said Bylund, a member of the Cancer Control and Population Sciences research program at the UF Health Cancer Center. “I still think media and the internet are the source and why misinformation can spread so rapidly, but it might come to a cancer patient interpersonally, from family or friends,” she said. Most patients rarely discussed the potential cancer treatments they had heard about with an oncologist, the study also found. Next, the researchers plan to survey a wider pool of patients, then study the outcomes of interventions designed to decrease misinformation exposure, like the information prescription.

April 1st is the one day we all expect to be fooled. Scammers are counting on the other 364

Breaking News: Free Cruise for All Retirees! Congratulations!!! If you are reading this, you have just been chosen for a luxury Caribbean cruise, a $5,000 shopping spree, and a lifetime supply of… well, something vaguely exciting. All you need to do is: Click this link, enter your banking info, confirm your SIN, and maybe your childhood pet's name for good measure. Still reading? Good. Because if that opening gave you even the tiniest thrill, the little flutter of wait, really? You've just experienced exactly what scammers are counting on. APRIL FOOL'S!!! And also: welcome to the world of phishing. Population: way too many of us. Phishing vs. Fishing: A Retirement Skill You Didn't Know You Needed There are two kinds of fishing in retirement. One involves a dock, a thermos of good coffee, and no deadlines at all. The fish might or might not cooperate. That's fine. That's the whole point. The other scenario involves someone trying to steal your identity by congratulating you on a cruise you never booked, a prize you never won, and a windfall that demands your banking details, your SIN, and, just for fun, the name of your first pet. (Buttons. It's always Buttons.) Let's make sure you're fluent in the first kind and bulletproof against the second. Fraud Doesn't Just Happen to Fools Here's something important to say aloud before we proceed. Fraud isn't caused by people being careless, gullible, or old. It is orchestrated by professionals whose full-time job is to manipulate human behaviour under pressure. There is a clear difference between these two, and how we discuss fraud influences whether victims come forward or stay silent out of shame. This issue is more significant than most realize. Canadians lost over $638 million to fraud in 2024, an increase from $578 million the previous year, according to the Canadian Anti-Fraud Centre. However, that figure only tells part of the story. The CAFC estimates that just 5 to 10 percent of total fraud losses are ever reported. Think about that for a moment. The number we see is already staggering, and the real total is almost certainly ten times higher. Seniors make up a disproportionate share of those losses, especially in investment fraud, romance scams, and the grandparent scam. But here's the part the statistics don't show: fraud is improving at its craft. These aren't the poorly written emails of 2005. Today's scams are refined, patient, and psychologically targeted. They're designed to create urgency, confusion, and fear — aiming to override careful thinking precisely when it's needed most. So let's talk about what that actually looks like. A Very Personal Fraud Story That Will Stay With You A family reached out to me recently, after reading one of my earlier posts on fraud and seniors. Their father had been the victim of a prolonged scam, one that unfolded over months and caused significant financial damage. They only found out after he passed away. Three things about this story stopped me cold. First, their father kept meticulous records. He journaled every interaction, every step, every decision. There was essentially a play-by-play account of how he became entangled and how difficult it became to find a way out. Second, he was an intensely private person. Not a single family member knew any of it was happening while it was happening. Third, he was a chartered professional accountant. Decades of financial training, discipline, and experience. Someone who understood numbers, risk, and how money moves better than most people ever will. And still. Under the right conditions, with the right psychological pressure applied at the right moments, he was drawn in. That is not a story about a foolish man. That is a story about how sophisticated fraud has become. And it is a story that is playing out in living rooms and email inboxes across this country every single day. Why Seniors Are Targeted (And It's Not What You Think) Scammers don't just go after older adults because they think we're naive. They go after us because we have assets. Savings. Home equity. Good credit. Pension income that actually shows up every month. We're not easy targets; we're valuable ones. They also go after us because retirement can come with conditions that fraud is specifically designed to exploit: financial anxiety about making savings last, changes in how we process decisions under pressure, and, for many, reduced opportunities to run something by a trusted person before acting. Social isolation is not a character flaw. It is a vulnerability, and the people running these operations know exactly how to use it. The Scams You Actually Need to Know About The Grandparent Scam. You get a call. It's your grandchild. They're in trouble, arrested, in an accident, stranded, and they need money right now. Please don't tell Mom and Dad. The caller may not even sound exactly right, but panic has a way of filling in the gaps. Sometimes a fake lawyer or police officer jumps on the line to add credibility. The script is designed to bypass your rational brain and go straight for your heart. If this ever happens: hang up. Call your grandchild directly on a number you already have. Every time. The CRA Impersonation Call. This one is especially popular at tax time. An official-sounding voice informs you that you owe back taxes and if you don't pay immediately via e-transfer or gift cards, a warrant will be issued for your arrest. The Canada Revenue Agency does not call you out of the blue demanding gift cards. Full stop. If you're ever unsure, hang up and call the CRA directly as 1-800-959-8281. The Romance Scam. Someone finds you online, charming, attentive, almost too good to be true. Weeks or months in, a crisis emerges. Could you help, just this once? These scams are emotionally brutal and financially devastating. If an online relationship moves unusually fast and a financial request follows, that's not love. That's a script. The Investment Opportunity. Guaranteed returns. Exclusive access. Limited time. These words belong together the way "healthy" and "deep-fried" don't. Legitimate investments don't come with countdown clocks. Phishing Emails and Texts. These mimic your bank, Canada Post, Service Canada, Amazon, and anything you'd recognize. They look almost right. The email address is a little off. The link goes somewhere slightly wrong. They want you to click, to enter information, to act now before something bad happens. The urgency is the tell. No Shame. Seriously. None. If this has happened to you, or someone you love, please hear this: falling for a scam does not mean you are getting old, losing it, or slipping cognitively. It means you are human and were placed under carefully engineered psychological pressure by someone who practices this for a living. That is it. The end. And if you need a reminder that this crosses every age and profession, consider the case of a retired district court judge who lost the equivalent of over $100,000 to a digital arrest scam. Fraudsters called claiming his phone number was linked to a trafficking investigation. Despite decades on the bench watching deception unfold in real time, fear and intimidation did what all that professional knowledge could not protect against. A judge. Still got hooked. That is what these scams do when they are built well. (Source: Devdiscourse) RCMP Sergeant Guy Paul Larocque of the Canadian Anti-Fraud Centre puts it plainly: "Fraudsters are professional salespeople who work a target until they close the deal and get their money." That framing matters. You would not blame yourself for being sold something by a skilled salesperson operating under false pretenses. This is no different. The embarrassment is real and completely understandable. However, it does not fairly reflect what occurred. The CAFC has pointed out that many individuals feel ashamed of being victims of fraud and hesitate to report it, but every report helps break up fraud schemes and protect others. Reporting to the Royal Canadian Mounted Police is not a sign of failure; it is a vital way to safeguard the next person. A Word to Family Members re: Fraud: Drop It Like It's Hot If someone you care about has been scammed, put down whatever you are holding, take a breath, and read this carefully. Do not scold them. Do not lecture them. Do not "grandsplain" them into the ground. Grandsplaining, for the uninitiated, is mansplaining for the aged, and it is just as unwelcome. Nobody needs a slow, patient, thoroughly detailed breakdown of everything they should have done differently while they sit there wishing the floor would open up and swallow them whole. They already know. They feel terrible. They have probably been replaying every moment of it since it happened, asking themselves how they missed it, why they trusted it, and what they were thinking. What they do not need is you asking those same questions out loud. Your role at this moment isn't to be the smartest person in the room. It's not to claim you would never have fallen for something like this. And it's certainly not to start a sentence with "well, I always said you should..." because if you finish that sentence, you're on your own. Your job is to be kind. Full stop. Help them contact the bank. Sit with them while they file the report. Make the tea. Handle the phone call they are too rattled to make. Be the calm in the room. That is what love looks like in a crisis, and this is a crisis. Now here is the part where the tables turn, so pay attention. Scammers are not ageist. They are not sitting in a room somewhere saying, "Let's only go after the over-65s today." They go after anyone with money, a phone, and a moment of distraction. Which means they go after everyone. Your inbox is not immune. Your judgment under pressure is not immune. Your "I would never fall for that" confidence is, frankly, exactly the kind of thing scammers count on. Fraud can happen to anyone, and sharing your experience with others, whether or not money was lost, can help prevent them from being victimized by the same or a similar fraud. Nobody is too sharp, too young, or too digitally savvy to be targeted. The call is coming for all of us eventually. So when it comes for you, and you call your mother in a panic, wouldn't you rather she answer with warmth instead of a very long "I told you so"? Be nice to her now. Consider it an investment. One day, she might be the one sitting you down for "the talk." And at that point, the only appropriate response is to make the tea and keep your opinions to yourself. What the Experts Say: Practical Tips to Stop Fraud In my book "Your Retirement Reset" (ECW Press: Now available for Pre-Order here), I cover the topic of fraud and scams." I wanted to address this issue in depth because fraud prevention is not a footnote in retirement planning. It belongs front and center. Here is an excerpt of Chapter 9 of the book: "Remember the old saying, 'Nothing ever comes free'? While it is hard for many seasoned Canadians not to trust a caller, unfortunately, that's the way of the world today. Here are some tips for protecting yourself. Be skeptical. Be wary of unsolicited phone calls, emails, or messages, especially those asking for personal information or money. Don't take their word for it. Ask the person for their details. If they say they are calling from your bank, get their name and branch number and call your bank for verification. If the message is in an email, contact the institution identified in the email. Do not respond right away, ever. Don't share personal information. Never share personal, financial, or health information with unknown individuals or organizations. Consult trusted individuals. Discuss suspicious offers or communications with family members, friends, or trusted advisors. This is especially important if you are asked to donate to a charity or make any kind of financial investment. Use technology wisely. Install antivirus software, create strong passwords, and stay alert to phishing tactics such as harmful links in texts or emails. Use the block feature on your phone to cut off repeat callers you suspect are fraud artists. Work closely with your financial institution. Ask your bank to send alerts for any unusual activity on your account. Review your statements every month and report unauthorized transactions immediately. Report suspicious activity. If you suspect a scam has targeted you, contact the police. Stay informed. Keep up to date on prevalent scams aimed at older adults. A quick Google search on any unsolicited information request can often tell you whether it has already been flagged. These scams are frequently reported to authorities and featured in the media and on consumer advocacy websites." How to Stay Off the Hook When It Comes to Fraud A little friction can be helpful. Scammers depend on speed, on you reacting before you think. The best thing you can do is slow down. Avoid clicking links in unexpected messages; instead, go directly to the company's website by typing it yourself. Call back on a number you find independently, not one provided in the suspicious message. Check email addresses carefully, as a transposed letter can sometimes be all it takes. Keep your devices updated, since those updates fix real vulnerabilities. Discuss these topics openly. With your kids, friends, book club, or the person behind you in the coffee line. Scams flourish in silence and shame. Talking honestly is one of our strongest protections. In retirement, urgency belongs in spin class. Not your inbox. What to Do If You Took the Bait No judgment here. These scams are truly sophisticated. Smart, experienced, financially educated people fall for them, as we've just established. If you think you've been scammed, stop engaging immediately, change your passwords, contact your bank to flag or freeze your account, run a security scan on your device, and report it to the Canadian Anti-Fraud Centre at 1-888-495-8501. Reporting matters even if you cannot recover the money. It protects the next person in line. Think of it as cutting the line before the fish swims off with your whole tackle box. 3 Things Worth Setting Up This Week to Protect Yourself from Fraud These take 20 minutes and quietly protect you around the clock. Two-factor authentication (2FA) adds a second verification step. It's usually a text code. And it helps ensure that a stolen password alone won't give access to your accounts. Credit Card controls allow you to lock and unlock your debit or credit card instantly through your bank's app, so if something seems suspicious, you can freeze it within seconds. Real-time alerts enable you to set notifications for any transaction over a threshold you specify, so if someone is spending your money, you are informed immediately, rather than finding out at the end of the month when the damage is already done. Don't Get Hooked by Fraud. Retirement should be about freedom. The freedom to fish from a proper dock, travel somewhere warm, and spend your money on things that truly bring you happiness. It's not meant to involve fake urgency, suspicious links, or people who want your SIN and the name of your childhood cat. We Need to Do More to Protect Seniors The fraud prevention system in this country, to be frank, hasn't kept pace with the rise of fraud itself. That gap is real, it's growing, and it needs more attention than it currently gets. Meanwhile, the best we can do is stay informed, keep in touch with trusted people, and not let embarrassment prevent us from seeking help or reporting what happened. You worked hard for what you have. You deserve to enjoy it without looking over your shoulder. So enjoy the lake. Take the cruise — a real one that you booked yourself. Spend wisely, live well, and protect what's yours. And if anyone ever tells you that you've won something you never entered? Smile. Wish them a Happy April Fool's. Then hang up. Have a scam story, a close call, or thoughts on what fraud prevention is getting right or getting wrong? I would love to hear from you. Drop it in the comments or send me a note. This is exactly the kind of conversation we should all be having, and the more real experiences we share, the better equipped we all are to protect each other. Sue Don't Retire…ReWire! My Book is Now Available for Pre-Order If this message speaks to you, or to someone you love, I hope you will pre-order a copy of Your Retirement Reset. Available September 8, 2026. Here's the link. And if you love supporting Canadian booksellers, please also check with your local independent bookstore. Most can easily order it for you.

Fewer Parents are Reading to Their Kids—and Why It Matters

A dramatic decline in reading for pleasure in the United States has fewer American parents reading aloud to their children — and experts warn the consequences can be dire. “It builds connections,” Carol Anne St. George, an expert in early literacy at the University of Rochester’s Warner School of Education and Human Development, recently told The74 for an article citing a 41-percent decline in parents reading to children daily. “People talk about text to text, text to world,” St. George said, “and those are the kinds of things that help children cognitively think and classify their world around them.” Many young parents grew up in an education system focused on reading as a means to testing and building skills rather than enjoyment. As a result, St. George worries, they often view reading to their young as an obligation rather than a joy and a time to bond. Experts say an increased reliance on screens and digital content and time pressures and competing demands on families have also fueled the decline. St. George notes that children benefit greatly from being read to regularly. The advantages of early literacy include: • Having a more robust vocabulary and stronger communications skills. • Being better prepared to learn in school. • Having a closer relationship with their parents. • Higher academic achievement and better health outcomes later in life. What Parents Can Do St. George advises parents to: • Let children choose books they enjoy. • Make reading part of a daily routine and that bedtime is ideal. • Focus on fun and connection. • Model good reading behavior because children mimic what they see. St. George is available for media interviews and can be reached by contacting Theresa Danylak, the director of communications at the Warner School, at tdanylak@warner.rochester.edu.

ExpertSpotlight: No Joke: The Curious Origins and Enduring Traditions of April Fools’ Day

Every April 1, the world collectively loosens up. Friends prank friends, brands try to outdo each other with outrageous announcements, and even the most serious newsrooms occasionally get in on the joke. But behind the laughter and “gotcha” moments, the origins of April Fools’ Day are anything but straightforward - and that’s part of what makes it so fascinating. One of the most widely accepted origin stories dates back to 1582 and the Gregorian calendar reform. When France shifted New Year’s celebrations from late March (around April 1) to January 1, not everyone got the memo, or chose to follow it. Those who continued celebrating in spring became the subject of ridicule, often tricked with fake gifts or sent on pointless errands. They were dubbed “April fools,” a label that stuck. Other theories reach even further back, connecting the day to ancient seasonal festivals like Hilaria, where people donned disguises, mocked authority, and celebrated the unpredictable shift into spring. Across cultures, the common thread is clear: a moment in the calendar where normal rules are bent, and mischief is not just accepted - it’s expected. What started as localized traditions has evolved into a global cultural phenomenon. Media outlets, corporations, and public figures now participate in April Fools’ Day with increasingly elaborate hoaxes. Perhaps the most famous example came from the BBC in 1957, when it aired a segment about Swiss farmers harvesting spaghetti from trees, complete with convincing visuals. Viewers were fooled, and a legendary prank was born. Today, in an era of viral content and misinformation, April Fools’ Day walks a fine line between humor and credibility, forcing audiences to question what they see and hear. Beyond the pranks, the day reveals something deeper about human nature. It’s a rare, socially sanctioned opportunity to challenge authority, play with truth, and share in collective amusement. For journalists, it also offers a unique angle: how stories spread, why people believe them, and what it says about trust in media. In a world often dominated by serious headlines, April Fools’ Day reminds us that sometimes, the most powerful connection comes not from facts alone, but from the shared experience of being delightfully fooled. Our experts can help! Connect with more experts here: www.expertfile.com

What the Meta/YouTube Verdict Still Misses About Youth Social Media Harm

The verdict against Meta and YouTube has reignited debate over addictive design and youth social media harm. But according to Harshi Sritharan, clinician and digital dependency expert with Offline.now, one key issue is still being overlooked: digital emotional regulation. Sritharan works with young people and families dealing with the real-life fallout of harmful platform design, including compulsive scrolling, sleep disruption, body-image distress, emotional dysregulation, and conflict at home. “The goal isn’t to remove technology from their lives entirely,” says Sritharan. “It’s to help young people and their families build healthier relationships with it.” She can speak to why regulating platform design matters, why digital resilience and online emotional regulation should be treated as core life skills, and why simply restricting access without healthier alternatives can push vulnerable youth into harder-to-monitor spaces. As news coverage focuses on liability and platform accountability, Sritharan offers a frontline clinical perspective on what these harms actually look like inside homes - and what young people, parents, schools, and policymakers may still be missing. ABOUT THE EXPERT Harshi Sritharan is a clinician and digital dependency expert with Offline.now, a digital wellness platform connecting individuals and families with therapists, coaches, and social workers who specialize in healthier relationships with technology.

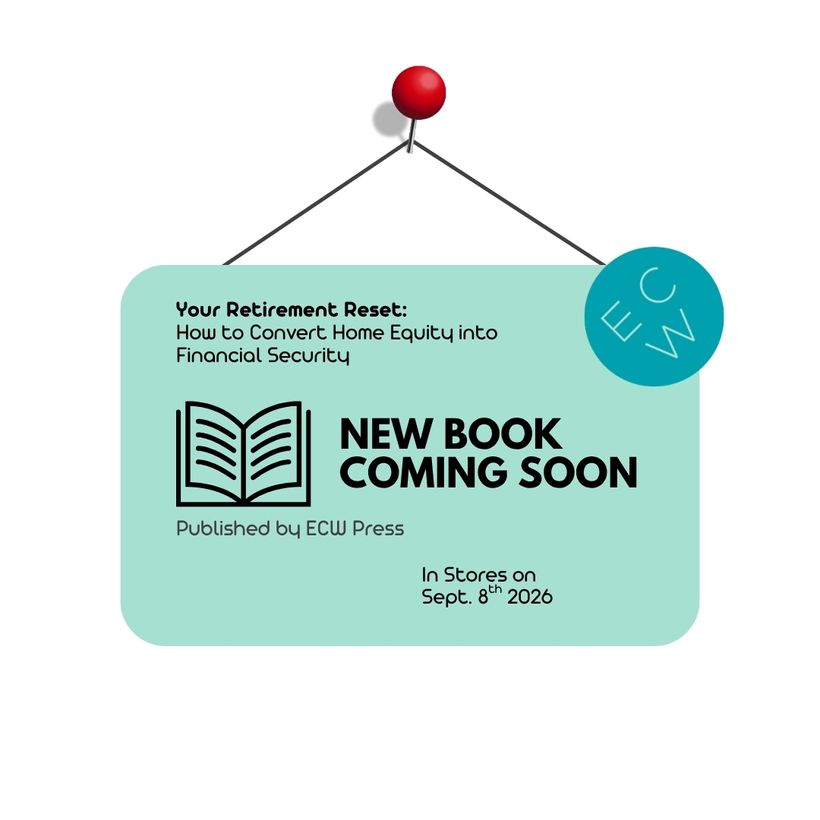

Your Retirement Reset: My New Book will Be in Stores on Sept. 8th

This one has been a long time coming. My new book, Your Retirement Reset: How to Convert Home Equity into Financial Security, published by ECW Press, finally has a publication date. Why I Wrote This Book I have spent decades watching far too many older Canadians carry unnecessary financial stress into what should be a more secure and dignified stage of life. Throughout my career as a mortgage broker, business owner, and later as an executive at HomeEquity Bank, I saw the same painful pattern again and again: people who had worked hard, paid down their homes, built real equity, and still felt trapped. Many were living with fear, cutting back on basic pleasures, worrying about every bill, and feeling ashamed that they had not “saved enough.” Meanwhile, a major asset was sitting right beneath their feet. What struck me most was this: younger homeowners often see home equity as a financial tool, but many retirees do not. For many older Canadians, the idea of borrowing against their home feels frightening, even when it could improve their quality of life and help them stay independent. This resistance is not just about math. It is emotional. It is psychological. And it is deeply tied to identity, security, family, and fear. The Retirement Problem We Are Not Talking About Honestly Enough The old retirement script is failing too many people. We are living longer. The cost of living keeps rising. Private sector pensions have largely disappeared. Healthcare and long-term care costs are real concerns. And many people reaching retirement are discovering, far too late, that the traditional advice to simply save, downsize, and make do does not reflect today’s reality. At the same time, most older Canadians want to age in place. They want to remain in the homes and communities they know and love. They do not want to be pushed into selling, renting, or moving in with family unless they truly choose that path. Yet many are gripped by what I call FORO — Fear of Running Out. That fear shapes countless decisions and robs people of peace of mind. It’s actually rooted in neuroscience and the way we’re wired to behave as we do. I’ve posted about this here in my newsletter and Substack a lot. Because it’s important. This is not a fringe issue. It is a national issue. And it deserves a more honest conversation. Why This Book Matters for Canadians 55+ There is a critical gap in this country when it comes to retirement literacy. Many Canadians over 55 have substantial value tied up in their homes, yet traditional retirement advice often does not seriously incorporate home equity into the conversation. At the same time, the information people do find is often fragmented, biased, overly technical, or scattered across lenders, planners, brokers, lawyers, accountants, media stories, and well-meaning family members. That leaves people vulnerable. They may rely on outdated assumptions. They may wait too long to explore options. They may make decisions out of fear rather than clarity. And because older adults usually do not have decades to recover from a financial mistake, the stakes are high. I want to be direct about this: one wrong decision later in life can be extremely hard to reverse. Seniors need unbiased, transparent information they can actually trust. I wanted to create a resource that is practical, plainspoken, and empowering. Not a sales pitch. Not a jargon-filled textbook. Not a one-size-fits-all solution. What I Hope This Book Will Accomplish I hope “Your Retirement Reset” helps Canadians 55+ do a number of things. First, I hope it helps people understand their options more clearly. Too many retirees only hear about a narrow set of choices. I want readers to see the full landscape and understand how different strategies work, including the pros, cons, and trade-offs. Second, I hope it helps people replace fear with confidence. Retirement should not be defined entirely by scarcity thinking. When people understand how to use all of their assets strategically, including home equity, they can make decisions from a position of strength rather than panic. Third, I hope it helps families have better conversations. One of the great hidden challenges in retirement planning is communication. Adult children often mean well, but they may not understand the emotional reality of aging, independence, or financial vulnerability. These conversations matter, and they are often avoided until a crisis forces them. This book is meant to encourage healthier, earlier, and more respectful dialogue. Fourth, I hope it helps more older Canadians protect their dignity and independence. To me, this is the heart of the matter. As I work through my current MBA studies, my life today is filled with spreadsheets. But retirement shouldn’t be. It is about autonomy, confidence, lifestyle, peace of mind, and the ability to live on your own terms for as long as possible. The Information Gap Nobody Is Filling One reason I felt so compelled to write this book is that the resources simply are not where they need to be. There is no shortage of opinions in the marketplace. But there is a shortage of clear, balanced, accessible education specifically designed for older Canadians trying to navigate retirement in the world as it actually exists now. Many books in this category are dated, narrowly focused, or too technical for many of the people I speak with. And it’s to be expected that much of the consumer-facing content around financial products like reverse mortgages comes from lenders themselves. Many seniors are left trying to piece together a life-changing financial strategy from disconnected advice and Google searches. That is the gap I am trying to fill. Canadians need impartial, balanced information they can trust — especially around home equity strategies and retirement financing. I believe Canadians deserve better than that. They deserve a resource that speaks to them in plain language, respects their intelligence, acknowledges the emotional complexity of these decisions, and gives them practical tools to move forward. We Need a More Modern Retirement Roadmap This book is built around a simple idea: retirement planning cannot just be about accumulating savings. It also has to be about learning how to use those resources wisely. That includes understanding how to: • create income • manage spending • shelter income from unnecessary tax pressure • protect savings from fraud and bad decisions • evaluate whether home equity should play a role in your retirement strategy These are the pillars I keep coming back to. They reflect what I believe Canadians in this stage of life truly need. I want readers to come away not just informed, but steadier. More capable. More hopeful. This Is Personal for Me I am part of this demographic myself. I understand the questions, the transitions, the uncertainty, and the pressure. I also know from lived experience that retirement is not simply a financial event. It is a life event. It affects your confidence, your relationships, your routines, your health, and your sense of who you are. That combination — professional experience and personal experience — is exactly what I bring to every page. That is why I have approached this book not simply as a finance book, but as a practical guide for real people facing real decisions. My hope is simple: that this book helps more Canadians 55+ move into the next chapter of life with greater knowledge, less fear, and a stronger sense of possibility. Because retirement should not just be about getting by. It should be about living with confidence, dignity, and choice. The Book is Now Available for Pre-Order If this message speaks to you, or to someone you love, I hope you will pre-order a copy of Your Retirement Reset. Available September 8, 2026. PRE-ORDER NOW: https://ecwpress.com/products/your-retirement-reset And if you love supporting Canadian booksellers, please also check with your local independent bookstore. Most can easily order it for you. Don’t Retire… Re-Wire! Sue

User-submitted photo of Barton Street in Hamilton, which placed second on Ontario’s 2025 top ten list. Concern about road conditions continues to be top of mind for Ontarians, with eight in 10 CAA members worried about the state of the province’s roads, according to new survey data released as CAA South Central Ontario (CAA SCO) launches the 2026 CAA Worst Roads campaign. The survey also found that nearly 70 per cent of CAA members don’t believe enough is being done to maintain Ontario’s roads, up five per cent from last year, reinforcing what many road users experience daily. Cracks in pavement remain the most common issue (88 per cent) identified by respondents, followed closely by potholes (87 per cent), uneven or bumpy road surfaces (81 per cent) and congestion (80 per cent). “Ontarians are telling us loud and clear that road conditions are not keeping pace with expectations,” says Teresa Di Felice, Assistant Vice President, Government and Community Relations for CAA South Central Ontario. “The Worst Roads campaign gives Ontarians a direct way to raise their concerns and helps decision-makers understand what roads need attention according to their constituents.” Despite widespread frustration, the survey suggests most concerns are not reaching decision-makers. It found that nearly 80 per cent of Ontarians commonly complain about road conditions to a spouse, co-worker or mechanic rather than to the governments responsible for road maintenance. CAA calls on Ontarians to nominate roads in urgent need of repair “We know this campaign works,” says Di Felice. “When Ontarians speak up and nominate roads they want to see repaired, we consistently see action.” Many nominated roads are critical trade and supply‑chain corridors, linking the CAA Worst Roads campaign to community growth and economic strength. “Growing population pressures in Ontario, particularly in the GTA, are driving the need for improved infrastructure to mitigate congestion issues, and the rapid wear and tear of our roads,” adds Di Felice. Poor road conditions contribute to vehicle damage, congestion, and safety risks for all road users, including pedestrians and cyclists. With the cost of living already high, the added expense of repairs caused by potholes and deteriorating roads is placing further strain on household budgets. The survey found that 80 per cent of Ontarians are paying out of pocket for those repairs, while ten per cent are forgoing repairs altogether. For more than two decades, the CAA Worst Roads campaign has influenced infrastructure decisions across the province. Roads that appear on the annual Worst Roads list often see repairs prioritized or moved up, as governments respond to public feedback. In the last five campaigns, over 10 roads have received attention due to their appearance on the CAA Worst Roads list. Most recently, County Road 49 in Prince Edward County received a large provincial investment supporting the repair of over 18 kilometres of the road. County Road 49 has been a popular road on the CAA Worst Roads Campaign’s top 10 list for some time. Ontarians can nominate any road for issues, including potholes, congestion, faded road markings, poor signage, traffic light timing, and pedestrian or cycling infrastructure. CAA SCO is encouraging all road users to participate. Nominations for the 2026 CAA Worst Roads campaign are open now and can be submitted online at www.caaworstroads.com until April 17. Once nominations close, CAA will compile and release Ontario’s Top 10 Worst Roads later this year, as well as regional top five lists. CAA conducted an online survey with 2,718 CAA SCO Members between January 6 to 14, 2026. Based on the sample size and the confidence level (95 per cent), the margin of error for this study was +/- 2 per cent.

Covering Cuba? Augusta has one of the leading experts ready to help with your coverage

Cuba is facing one of its most severe crises in decades, as compounding economic and energy challenges continue to strain everyday life on the island. Persistent fuel shortages have led to rolling blackouts, transportation disruptions, and reduced industrial output, while inflation and shortages of basic goods have eroded purchasing power for ordinary Cubans. Tourism, once a critical source of foreign exchange, has struggled to fully recover, and the country continues to grapple with declining productivity and limited access to international capital. These pressures have contributed to rising public frustration, increased migration, and a government response that blends cautious economic reforms with efforts to maintain stability. Paolo Spadoni is an ideal expert for journalists covering this evolving situation. As a specialist in Cuba’s political economy, his work focuses on the island’s external sector, including foreign investment, remittances, tourism and the impact of international sanctions. He brings a rare ability to connect on-the-ground developments – such as energy shortages or policy changes, to the broader structural realities shaping Cuba’s economy. With deep academic research and ongoing analysis of current reforms, Spadoni offers clear, credible insight into whether Cuba’s latest measures signal meaningful transformation or simply short-term responses to a prolonged crisis. Paolo Spadoni, PhD, is a widely recognized expert on Cuba and its international relations. He is a tri-lingual political economist with a specialization in international relations and a focus on Latin America’s political and business environments. His research focuses on international relations theories, Cuba's economy and business market, foreign investment in Cuba and U.S.-Cuba relations. View his profile Since this crisis escalated, Spadoni has been the 'go-to' expert for reporters with media from across North America like Reuters, Bloomberg and The New York Times connecting with him for his expertise, input and perspective on the situation. LA TERCERA: “The Cuban tourism sector was already struggling before the Covid pandemic. The best year for international tourism in Cuba was 2017 in terms of foreign exchange earnings. That was the year in which $3.3 billion was collected, and tourism represented 10% of Cuba's GDP at that time. In terms of employment, it provided 120,000 direct jobs and roughly 500,000 indirect jobs. So it played a significant role. That was the best year for international tourism in Cuba, which coincidentally ended in November of that year with the sanctions imposed by the first Trump administration. From then on, tourism from North American visitors began to decline, but European and Canadian visitors were already decreasing,” Spadoni explained to La Tercera. CBC NEWS: "Most of those investments are real estate investments more than tourism investments, meaning the Cuban military has taken possession of prime locations in the best tourism areas of Cuba," said Paolo Spadoni, an associate professor at Augusta University in Augusta, Ga., and co-author of the 2025 book The Cuban Tourism Industry: Evolution, Challenges and Prospects. Columbia Law School: "While seeking to finalize an economic agreement with Cuba, the Trump administration could secure deals across various sectors of the economy. However, tourism holds the most promising opportunities in the short term." Global News (Canada):

MEDIA RELEASE: Manitobans paying more for vehicle repairs as CAA Worst Roads campaign launches

Submitted photo of Saskatchewan Avenue, Winnipeg’s Worst Road in 2025. Manitobans are paying more out of pocket to fix their vehicles as concerns about road conditions continue to grow, according to new survey data released as CAA Manitoba launches its annual CAA Worst Roads Campaign. The survey found 92 per cent of Manitobans are concerned about the state of roads in the province and are spending an average of $944 to repair vehicle damage caused by poor road conditions. This is $122 more than last year, when the average repair cost was $882. As Winnipeg grows and congestion worsens, fixing key trade and connector routes isn’t just about road conditions; it’s about protecting the economy, keeping our city moving, and prioritizing affordability. “Most of the roads people flag as priorities are the same routes our supply chain depends on, they’re how goods get in, out, and across the province,” says Ewald Friesen, manager, government and community relations for CAA Manitoba. “With Manitoba’s growing population, especially in Winnipeg, there is a need for improved infrastructure.” At the same time, the rising cost of living has made consumers more mindful of their spending, and people are opting to keep their cars longer rather than buy a new one. Poor roads increase the wear and tear of tires, lead to higher fuel consumption, and increase the risk of other costly repairs. Nearly half of drivers (45 per cent) reported experiencing vehicle damage due to poor road conditions, with potholes cited as the leading cause, accounting for 86 per cent of damage. Most drivers (75 per cent) are paying for repairs out of pocket; 12 per cent filed a claim with Manitoba Public Insurance. Another 14 per cent said they chose not to repair the damage, up six per cent from last year. Despite widespread frustration, the survey suggests most concerns are not reaching decision-makers. It found that 85 per cent of Manitobans commonly complain about road conditions to a spouse, coworker or mechanic rather than to the governments responsible for road maintenance. Manitobans encouraged to nominate roads most in need of repair “The Worst Roads campaign is a proven platform that gives Manitobans a voice and helps governments identify the roads causing the most frustration,” says Friesen. “We know it works because we see governments prioritize budgets and move up road repairs every year after appearing on the list.” Manitobans can nominate any road for issues, including potholes, congestion, faded road markings, poor signage, traffic light timing, and pedestrian or cycling infrastructure. CAA Manitoba is encouraging all road users to participate. Nominations are open at www.caaworstroads.com from March 17 to April 10. Once nominations close, CAA Manitoba will release a list of the top 10 worst roads in the province, along with regional lists. CAA conducted an online survey with 649 CAA Manitoba Members between January 6 to 14, 2026. Based on the sample size and the confidence level (95 per cent), the margin of error for this study was +/-3 per cent.

Expert Q&A: What is Soft Diplomacy and how does it impact classrooms?

"Right now, storytelling is critical. Language learning is highly personal, and it’s the person-to-person relationships that grease the wheels," says Cheryl Ernst, director of the English Language Institute at the University of Delaware. She recently published English Language Programs as Facilitators of Soft Diplomacy in Innovations in Star Scholars Press. Here's how she's discussing this important topic. Q: What is the focus of this research, and why is it important? Ernst: ELI and other English language programs provide the ideal space for communication development, cross cultural appreciation, gaining life skills, and raising awareness about people beyond the media. Post pandemic, we’re hearing across campus how individuals feel less connected, and in English language classrooms, connection is critical. Language is only learned through production and practice since it’s a skill that needs to be honed. In language, there is no such thing as perfect. In our classrooms, English is the common goal, and everyone comes to that space at their own levels and overflowing with imperfection. Our students learn to use their vulnerability as a tool. They learn the value of a growth mindset living in a culture that is different from their own, and with that comes an appreciation for difference, respect for others, trust, human-to-human communication. Q: What inspired this research? Ernst: More than 30 years of observation, conversations, experiences, and personal relationships. There was no term to describe the skills English language programs teach beyond grammar (what’s perceived, anyway). Terms like personal diplomacy, person-to-person diplomacy, civic diplomacy, and the like happens all the time and oversimplifies what we do. In my readings, I started to see overlaps between soft power and diplomacy, which led to the concept of Soft Diplomacy. Then what distinguishes Soft Diplomacy from other more common monikers are the variety of skills that happen organically in our classrooms that we rarely acknowledge and students may not recognize. Q: What are some key findings or developments? Ernst: Institutionally, ELPs can do better highlighting the skills beyond English that we teach organically or deliberately. Q: How could this work potentially impact the field or the wider public? Ernst: Respecting ELPs for the space they provide and the skills they offer. It’s not “just English,” rather is learning to communicate in a common language and with people from around the globe. I’d like people to realize that relationships are foundational, that there are common values across nations and that differences are not bad. What version of English is “correct” British or American dialects (the New York? Wisconsin? Alabama? Iowa?). Q: What are the next steps or upcoming milestones in your research? Ernst: A former student and I have launched a podcast series called Soft Diplomacy in Action that focuses on personal stories from those who work in international education. We’ve interviewed an ELI associate professor from Morocco, the UD coordinator of the Mandela Fellows program, a professor who sees (and lives) the diplomatic value of sports, and a retired English language professional. We’re looking forward to continuing these conversations with individuals from a variety of disciplines that also work in this space but through different lenses. ABOUT CHERYL ERNST Cheryl Ernst is the director of the English Language Institute at the University of Delaware where she and her colleagues and students practice Soft Diplomacy every day. Her professional areas of interest include program administration and international marketing, teacher training and working with international teaching assistants, curriculum design, and advanced level academic English (graduate levels). To speak with Ernst her work and the importance of Soft Diplomacy, reach out to MediaRelations@udel.edu.