Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

Florida renters struggle with housing costs, new statewide report finds

Nearly 905,000 low-income renter households in Florida are struggling to afford their housing costs, according to the 2025 Statewide Rental Market Study, released by the University of Florida’s Shimberg Center for Housing Studies. Prepared for Florida Housing Finance Corporation, the report provides a comprehensive look at the state’s rental housing conditions and is used to guide funding decisions for Florida Housing’s multifamily programs, including the State Apartment Incentive Loan (SAIL) program. “Florida’s strong population growth has collided with limited housing supply, pushing rents beyond what many families can afford,” said Anne Ray, manager of the Florida Housing Data Clearinghouse at the Shimberg Center. “This report helps policymakers and housing providers target resources where the need is most acute — including communities that are experiencing the fastest growth and the greatest affordability gaps.” Key findings from the 2025 study include: A growing affordability gap: An estimated 904,635 renter households earning below 60% of their area median income (AMI) are cost burdened, paying more than 40% of their income toward rent. These households are spread across the state, with 64% in Florida's nine most populous counties, 33% in mid-sized counties and 3% in small, rural counties. Surging population and higher rent and housing costs: Between 2019 and 2023, Florida added more than 1 million households — nearly 195,000 of them renters — driven by in-migration from states like New York, Illinois and California. Despite the addition of more than 240,000 multifamily units, median rent soared nearly $500 per month, from $1,238 to $1,719. After years of growth, Florida's older renter population is holding steady: Renters age 55 and older represent 39% of cost burdened households, up from 29% in 2010 but similar to 2022 numbers. Most renters are working: 79% of renter households include at least one employed adult, compared to 67% of owner households. Most non-working renters are seniors or people with disabilities. Homelessness is on the rise: The report estimates 29,848 individuals and 44,234 families are without stable housing, up from 2022, as hurricanes and tight markets contribute to displacement. Assisted housing provides an alternative to high-cost private market rentals: Developments funded by Florida Housing, HUD, USDA and local housing finance authorities provide over 314,000 affordable rental units statewide. Future risks to affordable housing stock: More than 33,000 publicly assisted units may lose affordability protections by 2034 unless renewed. Evalu ating affordable housing in Florida “State- and federally-assisted rental housing developments are essential to providing stable, affordable homes for Florida’s workforce, seniors, and people with special needs,” Ray said. “Florida Housing Finance Corporation’s programs make up a significant portion of this housing, and our study helps ensure those resources are directed where they’re needed most. Preserving these developments — and expanding them — is critical to keeping pace with Florida’s growing population and maintaining affordability.” Since 2001, the Shimberg Center has produced the Rental Market Study every three years to inform strategic investments in affordable housing across Florida. The study evaluates needs across regions and among key populations including seniors, people with disabilities, farmworkers and others. The Rental Market Study and the Florida Housing Data Clearinghouse are part of a 25-year partnership between the Shimberg Center and Florida Housing Finance Corporation to support data-driven housing policy and planning.

In another milestone commitment to community health, ChristianaCare today announced a $1.6 million investment in 25 local nonprofits, unveiling the recipients of its Community Investment Fund during a special celebration at The Ministry of Caring in Wilmington. Since 2019, ChristianaCare’s Community Investment Fund has provided more than $5.6 million to 64 organizations, addressing social, behavioral and environmental health factors. ”ChristianaCare is empowering and supporting our nonprofit partners so they can help meet the many needs of the people they serve, and work with us to improve patient health and create healthy communities and a healthy Delaware,” said Bettina Tweardy Riveros, chief health equity officer at ChristianaCare. This year’s recipients received funding to support health improvement initiatives in neighboring communities and address critical issues and community needs. “Each of these recipients is making a significant and positive impact by addressing critical health challenges throughout our communities, including food insecurity, housing insecurity and environmental health. At ChristianaCare, we are honored to be joining forces with these 25 organizations to provide them with more resources so that they do more for those in need. It is another way we care for our community,” she said. The funded initiatives will be implemented throughout the upcoming year and were selected based on the quality of applicants’ proposals and implementation plans, and on the alignment of their proposals with the critical issues prioritized by the community in ChristianaCare’s Community Health Needs Assessment and Community Health Implementation Plan. Recipient Spotlight: Healthy Food for Healthy Kids "The impact of ChristianaCare’s 2024 Community Investment Awards funds on Healthy Foods for Healthy Kids will be felt not only in 2025 but for years to come. This funding will expand our program to an additional school, serving over 600 more students, and support data and research for future growth." Healthy Food for Healthy Kids, Lydia Sarson, Executive Director. Recipient Spotlight: Project New Start “Approximately 85% of the justice-involved individuals served by Project New Start are housing and food insecure. With ChristianaCare’s 2024 Community Investment Fund Award to Project New Start, which began 11/01/24, we have already been able to assist 23 individuals with clothing and household goods; 20 individuals with transportation assistance; 17 individuals with food support; and 7 individuals with housing as of 12/31/24. The impact of these funds cannot be overstated as this investment by ChristianaCare provides Project New Start the means to provide the critical basic needs an individual requires to live with dignity without the trauma of worrying about where they will sleep, how they will eat and how they can sustain employment. We are so grateful to ChristianaCare for their ongoing support.” Priscilla Turgon, Founder and Executive Director of Project New Start, Inc. Recipient Spotlight: YMCA of Delaware - Central YMCA Supportive Housing Program “The Central YMCA Supportive Housing Program, in partnership with Christiana Care, serves low-income men at risk of homelessness who often face trauma, addiction, disabilities or lack of family support. Through stable housing, nutritious meals, welcome packages, rental assistance and supportive activities, the program fosters community wellbeing, improves health outcomes, prevents homelessness and empowers residents to achieve self-sufficiency.” Jimia Redden, Executive Director of Housing. This year’s Community Investment Fund recipients are: • AIDS Delaware: AIDS Delaware’s mission is to eliminate the spread and stigma of HIV/AIDS, improve the lives of those living with HIV/AIDS and promote community health through comprehensive and culturally sensitive services, education programs and advocacy. • Black Mothers in Power: Black Mothers in Power seeks to eradicate racial health disparities for Black birthing people and Black babies throughout Delaware. • Boys & Girls Club of DE: Boys & Girls Clubs of Delaware inspires and enables young people, especially those most in need, to reach their full potential as productive, responsible, caring citizens. • Children and Families First DE: Children & Families First is one of Delaware's oldest and most trusted non-profit leaders in providing the supports and services children and their families need to thrive. • Claymont Community Center - Brandywine Resource Council: Claymont Community Center is a base for a variety of community organizations supporting educational, social, recreational, cultural, personal development, financial and wellness needs. • Delaware Center for Horticulture: The Delaware Center for Horticulture cultivates greener communities by inspiring appreciation and improvement of the environment through horticulture, education and conservation. • Delaware Futures, Inc: Delaware Futures empowers at-promise high school and middle school youth across the state of Delaware by providing year-round, trauma-informed curricula tailored to students at each grade level. • Delaware Nature Society: Delaware Nature Society connects people and nature to create a healthy environment for all through education, conservation and advocacy. • Do Care Doula: Do Care Doula provides grant-funded Doula training and development, subsidized Doula support and a variety of community outreach programs. • Healthy Food for Healthy Kids: Healthy Food for Healthy Kids supports educators in Delaware, bringing life-lasting benefits of gardening and good nutrition to kids. • Jefferson Street Center: The mission of JSC is to advance community-driven priorities in Northwest Wilmington that promote the conditions necessary for all residents to thrive. • Latin American Community Center: LACC seeks to empower members to become contributing members of society through advocacy and offers programs and services to anyone ages of one to 101. • Milford Housing Development Corporation: Milford Housing Development Corporation is a value-driven, nonprofit, affordable housing developer, providing services throughout Delaware. Its mission is to provide decent, safe, affordable housing solutions to people of modest means. • Ministry of Caring: Since Brother Ronald began the ministry in 1977 with the first shelter for homeless women on the Delmarva Peninsula, the Ministry has worked ceaselessly to ease the needs and struggles of our neighbors. • ONCOR Coalition: ONCOR’s vision is to build and promote spaces that connect people to the city and each other. It promotes positive relationships through community-based educational programs and recreational opportunities. • Our Daily Bread Dining Room of MOT: ODB is the only soup kitchen in the Middletown, Odessa and Townsend region. ODB is a volunteer run organization with over 300 volunteers. Volunteers help purchase and pick up food and ingredients, prepare and serve meals and clean and maintain the facility. • Project New Start: Project New Start provides a comprehensive cognitive behavioral change/workforce development initiative for individuals transitioning out of state and federal institutions. • Ray of Hope Mission Center: Ray of Hope’s mission is to recognize and address the needs of those who are struggling within our community and assist them in their efforts to provide for themselves and their families, both physically and spiritually. • St. Patrick's Center: Serving people in Wilmington’s East Side neighborhood since 1971, St. Patrick’s Center is a nonprofit organization that operates a Senior Center, and provides meals, groceries, clothing, paratransit and social service support to the public. • The Resurrection Center: The purpose of the Resurrection Center is to spread the gospel of Jesus Christ and create a spirit-filled environment that hungers for the Gospel and to serve as liberating agents in the midst of the world. • Voices of Hope: Voices of Hope’s mission is to empower lives and foster recovery. The nonprofit is dedicated to supporting individuals and families facing substance use disorder. Through compassion, education and community engagement, Voices of Hope strives to break the chains of addiction, promoting a healthier, brighter future for all. • West End Neighborhood House: At West End Neighborhood House, staff, clients, volunteers and donors work together to resolve complex social challenges throughout Delaware. Through outcomes-driven programming, the West End Neighborhood House provide support that meets community needs in finances, housing, education, employment and family services. • Westside Family Healthcare: Westside Family Healthcare is a community-minded, non-partisan health center located in Delaware. Westside opened its doors in 1988 and has maintained status as a Federally Qualified Health Center since 1994. • Wilmington HOPE Commission Inc.: The Hope Commission is a reentry program that helps formerly incarcerated men return to their community. It offers support services that address factors known to lead to repeat offenses. • YMCA of Delaware: The Central YMCA Supportive Housing Program offers housing for men aged 18 and older. Residents benefit from dorm-style accommodations, discounted access to the fitness center and connections to a range of health and human service providers in partnership with the YMCA.

I Was 33 Years Early to the ADU Party

The early 1990s were tough for many Canadians, including my partner and me. The recession of 1990-1991 hit us hard, leaving both of us without jobs and staring at an unemployment rate that had climbed to a record 10.23%. With bills piling up and options dwindling, we had to get creative—and fast. That’s when we found an unexpected lifeline in an unlikely place: my partner’s grandmother’s house. Grandma, a 90-year-old fireball from Newfoundland, was sharp as a tack and fiercely independent. However, her home was starting to feel too large for her to manage on her own. Meanwhile, we needed a place to live that wouldn’t drain our limited savings. Over cups of tea at her cozy kitchen table, a plan started to take shape: we would build a basement apartment in her house, move in, and exchange affordable rent for assistance around the house. It was a perfect win-win. I didn't know it, but I was an ADU pioneer Today, this living arrangement may be recognized as an Accessory Dwelling Unit (ADU), a secondary housing unit on a single-family property. However, in 1991, this concept was far from mainstream. For us, it was simply a matter of survival—a practical solution born from necessity. We rolled up our sleeves and got to work. With a few friends and determination, we transformed Grandma’s basement into a modest but functional living space. It was basic, even a bit wonky—you had to walk through the bedroom to get to the living room-kitchen combo—but it was ours. We managed most of the construction ourselves, and hired an electrician for the wiring and a plumber to handle the pipes. The rest was pure sweat equity. Living in that basement was an adjustment, to say the least. Space was tight, and our DIY craftsmanship wasn’t exactly HGTV-worthy. However, it provided us with a fresh start. But as ADU pioneers, we got much more than we could have imagined. A much closer connection to family. Grandma’s wit and energy were the heart of the house, and we grew closer to her than we ever imagined. Her stories about growing up in Newfoundland in the late 1800s mesmerized me. I would sit there, wide-eyed, as she recounted winters so cold that tea froze before it hit the cup and evenings illuminated by whale oil lamps. We laughed constantly, and she quickly became the grandmother I never had since my grandparents had passed before I was born. Grandma and I stayed close even after my relationship with my partner ended. I couldn’t imagine life without our Friday lunches, which became a cherished tradition. Every week, I’d visit, and she’d share more stories or critique my cooking attempts with her quick wit and that unmistakable Newfoundland twang. She continued to be a beacon of joy and wisdom in my life. Grandma thrived on independence, which she held onto with great determination. At 90 years old, she re-tarred her driveway by herself, much to the neighbours' surprise and my immense admiration. The tar application was as wrinkled as her skin, and she couldn't care less. She beamed with pride while I took her picture! She loved having visitors, and the parish clergy were frequent guests. She always welcomed them with a twinkle in her eye and a sharp sense of humour. Once, when the parish priest asked her if she ever thought about "the hereafter," she shot back, “Oh, I think about it every day when I go into the basement and ask myself, ‘What am I here after?’” That was Grandma: quick-witted, strong, and full of life. Our basement apartment was more than just a place to live; it was a lifeline. The benefits extended beyond us. Grandma stayed in the home she loved until she passed away peacefully at 96 years old, sitting at her kitchen table on my birthday. It was a poignant moment that reminded me how much she had shaped my life. The modest basement apartment not only sheltered us but also added value to her home. We inadvertently enhanced the property’s functionality and appeal by converting unused space into livable quarters. This represents a key advantage of ADUs in today’s economy. Given the housing shortages and rising costs, ADUs provide a practical solution by offering affordable rental options, increasing property values, and creating opportunities for intergenerational living. In recent years, governments have acknowledged the importance of ADUs, making it easier and more affordable for families to construct them. Changes to mortgage lending policies have been introduced to promote ADU construction. For instance, insured loans now cover up to $1.5 million, and the amortization period has been extended to 30 years, enhancing financing accessibility. Furthermore, the federal government has announced new refinancing options to allow up to 90% of the property’s value. At the same time, low-interest loans for ADU construction have doubled to $80,000, with repayment terms of 15 years. These welcome changes will lower financial barriers and assist homeowners in creating secondary housing units, addressing both affordability and housing shortages. This intergenerational arrangement we set up over three decades ago was a win-win in every way. It provided mutual support, strengthened family bonds, and created a housing solution that benefited both generations. Seniors can age in place with dignity and companionship while younger generations gain access to affordable housing and the chance to learn from their elders. The laughter, shared meals, and stories crafted memories that will last a lifetime. Moreover, ADUs can help ease housing shortages and increase the availability of affordable rentals. They represent a practical, cost-effective method to utilize existing properties better. For families, they offer flexibility—a space for aging parents, adult children, or even potential rental income. For communities, they supply essential housing stock without necessitating large-scale development. For a deeper dive into ADUs, here's a link to a post we shared last year https://expertfile.com/spotlight/10346/additional-dwelling-units--adus- What's Old is New Again It's often said that many things come back in style if you wait long enough. This may hold for ADUs, simply an old concept whose time has come again. Nonetheless, ADUs empower our younger generation to afford housing and achieve homeownership. They also provide vital support for our older generations, enabling them to age in place while generating much-needed income for a dignified retirement. Reflecting on the past, I often ponder who saved whom. Grandma’s indomitable spirit and sharp humour made every bump in the road worthwhile. She would tease me about the crooked shelves we installed and joke that our kitchen was so small we could stir the soup without getting off the couch. In truth, she gave me more than I ever gave her. Her strength, love, and unwavering sense of humour helped me navigate one of the most challenging times in my life. The quirky basement we built in 1991 may not have been perfect, but it served its purpose. Today, as ADUs gain popularity, they represent more than just housing; they embody connection, resilience, and finding creative solutions to life’s challenges. Whether it’s a basement apartment, a backyard cottage, or a garage conversion, ADUs can foster connection and help families thrive—just as we did all those years ago. And as for Grandma? She demonstrated that a touch of humour, plenty of love, and the occasional jab at a priest could keep anyone young at heart. Every time I think of her now, I can’t help but smile and wonder if, somewhere, she’s still re-tarring driveways and asking herself, ‘What am I here after?’ Don’t Retire … Re-Wire! Sue

Additional Dwelling Units (ADUs)

Summary: In a previous post, I wrote about the need for more creative solutions to the cost of housing. I also spoke to the housing shortage and the steep downpayment rules we continue to face. At the same time, the need for retirement income and an increased focus on "aging in place" has more and more property owners looking for solutions. Here, we explore why adding secondary living spaces to their properties, commonly referred to as Additional Dwelling Units (ADUs), is something you may want to consider. What Are ADUs? ADUs are fully equipped residential units situated on the same lot as a single-family home. They offer a distinct and private living arrangement while maintaining proximity to the main house. These living spaces may be integrated into the primary residence—such as a transformed garage or basement—or exist as independent structures, including small cottages or apartments. Why ADUs Are Gaining in Popularity ADUs can fulfill a broad range of needs, from accommodating aging relatives or adult children to creating a valuable source of rental income for homeowners. This income could assist seniors with cash flow and substantially boost their property's overall value. But is an ADU right for you? Before answering this, let's first take a brief look at their advantages and the rules and regulations governing the conversion or construction of such structures. Types of ADUs ADUs encompass a variety of secondary suites or dwelling units, primarily categorized as attached, detached, and semi-detached structures. Attached ADUs arise when homeowners convert existing spaces, such as basements, into livable areas. In contrast, detached ADUs consist of separate structures built apart from the principal residence. Laneway Houses / Laneway Suites: These small, detached units are constructed in the backyard or along the laneways of existing properties, maximizing the use of available space. Garden Suites: Similar to laneway houses, garden suites are secondary residences in the primary home's backyard. They offer self-sufficient living environments and are increasingly favoured for boosting housing density in urban settings while preserving the character of residential neighbourhoods. Basement Apartments: Self-contained living spaces in the basement of a residential property. These usually have a distinct entrance. In-law Units (In-law Suites, In-law Flats) are separate living sections within a single-family home that cater to relatives, providing a comfortable space for parents or in-laws. Detached Garages: These standalone structures are separate from the main house and traditionally store vehicles. They can also serve as storage areas or workshops. Adding a second-story apartment above garages is popular. Parking is premium in cities, and these structures provide the best of both worlds: keeping parking, storage, and adding living quarters above. Carriage Houses and Coach Houses: Originally designed as outbuildings on larger estates to store horse-drawn carriages, carriage houses, and coach houses have often been repurposed as living accommodations, guest houses, or rental units while maintaining their historic architecture. The Benefits of ADUs Additional Dwelling Units (ADUs) are indispensable in alleviating housing shortages and addressing affordability challenges within various communities. They also offer a wide range of personal and economic advantages for homeowners and tenants searching for budget-friendly rental options. Some key benefits include: An Aging-in-Place Option for Seniors: ADUs can allow elderly relatives to stay in their community and maintain an important sense of connection with neighbours, friends, and family. Rental Income: Homeowners can establish a dependable revenue stream with an ADU. These units represent a highly appealing affordable housing alternative. Accommodation for Adult Children: An ADU can provide temporary living arrangements to adult children who may not be able to buy into the housing market or who want to be closer to their aging parents. Dedicated Office/Creative Space: With more people working from home part-time or going entirely virtual, ADU can provide a more professional and comfortable work environment But There's Another Payoff for ADUs Beyond these apparent benefits, I'm also struck by how ADUs can help us cultivate a stronger sense of community and intergenerational connection. Let me unpack this more and list some unique attributes of ADUs that make them so vital to our housing strategy: Affordability: ADUs can also be more affordable than standalone houses, making them increasingly attractive for individuals or small families looking for budget-conscious living options. Connection: ADUs are much closer to the primary residence. This allows younger renters to forge more meaningful relationships and interactions with their homeowners (many of whom are seniors). Equity: For renters who want to move beyond an apartment or condo but lack the financial means, ADUs could present a great alternative. They also provide a unique way to give renters access to neighbourhoods where housing availability is a challenge. For young families, renting an ADU could allow them to place their children in better schools that require residency in the school district. Support: As we age, we are more likely to need help maintaining our homes. For example, help with yard work and snow removal could be traded for reduced rent. There is much to be said about the comfort and safety of having someone live a few steps away for our older generation. ADUs are a Key Part of the Government's Housing Strategy The Federal Government just announced the expansion of the Canada Secondary Suite Loan Program. Here's what you need to know: The loan amount has been increased to $80,000, and it has a 2% interest rate and a 15-year repayment term. In addition to the Secondary Suite Loan Program, homeowners can refinance with insured mortgages to help cover the cost of adding a secondary suite, starting January 15, 2025. Lenders and insurers will begin allowing mortgage refinancing of up to 90 percent of the post-renovation value of their home up to $2 million, amortized for up to 30 years. Homeowners can use this loan program and mortgage financing to help cover the cost of adding a secondary suite. These developments should get us all thinking more about the possibilities of ADUs. The benefits for many people and the clear intergenerational win-win exchanges are compelling. Given the impact they could yield for seniors in unlocking the value of their home equity and the compelling social benefits they offer for communities, I'll be exploring ADUs in much more detail over the coming year. Stay tuned. Don’t Retire … Re-Wire! Sue

Drops in the Bank of Canada rate will not solve housing affordability.

Summary: The Bank of Canada’s interest rate cuts won’t resolve Canada’s housing affordability crisis. Factors such as skyrocketing home prices, unaffordable down payments, and stagnant wage growth are other primary challenges to address. A personal example offered by the author shows how the price of her Toronto home surged over 1,000% from 1983 and 2024 while her wages during the same period rose only 142%. While some see this issue as a consequence of Baby Boomers remaining in their homes, it's more nuanced than that. We have systemic barriers in Canada that necessitate targeted policy changes. It’s time to tackle affordability and implement effective solutions. The Bank of Canada met today, to determine interest rates for the last time this year. They announced a drop of .50 basis points. This is part of a broader effort to stimulate economic growth in Canada, which faces challenges, especially a softening labor market and persistent inflation. Why Should You Care? Interest rates determine how affordable our debt will be and what return we can expect on our savings. Since mortgages represent most consumer debt, interest rates directly impact affordable housing costs, making them very newsworthy. However, interest rates only tell part of the story. When the Bank of Canada lowers its rate, it primarily impacts variable-rate mortgages. These are tied directly to the BoC's overnight rate, so a rate cut can reduce the interest costs on these loans. Homeowners with variable rates would likely see a reduction in their payments, with more of their payments going toward principal rather than interest. People without debt and savings (primarily seniors) will see a drop in their investment returns. In contrast, fixed-rate mortgages, which are not directly tied to the BoC's rate, are influenced more by the bond market, particularly the 5-year government bond yield. The current trend in bond yields suggests that fixed mortgage rates could also decrease over time. Let’s pause here and talk about the affordability of houses and how interest rates are not the reason housing is out of reach for most first-time buyers. A walk down memory lane might offer some perspective. I purchased my first home in the fall of 1983 for $63,500 (insert head shake). I was 27 years old, and before you do the math, yes, I am a Baby Boomer. My first serious (so I thought) live-together relationship had just ended, and I was looking for a place to live. I had finished school and had a good full-time job with Bell Canada. A rental would have been preferred, except I had a dog. Someone suggested that I buy a home. I did not know very much about purchasing real estate or homeownership, for that matter. But I was young and willing to learn. I had been working full-time for two and a half years. During my orientation at Bell Canada, my supervisor told me to sign up for their stock option program. She said I would never miss the money or regret signing up for the plan. She was right. When I purchased my home, there was enough money in my stock account for a down payment and closing costs. My interest rate was a terrifying 12.75%, yielding a mortgage payment of just under $670 monthly. The lender deemed this affordable based on my $18,000 annual wage. Life was good. This was in 1983, when the minimum down payment for a home purchase in Canada was typically 10% for most buyers. However, a lower down payment could be possible with mortgage insurance (provided by organizations like Canada Mortgage Housing Corporation (CMHC), which allowed buyers to put down as little as 5%, provided they qualified for insurance. This was commonly available for homes under $150,000, with stricter terms for higher-priced homes. If you had a higher down payment of 25% or more, mortgage insurance wasn't required, and you could avoid extra costs associated with insured mortgages. This was part of broader efforts by the government to make homeownership more accessible, especially amid the high interest rates of the time. So let's do the math. Circa 1983 I first needed to prove that I had saved $3,175 in down payments and $953 in closing costs for $4128. In the 2.5 years I worked at Bell Canada, I saved $4,050 (including Bell Canada’s contribution) in stocks. I also had another $5,000 in my savings account. $9,000 was enough to complete the transaction and leave me with a healthy safety net. Fast forward to 2024 Let’s compare what the same transaction would look like today. Using the annual housing increase cited on the CREA website, the same house would be valued at approximately $700,000 today. Interest rates are much lower today, at 4.24%, yielding a mortgage payment of $3,545. 1. The down payment rules have changed. For the first $500,000, The minimum down payment is 5%. 5% X 500,000=25,0005\% \times 500,000 = 25,0005% X 500,000 = $25,000 2. The minimum down payment for the portion above $500,000 is 10%. 10% X (700,000−500,000) = 20,00010\% \times (700,000 - 500,000) = 20,00010% X (700,000−500,000) = $20,000 3. Total minimum down payment: 25,000+20,000 =4 5,00025,000 + 20,000 = 45,00025,000+20,000 = $45,000 Thus, the minimum down payment for a $700,000 home is $45,000. Here is the comparison: 1983 Scenario 2024 Scenario Variance Purchase Price: $63,500 $700,000 up 1002% Down Payment: $3,175 $45,000 up 1317% Loan Amount: $60,325 $655,000 up 986% Interest Rate: 12.75% 4.24% down 200% Monthly Mortgage Payment: $670 $3,545 up 429% Wage: $18,000 $43,500 up 142% Gross Debt Service Ratio: 44.6% 97.8% up 119% Time to Save for Down payment: 2 years 12.4 years up 520% *Please note that this example does not include mortgage insurance The real problem As you can see, housing was much more affordable for me in 1983 and far from cheap in 2024. During the past 41 years, wages have increased by 142%, yet interest rates have dropped by 200%. But the most significant impact on affordability has been the over 1,000% increase in housing prices. So why is all the focus on interest rates? At the risk of oversimplifying a complicated issue, I believe the media often uses interest rates as a "shiny penny" to capture attention, diverting focus from deeper housing affordability issues. This keeps the spotlight on inflation and monetary policy, aligning with economic agendas while ignoring systemic problems like down payment barriers and the shortage of affordable homes. Indeed, a movement in interest rates often has an immediate and noticeable impact on borrowers' affordability, making it a hot topic for news and policymakers. However, the frequency and consistency of the Bank of Canada meetings on interest rates give the impression that rates are the primary issue, even though they are just one part of a complex system. For example, even if the Bank of Canada dropped interest rates below zero, it would do little to solve today’s homeownership affordability issue. The real problems: 1. Down Payment Challenges: With housing prices skyrocketing, the 5%- 20% down payment required has become insurmountable for many, particularly younger buyers. High rents, stagnant wage growth relative to home prices, and rising living costs make saving nearly impossible. 2. Lack of Affordable Starter Homes: Due to profitability and zoning restrictions, housing developments often prioritize larger, higher-margin homes or luxury condos over affordable single-family starter homes. 3. Misplaced Generational Blame: Blaming Baby Boomers for "holding onto homes" oversimplifies the issue. They are staying put due to limited downsizing options, emotional attachments, or the need for housing stability in retirement, not a desire to thwart younger generations. 4. Political Challenges: Addressing structural issues like zoning reform or incentivizing affordable housing construction requires political will and collaboration, which can be slow and contentious. A broader lens is needed to understand and address the actual barriers to home ownership. Interest drops are merely a band-aid solution that misses the central issue of saving a down payment. The suggestion that we have an intergenerational issue needs to be revised. The fact that Baby Boomers are holding on to their homes should not surprise anyone. However, Real Estate models that predicted copious numbers of Baby Boomers selling their homes to downsize got it wrong. Downsizing was a concept conceived in the 1980s. Unfortunately, it did not account for record-setting home price increases or inflation, leaving it undesirable for today’s seniors. Although this is a complex issue, a few suggested solutions are worth exploring. What can be done? Focus on Policy Innovations: To create housing, increase supply, curb speculative investments, and provide targeted assistance for builders to build modest starter homes. To create rentals, homeowners should also receive income tax incentives to build Accessory Dwelling Units (ADUs). These could be used as affordable rentals or to house caregivers for senior homeowners. Today, The federal government announced a doubling of its Secondary Suite Loan Program, initially unveiled in the April 2024 budget. This is a massive step in the right direction. To create down payments, adopt a policy allowing first-time home buyers to avoid paying tax on their first $250,000 of income. Then, they could use the tax savings as a down payment. Focus on Education and Advocacy: Include a warning that helps consumers understand that withdrawing from RSPs results in a significant loss of compound interest related to withdrawals and how this can harm income during retirement. Encourage early inheritance to create gifted down payments. Normalize the concept by emphasizing the benefits to the giver and the receiver. Educate the public on using financial equity safely and create down payments as an early inheritance for their heirs. This will shift the conversation and initiate an intergenerational transfer of wealth that empowers the next generation to own a home. The Bottom Line While the Bank of Canada interest rate cut may ease some financial strain for homeowners with variable-rate mortgages, it will do little to address the core issue of housing affordability. The media's fixation on interest rates as a "shiny penny" distracts from more profound systemic barriers, such as the inability to save for a down payment and the lack of affordable housing stock. These challenges require targeted policies, structural reforms, and intergenerational collaboration to be tackled effectively. The focus must shift from short-term rate adjustments to long-term solutions that prioritize accessibility and affordability in housing. Without meaningful action, homeownership will remain out of reach for many, perpetuating the cycle of financial inequity across generations. Dont't Retire... Re-Wire! Sue

NYS Budget Provisions May Protect Incumbent Democrats

Lawrence Levy, associate vice president and executive dean of the National Center for Suburban Studies, was interviewed by City & State New York about how Governor Kathy Hochul’s budget and focus on issues like affordable housing and retail theft may provide some protection for incumbent Democrats this November. The state budget may be designed to insulate Democrats from Republican attacks, but it’s not clear that it will be the deciding factor in various races. The 2024 election cycle is an entirely different beast than 2022. Two years ago, Hochul was at the top of the ticket in New York. This year, she’s not even on the ballot. That may actually be a boon for Democrats, as many observers credited her lackluster performance with negatively impacting races down ballot and the latest Siena College polling has her favorability and job approval ratings at all-time lows. Hochul notably did not stump for Suozzi during his high-profile race in February despite her role as de facto head of the state Democratic Party. And in the weeks following the state budget, she has only visited a swing district to celebrate her policy successes in the spending plan once. Instead, President Joe Biden and Donald Trump will be at the top of the ticket, and any thoughts about the specific policies included in the state budget could be reflected by voters’ sentiments about the two presidential candidates. “With the presidential campaign at the top of the ticket, I don’t think what Hochul does, or doesn’t do, will make a particular difference in any of the competitive congressional races,” said Lawrence Levy, executive dean of the National Center for Suburban Studies at Hofstra University. “Yes, she may be cited by Republicans along with several other high-profile Democrats as supposedly insensitive to their constituents on housing and crime, to see if that still sticks, but mostly it’s going to be about Trump and Biden.” May 13 - City and State New York Covering New York politics - we have experts ready to help with any of your questions and stories. Lawrence Levy is the Executive Dean of the National Center for Suburban Studies at Hofstra University. He's available to speak with media - simply click on his icon now to arrange an interview today.

Healthy Environment, Healthy People: The Intersection Between Climate and Health

How is climate change influencing our health? Why does climate change have a greater impact on vulnerable populations and low-income people? How does the U.S. health care system affect the climate? How can health care systems improve their impact on the climate and the environment? ChristianaCare’s inaugural Climate and Health Conference addressed these topics and raised possible solutions at the John H. Ammon Medical Education Center on the Newark, Delaware, campus on April 12. At the conference, the common denominator was this: An unhealthy environment can lead to illnesses and deaths from air pollution, high heat, contaminated water and extreme weather events. Health systems, government entities, community organizations and individuals all have a role to play in decreasing these effects. “Climate, the environment and health care systems are intertwined,” said Greg O’Neill, MSN, APRN, AGCNS-BC. “We need to pay close attention to this relationship so we can improve health for everyone.” O’Neill is director of Patient & Family Health Education and co-chair of the Environmental Sustainability Caregiver Committee at ChristianaCare. Climate change and intensifying health conditions Negative health effects are so closely tied to the environments where people live, work and play that The Lancet called climate change “the greatest global health threat facing the world in the 21st century [and] the greatest opportunity to redefine the social and environmental determinants of health.” At the conference, speakers addressed specific areas of concern. Asthma. Air pollutants, while largely invisible, are associated with asthma. What’s more, people who live in urban areas with little green space are more likely to have uncontrolled asthma, said speaker Robert Ries, M.D., an emergency medicine resident at ChristianaCare. And there’s the rub, he said: When people with asthma spend time in green spaces, it may improve their health. “In Canada,” he said, “some doctors prescribe nature – two hours a week for better overall health outcomes. Could we do that here?” Heat-related illness. Temperatures worldwide have been rising, increasing the likelihood of heat-related health incidents. Heat waves may be harmful to children and older adults, particularly those who don’t have access to air conditioning, swimming pools or transportation to the beach, said speaker Alan Greenglass, M.D., a retired primary care physician. Children visit the emergency room 20% more frequently during heat waves. Weather-related illness. Climate change is causing more floods, which may result in respiratory problems due to mold growth; and droughts, which may threaten water safety and contribute to global food insecurity, said speaker Anat Feingold, M.D., MPH, an infectious disease specialist at Cooper Health. Stress and anxiety. Climate change can affect mental health, even leading to “solastalgia,” which is distress about environmental change and its effect on one’s home, said speaker Zachary Radcliff, Ph.D., an adolescent psychologist at Nemours. He encouraged clinicians in the audience to keep this mental health concern in mind when seeing patients as it may become more prevalent. Cardiovascular disease risk. Frequent consumption of red meat increases the risk of cardiovascular disease, the top cause of death in the U.S. It’s also unhealthy for the environment, said speaker Shirley Kalwaney, M.D., an internal medicine specialist at Inova. Livestock uses 80% of available farmland to produce only 17% of calories consumed, creating a high level of greenhouse gas emissions. By comparison, plant-based whole foods decrease the risk of cardiovascular disease and diabetes. They use only 16% of available farmland, producing 82% of calories consumed. This makes reducing red meat in our diets one of the most powerful ways to lower the impact on our environment. Health equity and the environment People in low-income communities are more likely to live in urban areas that experience the greatest impacts of climate change, including exposure to air pollutants and little access to green space, said speaker Abby Nerlinger, M.D., a pediatrician for Nemours. A Harvard study in 2020 demonstrated that air pollution was linked with higher death rates from COVID-19 — likely one of the many reasons the pandemic has disproportionally harmed Black and Latino communities. Similarly, access to safe, affordable housing is essential to a healthy environment, said Sarah Stowens, Ed.D., manager of State Policy and Advocacy for ChristianaCare, who advocated for legislation including the Climate Solutions Act, another bill that increased oversight regarding testing and reporting of lead poisoning and a policy to reduce waste from topical medications. Opportunities for change in health care Reduce emissions from pharmaceuticals and chemicals. These emissions are responsible for 18% of a health system’s greenhouse gas emissions. One way to reduce this number is for clinicians to prescribe a dry-powder inhaler (DPI) instead of a metered-dose inhaler (MDI) when applicable and safe for the patient and to give patients any inhalers that were used in the hospital at discharge if they are going home on the same prescription. Hospitals have opportunities to reduce greenhouse gases while caring for patients, said Deanna Benner, MSN, APRN, WHNP, women’s health nurse practitioner and co-chair of ChristianaCare’s Environmental Sustainability Caregiver Committee. The health care sector is responsible for 8.5% of U.S. greenhouse gas emissions, the highest per person in the world. U.S. greenhouse gas emissions account for 27% of the global health care footprint. One way to significantly reduce the carbon footprint is to use fewer anesthetic gases associated with greater greenhouse gas emissions, Benner said. Limit single-use medical devices. Did you know that one surgical procedure may produce more waste than a family of four produces in a week? Elizabeth Cerceo, M.D., director of climate health at Cooper Health, posed this question during her talk. Sterilizing and reusing medical devices, instead of using single-use medical devices, she said, may meaningfully reduce hospital waste. ChristianaCare’s commitment to healthy environments and healthy people As one of the nation’s leading health systems, ChristianaCare is taking a bold, comprehensive approach to environmental stewardship. ChristianaCare reduced its carbon footprint by 37% in 2023 by purchasing emission-free electricity. ChristianaCare joined the White House Climate Pledge to use 100% renewable energy by 2025, reduce greenhouse gas emissions by 50% by 2030 and achieve zero net emissions by 2050. ChristianaCare has created an Environmental, Social and Governance structure to help advance a five-year strategic plan that delivers health equity and environmental stewardship. Nearly 150 staff members have become Eco-Champions, an opportunity to be environmental change-leaders in the workplace. In 2023, ChristianaCare’s successful environmental stewardship included: Reducing our carbon footprint by 37% by purchasing emission-free electricity. Recycling 96,663 pounds of paper, which preserved 11,485 trees. Reducing air pollution by releasing an estimated 33,000 fewer pounds of nitrogen oxides and sulfur oxides through the use of a cogeneration energy plant on the Newark campus. Donating 34,095 pounds of unused food to the Sunday Breakfast Mission in Wilmington, Delaware. Donating 1,575 pounds of unused medical equipment to Project C.U.R.E., ChristianaCare’s Virtual Education and Simulation Training Center and Delaware Technical Community College. “In quality improvement, they say you improve the things that you measure,” O’Neill said in expressing goals for continued success. In looking ahead, said Benner, “I really hope that this conference is the catalyst for positive change with more people understanding how climate is connected to health, so that we can protect health from environmental harms and promote a healthy environment for all people to thrive.”

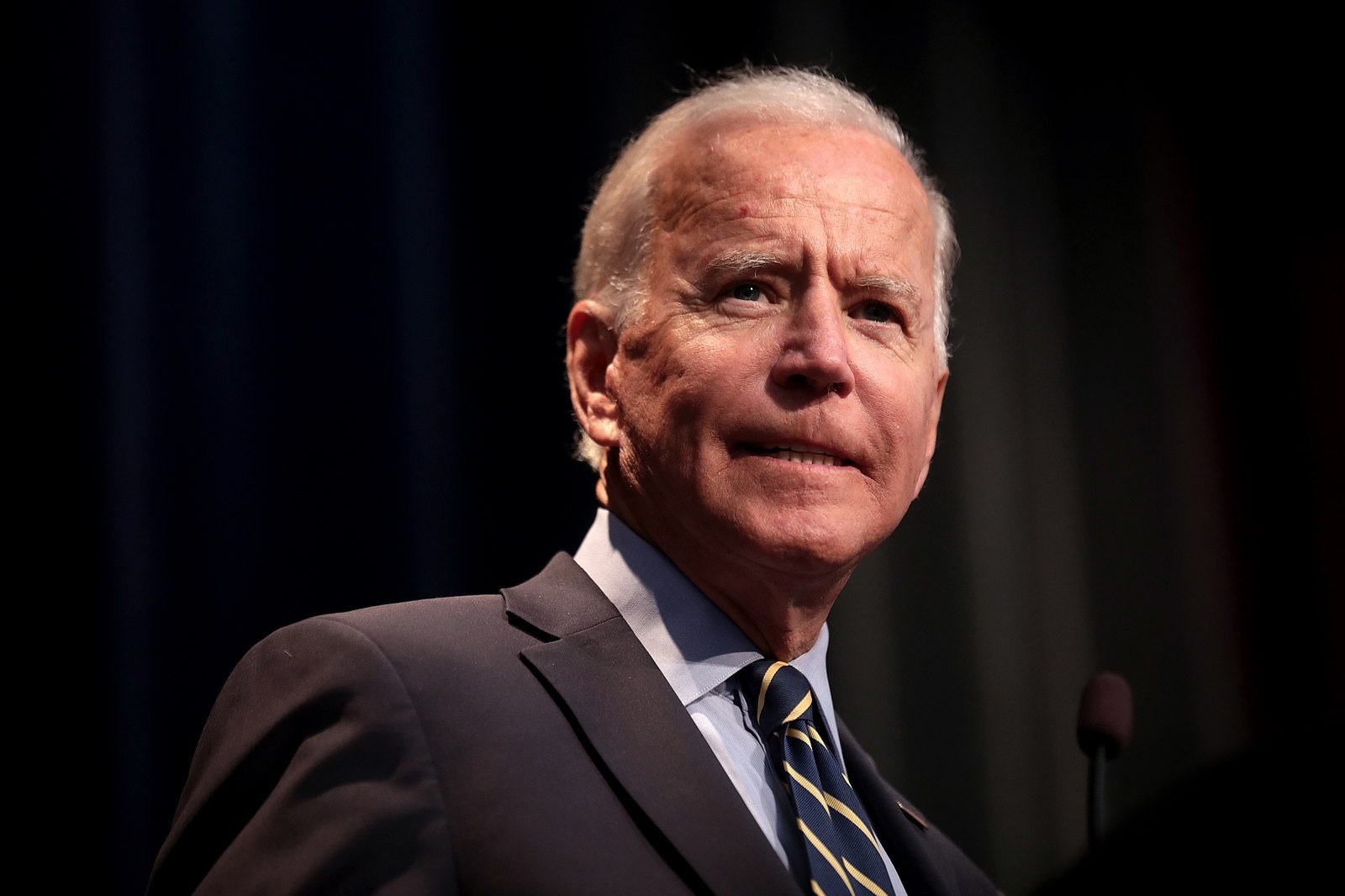

Will Biden’s Plan to Resettle Afghans Transform the U.S. Refugee Program?

Among the high-profile anti-immigration policies that characterized the four years of Donald Trump’s presidency was a dramatic contraction in refugee resettlement in the United States. President Biden has expressed support for restoring U.S. leadership, and increased commitment is needed to help support the more than 80 million people worldwide displaced by political violence, persecution, and climate change, says UConn expert Kathryn Libal. As Libal writes, with co-author and fellow UConn professor Scott Harding, in a recent article for the Georgetown Journal of International Affairs, the rapid evacuation of more than 60,000 Afghans pushed the Biden administration to innovate by expanding community-based refugee resettlement and creating a private sponsorship program. But more resources are needed to support programs that were severely undermined in previous years and to support community-based programs that help refugees through the resettlement process: Community sponsorship also encourages local residents to “invest” in welcoming refugees. Under existing community sponsorship efforts, volunteers often have deep ties to their local communities—critical for helping refugees secure housing, and gain access to employment, education, and health care. As these programs expand, efforts to connect refugees to community institutions and stakeholders, which are crucial to help facilitate their social integration, may be enhanced. As Chris George, Executive Director of Integrated Refugee and Immigrant Services in New Haven, Connecticut, has observed, “It’s better for the refugee family to have a community group working with them that knows the schools and knows where to shop and knows where the jobs are.” As more local communities take responsibility for sponsoring refugee families, the potential for a more durable resettlement program may be enhanced. In the face of heightened polarization of refugee and immigration policies, community sponsorship programs can also foster broad-based involvement in refugee resettlement. In turn, greater levels of community engagement can help challenge opposition toward and misinformation about refugees and create greater public support for the idea of refugee resettlement. Yet these efforts are also fraught with significant challenges. Sponsor circle members may have limited capacity or skills to navigate the social welfare system, access health care services, or secure affordable housing for refugees. If group members lack familiarity with the intricacies of US immigration law, helping Afghans designated as “humanitarian parolees” attain asylum status may prove daunting. Without adequate training and ongoing support from resettlement agencies and caseworkers, community volunteers may experience “burn out” from these various responsibilities. Finally, “successful” private and community sponsorship efforts risk providing justification to the arguments of those in support of the privatization of the USRAP and who claim that the government’s role in resettlement should be limited. Opponents of refugee resettlement could argue that community groups are more effective than the existing public–private resettlement model and seek to cut federal funding and involvement in resettlement. Such action could ultimately limit the overall number of refugees the United States admits in the future. December 11 - Georgetown Journal of International Affairs. If you are a journalist looking to know more about this topic – then let us help with your coverage and questions. An associate professor of social work and human rights, Kathryn Libal is the director of UConn's Human Rights Institute and is an expert on human rights, refugee resettlement, and social welfare. She is available to speak with media – click on her icon now to arrange an interview.

Homelessness expert on eviction moratoriums

Marybeth Shinn, Cornelius Vanderbilt Chair, Department of Human and Organizational Development, is available for commentary on eviction moratoriums and how they work. An expert on the topic of homelessness and affordable housing, Shinn is also the author of a recently published book, "In the Midst of Plenty: Homelessness and What to Do About It." Shinn can speak to: How an eviction moratorium works and consequences for it ending, including accumulated rents being due The health hazard that evictions and potential homelessness or congregate housing cause, especially as we continue to endure COVID Her view that we know what causes homelessness (lack of affordable housing, rising inequality, etc.) and have the resources to end it, but lack the political will Suggested government assistance to end the crisis and how affordable housing is the first step to getting people back on their feet (everything else, such as employment, comes second)

Assessing Biden's "Green Infrastructure" Plan From a Climate Perspective

In a virtual climate summit attended by leaders from all over the globe, President Joseph Biden announced plans for the United States to cut carbon emissions by as much as 52% by the year 2030. This commitment was outlined in what the Biden administration is calling a "green infrastructure" bill, one that has echoes of the Obama-era Green New Deal. Samantha Chapman, PhD, a biology professor at Villanova University and co-director of the Center for Biodiversity and Ecosystem Stewardship, recently broke down the pros and cons of the bill with KYW Newsradio's Matt Leon. According to Dr. Chapman, the bill addresses what she identifies as the two major strategies for mitigating the negative effects of our warming planet: "preventing more climate change and adapting to climate change." Dr. Chapman considers that the strength of the bill lies in what she and Matt Leon refer to as "base hits" rather than the "home run" structure of the Green New Deal, meaning that Biden's plan relies on smaller, easily achievable goals—like incentivizing a switch to a more sustainable type of cement for building bridges—rather than sweeping reform in an effort to get the bill passed. Dr. Chapman calls the improvement of the power grid, which would support the manufacturing of electric cars and ease our nation's reliance on fossil fuels, "one of the biggest things in the bill." The professor also notes that she is hopeful about the installation of broadband in remote areas allowing for wider internet access and investment in energy-efficient affordable housing and job training to support communities that rely on the fossil fuel industries. "You can't just shut these people's livelihoods down and say 'okay, good luck' or just give them a payout. People want to have jobs that fulfill them," says Dr. Chapman. This direction, focusing on infrastructure with climate and equity at the center of the conversation, is in line with the Biden campaign's slogan to "build back better." Dr. Chapman points out that this bill creates an opportunity to focus on the word "better" by reevaluating the definition of infrastructure itself. "What is infrastructure?" she asks. "Is clean air infrastructure? Is clean water infrastructure? We know that natural infrastructures [feedback systems like our waterways and forests]—and we still have a lot of them in the U.S., thankfully—give us a buffer against climate change." As a climate scientist specializing in coastal ecosystems, Dr. Chapman told Leon she hopes to see an emphasis on these types of natural infrastructures. "I think that salt marshes and mangroves are really important in buffering our coast against big storms, so I want to see explicitly that we are going restore these places. It would be good for biodiversity; it would be good for people hanging out and kayaking; and it would help us protect against these big storms that are coming whether or not we cap our emissions. I think I would like to see more of these green barriers along our coast rather than big seawalls, and I haven't seen that exactly yet, but again the fine print's not there," she points out. "The bill's not done." Finally, Dr. Chapman spoke to how this infrastructure bill could have an impact on the future of the country if it is passed and observed. "I think there's still work to do on things like forests and biodiversity; there's always more work to do. I think it would be a massive step in the right direction. And then we'd have to go to the rest of the world and start doing some work there."