Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

April 1st is the one day we all expect to be fooled. Scammers are counting on the other 364

Breaking News: Free Cruise for All Retirees! Congratulations!!! If you are reading this, you have just been chosen for a luxury Caribbean cruise, a $5,000 shopping spree, and a lifetime supply of… well, something vaguely exciting. All you need to do is: Click this link, enter your banking info, confirm your SIN, and maybe your childhood pet's name for good measure. Still reading? Good. Because if that opening gave you even the tiniest thrill, the little flutter of wait, really? You've just experienced exactly what scammers are counting on. APRIL FOOL'S!!! And also: welcome to the world of phishing. Population: way too many of us. Phishing vs. Fishing: A Retirement Skill You Didn't Know You Needed There are two kinds of fishing in retirement. One involves a dock, a thermos of good coffee, and no deadlines at all. The fish might or might not cooperate. That's fine. That's the whole point. The other scenario involves someone trying to steal your identity by congratulating you on a cruise you never booked, a prize you never won, and a windfall that demands your banking details, your SIN, and, just for fun, the name of your first pet. (Buttons. It's always Buttons.) Let's make sure you're fluent in the first kind and bulletproof against the second. Fraud Doesn't Just Happen to Fools Here's something important to say aloud before we proceed. Fraud isn't caused by people being careless, gullible, or old. It is orchestrated by professionals whose full-time job is to manipulate human behaviour under pressure. There is a clear difference between these two, and how we discuss fraud influences whether victims come forward or stay silent out of shame. This issue is more significant than most realize. Canadians lost over $638 million to fraud in 2024, an increase from $578 million the previous year, according to the Canadian Anti-Fraud Centre. However, that figure only tells part of the story. The CAFC estimates that just 5 to 10 percent of total fraud losses are ever reported. Think about that for a moment. The number we see is already staggering, and the real total is almost certainly ten times higher. Seniors make up a disproportionate share of those losses, especially in investment fraud, romance scams, and the grandparent scam. But here's the part the statistics don't show: fraud is improving at its craft. These aren't the poorly written emails of 2005. Today's scams are refined, patient, and psychologically targeted. They're designed to create urgency, confusion, and fear — aiming to override careful thinking precisely when it's needed most. So let's talk about what that actually looks like. A Very Personal Fraud Story That Will Stay With You A family reached out to me recently, after reading one of my earlier posts on fraud and seniors. Their father had been the victim of a prolonged scam, one that unfolded over months and caused significant financial damage. They only found out after he passed away. Three things about this story stopped me cold. First, their father kept meticulous records. He journaled every interaction, every step, every decision. There was essentially a play-by-play account of how he became entangled and how difficult it became to find a way out. Second, he was an intensely private person. Not a single family member knew any of it was happening while it was happening. Third, he was a chartered professional accountant. Decades of financial training, discipline, and experience. Someone who understood numbers, risk, and how money moves better than most people ever will. And still. Under the right conditions, with the right psychological pressure applied at the right moments, he was drawn in. That is not a story about a foolish man. That is a story about how sophisticated fraud has become. And it is a story that is playing out in living rooms and email inboxes across this country every single day. Why Seniors Are Targeted (And It's Not What You Think) Scammers don't just go after older adults because they think we're naive. They go after us because we have assets. Savings. Home equity. Good credit. Pension income that actually shows up every month. We're not easy targets; we're valuable ones. They also go after us because retirement can come with conditions that fraud is specifically designed to exploit: financial anxiety about making savings last, changes in how we process decisions under pressure, and, for many, reduced opportunities to run something by a trusted person before acting. Social isolation is not a character flaw. It is a vulnerability, and the people running these operations know exactly how to use it. The Scams You Actually Need to Know About The Grandparent Scam. You get a call. It's your grandchild. They're in trouble, arrested, in an accident, stranded, and they need money right now. Please don't tell Mom and Dad. The caller may not even sound exactly right, but panic has a way of filling in the gaps. Sometimes a fake lawyer or police officer jumps on the line to add credibility. The script is designed to bypass your rational brain and go straight for your heart. If this ever happens: hang up. Call your grandchild directly on a number you already have. Every time. The CRA Impersonation Call. This one is especially popular at tax time. An official-sounding voice informs you that you owe back taxes and if you don't pay immediately via e-transfer or gift cards, a warrant will be issued for your arrest. The Canada Revenue Agency does not call you out of the blue demanding gift cards. Full stop. If you're ever unsure, hang up and call the CRA directly as 1-800-959-8281. The Romance Scam. Someone finds you online, charming, attentive, almost too good to be true. Weeks or months in, a crisis emerges. Could you help, just this once? These scams are emotionally brutal and financially devastating. If an online relationship moves unusually fast and a financial request follows, that's not love. That's a script. The Investment Opportunity. Guaranteed returns. Exclusive access. Limited time. These words belong together the way "healthy" and "deep-fried" don't. Legitimate investments don't come with countdown clocks. Phishing Emails and Texts. These mimic your bank, Canada Post, Service Canada, Amazon, and anything you'd recognize. They look almost right. The email address is a little off. The link goes somewhere slightly wrong. They want you to click, to enter information, to act now before something bad happens. The urgency is the tell. No Shame. Seriously. None. If this has happened to you, or someone you love, please hear this: falling for a scam does not mean you are getting old, losing it, or slipping cognitively. It means you are human and were placed under carefully engineered psychological pressure by someone who practices this for a living. That is it. The end. And if you need a reminder that this crosses every age and profession, consider the case of a retired district court judge who lost the equivalent of over $100,000 to a digital arrest scam. Fraudsters called claiming his phone number was linked to a trafficking investigation. Despite decades on the bench watching deception unfold in real time, fear and intimidation did what all that professional knowledge could not protect against. A judge. Still got hooked. That is what these scams do when they are built well. (Source: Devdiscourse) RCMP Sergeant Guy Paul Larocque of the Canadian Anti-Fraud Centre puts it plainly: "Fraudsters are professional salespeople who work a target until they close the deal and get their money." That framing matters. You would not blame yourself for being sold something by a skilled salesperson operating under false pretenses. This is no different. The embarrassment is real and completely understandable. However, it does not fairly reflect what occurred. The CAFC has pointed out that many individuals feel ashamed of being victims of fraud and hesitate to report it, but every report helps break up fraud schemes and protect others. Reporting to the Royal Canadian Mounted Police is not a sign of failure; it is a vital way to safeguard the next person. A Word to Family Members re: Fraud: Drop It Like It's Hot If someone you care about has been scammed, put down whatever you are holding, take a breath, and read this carefully. Do not scold them. Do not lecture them. Do not "grandsplain" them into the ground. Grandsplaining, for the uninitiated, is mansplaining for the aged, and it is just as unwelcome. Nobody needs a slow, patient, thoroughly detailed breakdown of everything they should have done differently while they sit there wishing the floor would open up and swallow them whole. They already know. They feel terrible. They have probably been replaying every moment of it since it happened, asking themselves how they missed it, why they trusted it, and what they were thinking. What they do not need is you asking those same questions out loud. Your role at this moment isn't to be the smartest person in the room. It's not to claim you would never have fallen for something like this. And it's certainly not to start a sentence with "well, I always said you should..." because if you finish that sentence, you're on your own. Your job is to be kind. Full stop. Help them contact the bank. Sit with them while they file the report. Make the tea. Handle the phone call they are too rattled to make. Be the calm in the room. That is what love looks like in a crisis, and this is a crisis. Now here is the part where the tables turn, so pay attention. Scammers are not ageist. They are not sitting in a room somewhere saying, "Let's only go after the over-65s today." They go after anyone with money, a phone, and a moment of distraction. Which means they go after everyone. Your inbox is not immune. Your judgment under pressure is not immune. Your "I would never fall for that" confidence is, frankly, exactly the kind of thing scammers count on. Fraud can happen to anyone, and sharing your experience with others, whether or not money was lost, can help prevent them from being victimized by the same or a similar fraud. Nobody is too sharp, too young, or too digitally savvy to be targeted. The call is coming for all of us eventually. So when it comes for you, and you call your mother in a panic, wouldn't you rather she answer with warmth instead of a very long "I told you so"? Be nice to her now. Consider it an investment. One day, she might be the one sitting you down for "the talk." And at that point, the only appropriate response is to make the tea and keep your opinions to yourself. What the Experts Say: Practical Tips to Stop Fraud In my book "Your Retirement Reset" (ECW Press: Now available for Pre-Order here), I cover the topic of fraud and scams." I wanted to address this issue in depth because fraud prevention is not a footnote in retirement planning. It belongs front and center. Here is an excerpt of Chapter 9 of the book: "Remember the old saying, 'Nothing ever comes free'? While it is hard for many seasoned Canadians not to trust a caller, unfortunately, that's the way of the world today. Here are some tips for protecting yourself. Be skeptical. Be wary of unsolicited phone calls, emails, or messages, especially those asking for personal information or money. Don't take their word for it. Ask the person for their details. If they say they are calling from your bank, get their name and branch number and call your bank for verification. If the message is in an email, contact the institution identified in the email. Do not respond right away, ever. Don't share personal information. Never share personal, financial, or health information with unknown individuals or organizations. Consult trusted individuals. Discuss suspicious offers or communications with family members, friends, or trusted advisors. This is especially important if you are asked to donate to a charity or make any kind of financial investment. Use technology wisely. Install antivirus software, create strong passwords, and stay alert to phishing tactics such as harmful links in texts or emails. Use the block feature on your phone to cut off repeat callers you suspect are fraud artists. Work closely with your financial institution. Ask your bank to send alerts for any unusual activity on your account. Review your statements every month and report unauthorized transactions immediately. Report suspicious activity. If you suspect a scam has targeted you, contact the police. Stay informed. Keep up to date on prevalent scams aimed at older adults. A quick Google search on any unsolicited information request can often tell you whether it has already been flagged. These scams are frequently reported to authorities and featured in the media and on consumer advocacy websites." How to Stay Off the Hook When It Comes to Fraud A little friction can be helpful. Scammers depend on speed, on you reacting before you think. The best thing you can do is slow down. Avoid clicking links in unexpected messages; instead, go directly to the company's website by typing it yourself. Call back on a number you find independently, not one provided in the suspicious message. Check email addresses carefully, as a transposed letter can sometimes be all it takes. Keep your devices updated, since those updates fix real vulnerabilities. Discuss these topics openly. With your kids, friends, book club, or the person behind you in the coffee line. Scams flourish in silence and shame. Talking honestly is one of our strongest protections. In retirement, urgency belongs in spin class. Not your inbox. What to Do If You Took the Bait No judgment here. These scams are truly sophisticated. Smart, experienced, financially educated people fall for them, as we've just established. If you think you've been scammed, stop engaging immediately, change your passwords, contact your bank to flag or freeze your account, run a security scan on your device, and report it to the Canadian Anti-Fraud Centre at 1-888-495-8501. Reporting matters even if you cannot recover the money. It protects the next person in line. Think of it as cutting the line before the fish swims off with your whole tackle box. 3 Things Worth Setting Up This Week to Protect Yourself from Fraud These take 20 minutes and quietly protect you around the clock. Two-factor authentication (2FA) adds a second verification step. It's usually a text code. And it helps ensure that a stolen password alone won't give access to your accounts. Credit Card controls allow you to lock and unlock your debit or credit card instantly through your bank's app, so if something seems suspicious, you can freeze it within seconds. Real-time alerts enable you to set notifications for any transaction over a threshold you specify, so if someone is spending your money, you are informed immediately, rather than finding out at the end of the month when the damage is already done. Don't Get Hooked by Fraud. Retirement should be about freedom. The freedom to fish from a proper dock, travel somewhere warm, and spend your money on things that truly bring you happiness. It's not meant to involve fake urgency, suspicious links, or people who want your SIN and the name of your childhood cat. We Need to Do More to Protect Seniors The fraud prevention system in this country, to be frank, hasn't kept pace with the rise of fraud itself. That gap is real, it's growing, and it needs more attention than it currently gets. Meanwhile, the best we can do is stay informed, keep in touch with trusted people, and not let embarrassment prevent us from seeking help or reporting what happened. You worked hard for what you have. You deserve to enjoy it without looking over your shoulder. So enjoy the lake. Take the cruise — a real one that you booked yourself. Spend wisely, live well, and protect what's yours. And if anyone ever tells you that you've won something you never entered? Smile. Wish them a Happy April Fool's. Then hang up. Have a scam story, a close call, or thoughts on what fraud prevention is getting right or getting wrong? I would love to hear from you. Drop it in the comments or send me a note. This is exactly the kind of conversation we should all be having, and the more real experiences we share, the better equipped we all are to protect each other. Sue Don't Retire…ReWire! My Book is Now Available for Pre-Order If this message speaks to you, or to someone you love, I hope you will pre-order a copy of Your Retirement Reset. Available September 8, 2026. Here's the link. And if you love supporting Canadian booksellers, please also check with your local independent bookstore. Most can easily order it for you.

What the Meta/YouTube Verdict Still Misses About Youth Social Media Harm

The verdict against Meta and YouTube has reignited debate over addictive design and youth social media harm. But according to Harshi Sritharan, clinician and digital dependency expert with Offline.now, one key issue is still being overlooked: digital emotional regulation. Sritharan works with young people and families dealing with the real-life fallout of harmful platform design, including compulsive scrolling, sleep disruption, body-image distress, emotional dysregulation, and conflict at home. “The goal isn’t to remove technology from their lives entirely,” says Sritharan. “It’s to help young people and their families build healthier relationships with it.” She can speak to why regulating platform design matters, why digital resilience and online emotional regulation should be treated as core life skills, and why simply restricting access without healthier alternatives can push vulnerable youth into harder-to-monitor spaces. As news coverage focuses on liability and platform accountability, Sritharan offers a frontline clinical perspective on what these harms actually look like inside homes - and what young people, parents, schools, and policymakers may still be missing. ABOUT THE EXPERT Harshi Sritharan is a clinician and digital dependency expert with Offline.now, a digital wellness platform connecting individuals and families with therapists, coaches, and social workers who specialize in healthier relationships with technology.

Covering Cuba? Augusta has one of the leading experts ready to help with your coverage

Cuba is facing one of its most severe crises in decades, as compounding economic and energy challenges continue to strain everyday life on the island. Persistent fuel shortages have led to rolling blackouts, transportation disruptions, and reduced industrial output, while inflation and shortages of basic goods have eroded purchasing power for ordinary Cubans. Tourism, once a critical source of foreign exchange, has struggled to fully recover, and the country continues to grapple with declining productivity and limited access to international capital. These pressures have contributed to rising public frustration, increased migration, and a government response that blends cautious economic reforms with efforts to maintain stability. Paolo Spadoni is an ideal expert for journalists covering this evolving situation. As a specialist in Cuba’s political economy, his work focuses on the island’s external sector, including foreign investment, remittances, tourism and the impact of international sanctions. He brings a rare ability to connect on-the-ground developments – such as energy shortages or policy changes, to the broader structural realities shaping Cuba’s economy. With deep academic research and ongoing analysis of current reforms, Spadoni offers clear, credible insight into whether Cuba’s latest measures signal meaningful transformation or simply short-term responses to a prolonged crisis. Paolo Spadoni, PhD, is a widely recognized expert on Cuba and its international relations. He is a tri-lingual political economist with a specialization in international relations and a focus on Latin America’s political and business environments. His research focuses on international relations theories, Cuba's economy and business market, foreign investment in Cuba and U.S.-Cuba relations. View his profile Since this crisis escalated, Spadoni has been the 'go-to' expert for reporters with media from across North America like Reuters, Bloomberg and The New York Times connecting with him for his expertise, input and perspective on the situation. LA TERCERA: “The Cuban tourism sector was already struggling before the Covid pandemic. The best year for international tourism in Cuba was 2017 in terms of foreign exchange earnings. That was the year in which $3.3 billion was collected, and tourism represented 10% of Cuba's GDP at that time. In terms of employment, it provided 120,000 direct jobs and roughly 500,000 indirect jobs. So it played a significant role. That was the best year for international tourism in Cuba, which coincidentally ended in November of that year with the sanctions imposed by the first Trump administration. From then on, tourism from North American visitors began to decline, but European and Canadian visitors were already decreasing,” Spadoni explained to La Tercera. CBC NEWS: "Most of those investments are real estate investments more than tourism investments, meaning the Cuban military has taken possession of prime locations in the best tourism areas of Cuba," said Paolo Spadoni, an associate professor at Augusta University in Augusta, Ga., and co-author of the 2025 book The Cuban Tourism Industry: Evolution, Challenges and Prospects. Columbia Law School: "While seeking to finalize an economic agreement with Cuba, the Trump administration could secure deals across various sectors of the economy. However, tourism holds the most promising opportunities in the short term." Global News (Canada):

Retirement Maxxing: How Small Decisions Help You Build a Better Future

The basic idea is to pick a corner of your life and optimize it ruthlessly. Sleep maxxing. Health maxxing. Productivity maxxing. In its more extreme corners, people are attempting to optimize their actual physical features. Go ahead and Google "looksmaxxing" if you are curious and have a strong constitution. One influencer named Clavicular — a 20-year-old from Hoboken who claims to have taken a literal hammer to his face to coax a chiselled jawline — has become the reigning king of this particular rabbit hole. Medical experts would prefer you not try that at home. The Globe and Mail published a comprehensive explainer on the whole phenomenon. The Republican National Committee put out a press release praising Donald Trump for "jobsmaxxing" the economy. The Department of Defence posted a soldier with the caption "lethality maxxing." It has become, as one writer put it, the suffix that just will not quit. Retirement Maxxing: because chin waxing, I mean maxxing, was already taken. And yet, buried beneath all the absurdity, the underlying impulse is not entirely ridiculous. Humans want to optimize things. We always have. The real question is whether we are optimizing the right things. Then, as these things sometimes happen, three articles landed in my inbox in the same week and refused to leave my mind. Maxxing. The psychology of future selves. A golfer named Max Greyserman, who sits just one-tenth of a stroke from the top of his sport. I am not a woman who ignores signs. The connection was obvious once I saw it: retirement might be the most important time to apply this kind of thinking. Not the obsessive version involving ice baths and fourteen supplements before breakfast. The practical version. Thoughtful maxxing that quietly stacks the odds in your favour over decades. Retirement isn't just one decision; it's hundreds made over the years, each guiding your future self toward either financial dignity or a Shaggy tribute tour you never signed up for. The “Shaggy Problem”: How Your Retirement Decisions Today Determine Your Financial Security Tomorrow You remember Shaggy. The reggae artist. Enormous hit. "It Wasn't Me." When it comes to retirement, it absolutely was you. Every decision you make today is writing a letter to your future self. Some of those letters are generous and thoughtful. Others arrive decades later, like a bill you forgot to pay, from a creditor with excellent memory and zero sympathy. The seventy-five-year-old version of you hopes the fifty-five-year-old paid attention. The eighty-five-year-old version would very much like functioning knees, a dignified income, and the ability to say "I planned for this" rather than "I did not think it would go this fast." It went that fast. That's why the most useful habit you can develop right now is what I call the future-self test. Before making a major financial or lifestyle decision, pause and ask: how will this look from the other end? Will I still think this tattoo is a good idea when I’m ninety? Will I regret staying in a house that is too large and too expensive for another decade? Will my future self thank me for delaying CPP, or curse me for taking it early because waiting felt uncomfortable? Or as the Beatles asked rather memorably: “when I'm sixty-four, will you still need me, will you still feed me?” The song is charming. The financial planning version is considerably less so if you have not thought it through. The future-self test is not complicated. It is just the habit of writing better letters. What Sports Analytics Can Teach Us About Smarter Retirement Decisions Speaking of decisions that come back to haunt you, let's discuss probabilities. A recent New York Times article about golfer Max Greyserman stopped me mid-scroll (Lindgren, 2026). Not because of the golf — though the golf is fascinating — but because of what it revealed about the gap between what the data says and what people actually do when the stakes are high. Greyserman's scoring average is less than one-tenth of a stroke per round away from the elite level. One-tenth of a stroke. Not a full swing, a putting mistake, or a collapse on the eighteenth. The difference between obscurity and greatness in pro golf is about the time it takes to find your reading glasses. Which, as we've established, were on your head the entire time. Hockey analytics have demonstrated that teams trailing late in a game should often pull the goalie much earlier than the traditional last-ninety-seconds rule. Research indicates that pulling the goalie around the eight-minute mark can significantly boost the chances of scoring, as the extra attacker alters the odds. However, most coaches still wait until the final minute or two. Why? Because if you pull the goalie at eight minutes and lose badly, it can look like you lost your mind. The math checks out, but the optics are terrifying. Soccer offers a similarly uncomfortable example. A widely cited study analysing thousands of penalty kicks found that about one-third of kicks are aimed straight down the middle of the net, yet goalkeepers stay in the centre only around six percent of the time (Chiappori, Levitt, & Groseclose, 2002). Shooting directly down the middle often provides good odds because the keeper has already committed to diving one way or the other. But if the goalkeeper stays put and makes the save, the kicker seems to have tried to outsmart the odds and failed. The math checks out. The optics, however, are still terrifying. Retirement is filled with these moments. And most people make their decisions based on the optics. Common Retirement Decisions Canadians Get Wrong — And What the Data Actually Says: Working a couple of extra years often delivers significantly better retirement outcomes, yet people retire early because they feel emotionally ready. Delaying CPP can greatly increase guaranteed lifetime income, yet many choose to claim early because waiting seems risky. Downsizing can free up cash and lessen financial stress, yet people stay in large homes because selling feels like giving up. Using home equity wisely can boost retirement income, yet many retirees dismiss this option because of a stigma rooted in outdated beliefs rather than current data. In each case, the emotionally comfortable choice is not the one with the best long-term odds. Fear of loss, fear of regret, fear of looking foolish — those emotions sprint ahead of rational thinking every single time. That is why the future-self test matters. Math is universal, but money is deeply personal, and the goal is to let one inform the other before it is too late. The Psychology of Retirement Saving: Why We Treat Our Future Self Like a Stranger The second New York Times article examined the psychology of how we connect with our future selves (The New York Times, 2026). The findings are humbling. Psychologists have discovered that people often see their future self almost like a stranger, which explains why saving for retirement can seem somewhat punishing. It feels less like helping yourself and more like sending a cheque to someone who shares your cheekbones but whose problems seem distant and abstract. Research led by Hal Hershfield found that when people feel more connected to their future selves, they save more and make consistently better long-term financial decisions (Hershfield, 2011). Retirement planning is not just about spreadsheets and withdrawal rates. It is about being genuinely generous towards the person you are becoming. It is a love letter, written in small decisions, over a very long time. So, write a good one. Your future self is counting on you. How to Optimize Your Retirement: A Practical Framework for Canadians If retirement maxxing were a lifestyle trend — and I am formally proposing that it should be — it wouldn’t involve bone-smashing or extreme jawline enhancement. It would look more like this. Health Maxxing: Why Strength and Mobility Are Financial Assets Move your body. Lift weights now and then. Walk up hills. Muscle strength is one of the most underrated assets for retirement that nobody discusses at dinner parties. Research from the National Institute on Aging confirms that strength training improves mobility, balance, and healthy longevity (National Institute on Aging, 2023). These are the very factors that influence whether your later years feel like a gift or a burden. People hesitate over the cost of a gym membership while ignoring the significant long-term benefit of staying upright, independent, and capable. Skipping exercise to save a few dollars is like stepping over a hundred-dollar bill to find a quarter. As Aunt Equity likes to say: be careful not to get out over your skis. (Yes, that was an exercise metaphor. You’re welcome.) Income Maxxing: How to Build Reliable Cash Flow That Lasts Build reliable income streams so you can sleep at night without one eye on the market. Pensions, annuities, dividends, home equity, and carefully structured withdrawals — these all play a role in a well-crafted retirement income plan. The goal isn’t to maximize a single number – it’s to reduce the worry behind all of them. If your retirement plan currently makes you watch financial news at midnight while eating crackers over the sink, something has gone wrong and we should talk. Purpose Maxxing:Why It Matters for Your Health and Longevity Retirement is not a forty-year holiday. Humans need purpose, connection, and something worth getting out of bed for — especially on days when nobody expects you anywhere and the morning is entirely, terrifyingly yours. NIH research consistently shows that social engagement and a sense of purpose are linked to better health and longer life (National Institute on Aging, 2023). Purpose is what makes a retirement that feels like freedom different from one that feels like a long Sunday afternoon with nowhere to go. Somewhere along the way, society decided that aging meant quietly fading into the background. Retirement is when you finally have permission to dye your hair a vibrant colour, volunteer somewhere meaningful, start a project that genuinely excites you, or do all three at once and totally surprise your grandchildren. Purpose is not optional. It is the foundation. Decision Maxxing: How to Overcome Emotional Bias Use data when the stakes are high. Emotions are useful for choosing dessert but much less reliable for planning a thirty-year income. Don't swat away analytics like a fly at a family picnic just because they suggest something uncomfortable. Run projections. Stress-test your plan. Understand probabilities. Pull the goalie early if the math indicates so, even if it looks odd at the moment. Because appearing odd now and being wrong later are not the same thing. Not even close. The Ending That Brings It All Together: Small Decisions That Compound Over Time Here’s what three articles about “maxxing” our future selves, and golf, taught me about retirement. Clavicular is out there taking a hammer to his face in pursuit of optimization. Max Greyserman is grinding for one-tenth of a stroke. Hal Hershfield is reminding us that we treat our future selves like strangers when we should treat them like people we love. And somewhere between all three of them is the retirement insight that really matters: the best decisions compound quietly. Tiny improvements in health, income strategy, purpose, and decision-making build up into dramatically different outcomes over decades. Not because of one dramatic move, but because of many small, sensible ones made with the future in mind. Your future self isn't a stranger waiting to judge you. They are the person you are intentionally becoming, shaped by every decision you make today. Perform the future-self test before making risky decisions like pulling the goalie, shooting down the middle, or getting a tattoo that might lead to an awkward chat with your colonoscopy technician (this is for you, JK). Consider whether your fifty-five-year-old self is being kind to your seventy-five-year-old self. Look at what the data says, not just what feels right. Retirement maxxing isn't about perfection. It's about making small, sensible decisions consistently and thoughtfully over time. Think of it as compound interest for your future self. Einstein allegedly called compounding the most powerful force in the universe. He was talking about money, but he might as well have been talking about the small, steady choices that create a retirement worth living. Your future self will be deeply grateful—having functional knees, a dignified income, and a tattoo they still absolutely love. And when you turn sixty-four, and someone asks how you got there so gracefully, you won't need to channel your inner Shaggy. You just smile and say: It was me! Sue Don’t Retire…ReWire! P.S. Aunt Equity approves. Ready to start retirement maxxing? Here are two things you can do today. Run the future-self test on one financial decision you have been avoiding. Just one. Write down what your seventy-five-year-old self would think of the choice you are leaning toward. You might be surprised what comes up. Move your body and find your people. Join a pickleball club, a walking group, a trivia night, or a bridge league. Laugh often. Sweat occasionally. Your future self needs both, and your colonoscopy technician will be thrilled. Want more insights like this? Subscribe to my free newsletter here, where I share practical strategies, real-world stories, and straight talk about navigating retirement with confidence—not confusion. Plus, all subscribers get exclusive early access to advance chapters from my upcoming book. For Canadians 55+: Get actionable advice on making your home equity work for you, understanding your options, and living retirement on your terms. For Mortgage Brokers and Financial Professionals: Learn how to become the trusted advisor your 55+ clients desperately need (and will refer to everyone they know). This isn't just another revenue stream—it's your opportunity to build lasting relationships in Canada's fastest-growing demographic.

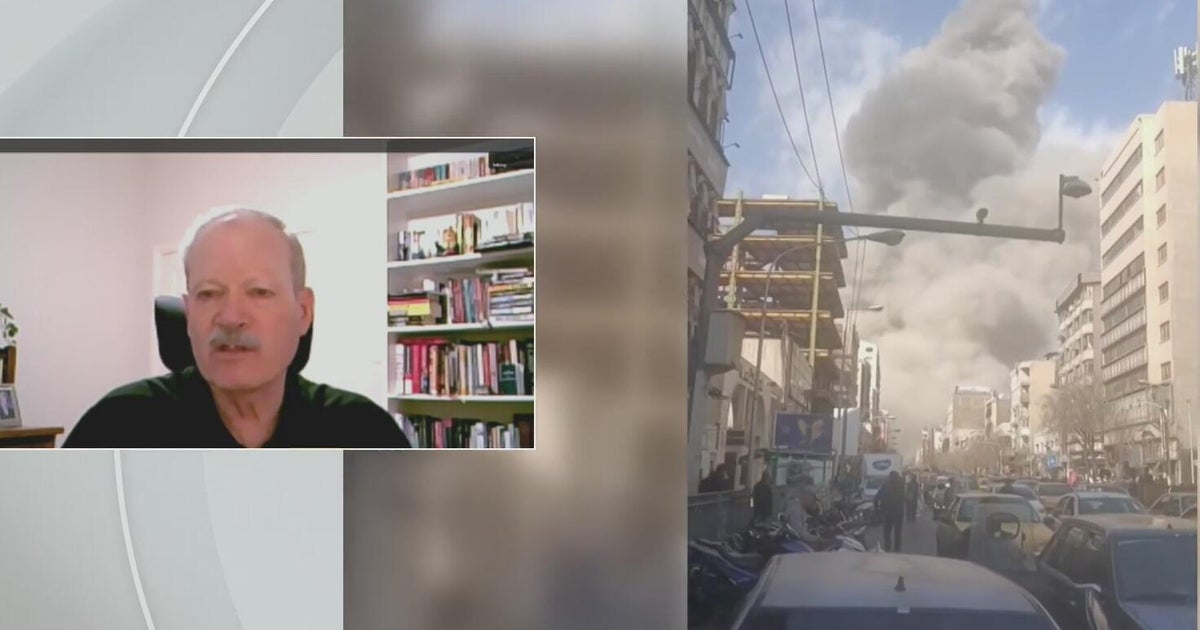

Covering the War in Iran? TCU has Experts that Are Getting National Coverage

As the war against Iran continues to unfold, global media coverage has intensified, with major news organizations providing near-constant reporting on the conflict and its geopolitical implications. From live battlefield updates to analysis of regional alliances, energy markets, and international diplomacy, the story has become one of the most closely followed developments in international affairs. Networks such as CBS News are dedicating significant airtime to helping audiences understand the rapidly evolving situation and the broader implications for global stability. To provide credible context and insight, these outlets often turn to academic experts who specialize in Middle East politics and international relations. Experts like Ralph Carter from Texas Christian University (TCU) are among those providing research-based analysis that helps explain the historical roots of the conflict, the motivations of the key actors involved, and what developments could come next. Their expertise allows journalists to translate complex geopolitical dynamics into clear, accurate information for audiences trying to make sense of a fast-moving global crisis. Professor Ralph Carter teaches introductory courses in political science and international politics as well as advanced courses in Middle East conflicts, U.S. foreign policy and Russian foreign policy. He is the author or editor of eight books and the author or co-author of over 50 journal articles, book chapters, and other professional publications. His research agenda focuses on the making of U.S. foreign, trade, and defense policy, with a particular emphasis on the roles played by members of Congress. Recently, Professor Carter's expertise was sought out by CBS News in Dallas/Fort Worth as journalists were updating Americans on the current situation in the war in Iran. Ralph Carter is available to speak with the media about the ongoing war in Iran - simply click on his icon now to arrange an interview today.

Manitobans are still eager to travel, but how and where they’re going is changing, and so are the risks they may not see coming. New survey findings released as part of CAA Manitoba’s Travel Wise Week show a clear shift toward staying closer to home. Sixty per cent of Manitobans prefer travelling within Canada, while just 20 per cent are planning a trip to the United States. Global uncertainty, rising costs, and changing perceptions about international destinations are influencing those decisions. “We’re seeing more Manitobans choosing Canada because it feels familiar and safe,” said Susan Postma, Regional Manager, CAA Manitoba. “But that sense of comfort can lead people to underestimate the financial risks that can still come with travelling, even within our own borders.” Staying in Canada and Leaving Coverage Behind While Canadians feel confident travelling within their own country, many assume “home turf” means low risk. This misconception leaves millions exposed to unexpected costs when trips don’t go as planned. The survey found that 64 per cent of Canadians did not have travel insurance for their most recent trip within Canada. Provincial health coverage often provides only limited protection when travelling outside your home province, and in some cases, does not cover services such as air ambulances, extended hospital stays, or trip interruption costs. Recent media stories have highlighted Canadians facing unexpected medical bills, emergency transportation costs, or sudden trip changes, all during trips that never left the country. “People are often surprised to learn how quickly expenses can add up if something goes wrong,” says Postma. “A simple injury on a hiking trail or a family emergency back home can turn a short trip into a major financial stress.” With recent geopolitical incidents in Cuba, Mexico and the Middle East, CAA’s Travel Wise Campaign is focused on helping Canadians understand risk, avoid misinformation, and make decisions grounded in facts rather than fear or speculation. Here are some tips: Understand what an “avoid non-essential travel” advisory really means: Travel advisories reflect real-time safety risks, and an “avoid non-essential travel” signal indicates rapidly changing conditions that may change quickly, and support may be limited. Know that advisories can affect your insurance and your exit options: Travelling against government advice can limit your travel insurance, including medical care or emergency evacuation. Coverage must be in place before conditions deteriorate. Flexibility is essential; review cancellation and change policies now: Travellers should proactively confirm cancellation deadlines, refund eligibility, rebooking options for all reservations and understand the limits of credit card protections, employee benefits, and pension coverage benefits. Stay connected to Canada while abroad: Canadians should monitor official updates from Global Affairs Canada and register with the Registration of Canadians Abroad service before departure or while on location if something arises. Rely on reputable sources and be cautious of misinformation online: Canadians should rely on official government sources, established travel organizations, and verified news outlets for travel guidance. Additionally, the CAA Air Passenger Help Guide helps you understand your rights when faced with common flight disruptions, such as delayed or cancelled flights or lost bags. The guide can be found at CAA.ca/AirPassengerHelpGuide. For more information on travel insurance and how to stay protected, visit www.caamanitoba.com/travelwise The online survey was conducted by DIG Insights from September 29 – October 8, 2025, with 2,0210 Canadian travellers aged 25 to 64 who have travelled outside their province of residence in the past three years and plan to travel again in the next five years, out of which 137 travellers were from Manitoba or Saskatchewan. Based on the sample size of n=2,021 and with a confidence level of 95%, the margin of error for this research is +/- 2%.)

Canadians remain passionate about exploring new destinations, but changing global dynamics are reshaping how and where they travel. According to CAA’s Travel Wise survey, more than half of Canadians (51 per cent) now say geopolitical and economic factors, such as instability abroad, a perception of the U.S. as being less welcoming, and rising travel costs, are influencing where Canadians choose to travel. Shifting Destinations and Attitudes Travel patterns are evolving. The survey conducted in 2025 shows that only 22 per cent of Canadians planned to visit the U.S., an 11 per cent drop from 2024. Instead, many are opting to stay within Canada (40 per cent) or explore international destinations. The perception of the U.S. as less welcoming, coupled with rising travel costs and global instability, is prompting Canadians to reconsider their travel plans. "Canadians are adventurous by nature, but today’s travellers are having to make thoughtful decisions," says Kaitlynn Furse, Director of Corporate Communications. "We’re seeing a clear trend toward exploring closer to home and seeking out new international experiences, all while keeping an eye on safety and value." Travel Insurance: A Critical, Yet Overlooked, Safeguard While Canadians feel confident travelling within their own country, many assume “home turf” means low risk. This misconception leaves millions exposed to unexpected costs when trips don’t go as planned. The survey found that 64 per cent did not have travel insurance on their most recent trip when travelling within Canada. “Recent stories have highlighted Canadians facing unexpected medical bills, trip interruptions, and emergency expenses while travelling within Canada, often because they didn’t realize their regular provincial health coverage or credit card benefits had limits,” says Furse. “If something were to happen, provincial healthcare only partially covers you outside of your home, and sometimes, not at all, covering only basic emergency medical services when travelling in another province.” Among those who travelled uninsured, 44 per cent believed coverage wasn’t needed, and 29 per cent thought their provincial government’s health plan would suffice. However, provincial healthcare only partially covers emergency medical services in other provinces, and sometimes not at all. “One of the biggest misconceptions we see is the idea that travelling within Canada comes with less risk,” says Furse. “Unexpected medical costs, trip interruptions and emergencies can happen anywhere, and many travellers are surprised to learn they’re not fully covered.” With recent geopolitical incidents in Cuba, Mexico and the Middle East, Travel Wise is focused on helping Canadians understand risk, avoid misinformation, and make decisions grounded in facts rather than fear or speculation. Here are some tips: Understand what an “avoid non-essential travel” advisory really means: Travel advisories reflect real-time safety risks, and an “avoid non-essential travel” signal indicates rapidly changing conditions that may change quickly, and support may be limited. Know that advisories can affect your insurance and your exit options: Travelling against government advice can limit your travel insurance, including medical care or emergency evacuation. Coverage must be in place before conditions deteriorate. Flexibility is essential; review cancellation and change policies now: Travellers should proactively confirm cancellation deadlines, refund eligibility, rebooking options for all reservations and understand the limits of credit card protections, employee benefits, and pension coverage benefits. Stay connected to Canada while abroad: Canadians should monitor official updates from Global Affairs Canada and register with the Registration of Canadians Abroad service before departure or while on location if something arises. Rely on reputable sources and be cautious of misinformation online: Canadians should rely on official government sources, established travel organizations, and verified news outlets for travel guidance. For many travellers, cancelled or delayed flights remain a top concern. CAA’s Air Passenger Help Guide offers a straightforward resource for travellers facing disruptions. The online survey was conducted by DIG Insights from September 29 – October 8, 2025, with 2,0210 Canadian travellers aged 25 to 64 who have travelled outside their province of residence in the past three years and plan to travel again in the next five years. Based on the sample size of n=2,021 and with a confidence level of 95%, the margin of error for this research is +/- 2%.)

Operation Epic Fury: Florida Atlantic's Expert is Ready for Your Questions and Coverage

As tensions surrounding Operation Epic Fury in the Middle East intensifies and the risk of regional escalation grows, Robert G. Rabil, Ph.D., professor of political science at Florida Atlantic University, stands out as one of the most authoritative voices journalists can turn to for clear, strategic analysis. A nationally recognized scholar of Middle Eastern politics, political Islam, terrorism and U.S. foreign policy, Rabil brings decades of research, regional expertise and media experience to breaking developments. He does not simply react to headline, he explains the historical forces, ideological movements and geopolitical calculations driving them. At a time when the conflict’s implications stretch far beyond Iran’s borders, affecting Israel, Gulf states, global energy markets and U.S. national security, Rabil provides critical context on both state and non-state actors shaping events on the ground. Robert Rabil, Ph.D., professor of political science at Florida Atlantic University, is a leading authority on Middle Eastern politics, security, and U.S.–Middle East relations. View his profile Recent media coverage: WINK: Dr. Robert Rabil, a political science professor at Florida Atlantic University, said the attack marks one of the most significant escalations in regional conflict in years. "I would say now the joint attack today is one of the very few, if not the only, as a matter of fact, attack on a country in the Middle East," said Rabil. "And today, as we have seen, I believe that the President has taken the final decision, and he said, Listen, it's about time, mainly, either to change the regime or produce a change within the regime.” ABC News: “What the president has done recently, what he did with Maduro, and the assassination of Soleimani — all of that changes the regime’s behavior,” Rabil said. Rabil said if Iran’s government were to collapse or dramatically change, cooperation with Western nations, including the United States, could resume, especially if Iranians pursue a democratic alternative. The Jerusalem Post Op-Ed - The writer is a professor of political science at Florida Atlantic University. He served as chief of emergency of the Red Cross in East Beirut during Lebanon’s civil war. CNN Robert G. Rabil, Special to CNN Rabil offers measured, informed analysis rooted in decades of scholarship and policy study and can help with key story angles such as: • Iran’s Regime Stability and Internal Pressures How domestic dissent, economic strain and political factions inside Iran influence wartime decision-making. • U.S.–Iran Strategic Calculus What options Washington realistically has, historical precedents shaping current policy, and risks of escalation or miscalculation. • Israel and Regional Security Dynamics How Israel, Saudi Arabia and Gulf states are responding — and whether a broader regional war is possible. • Proxy Warfare and Militant Networks The role of Hezbollah, Hamas and other non-state actors in expanding or containing the conflict. • Iran’s Nuclear Program How the conflict affects nuclear negotiations, deterrence strategy and global security concerns. • Energy Markets and Global Economic Fallout Implications for oil prices, shipping lanes and international economic stability. • Long-Term Regional Realignment Whether this conflict accelerates a reshaping of alliances in the Middle East.

Target Market: Who Are They, What Do They Value, and Where Are They?

In last week’s column on Super Bowl ads, I stressed the importance of providing a value proposition when you are advertising or marketing your goods and services. As a reminder, a value proposition is a promise that you make to potential customers that provides them a compelling reason why they should buy your product rather than a product from one of your competitors. Prior to developing a value proposition, you first need to understand who you are trying to sell to and what product characteristics they value. This will ensure that your value proposition will be more likely convince these buyers (your target market) to buy from you. The most effective Super Bowl ads from last week did this important work well. Once the company has a good, valuable proposition, it then needs to communicate that valuable proposition to its target market. Fortunately for companies with Super Bowl ads, just about all target markets are watching the game. However, for pretty much all other advertising and marketing, it must communicate where the target market will see or hear it. In today’s column, I will walk you through how to determine who your target market is, what they value, and finally, where to distribute your marketing messages. You are probably asking yourself, why is a guy who teaches Operations and Supply Chain Management (O&SCM) writing about Marketing? The answer is simple, really. It is the job of the O&SCM function of the company to deliver on the value proposition. So, as marketing develops its value proposition, it must confer with O&SCM to determine if the firm can deliver on that value proposition. If marketing communicates a value proposition it cannot meet, the company will likely be unsuccessful. With that in mind, let us examine the target market/value proposition development process. As a firm begins to identify its target market for a particular product, it must first determine the various potential customers who might buy that product and attempt to partition those customers into groups who value similar things. For instance, looking at the automobile market, there are some customers who value low price most, some who value performance and aesthetics most, and others who value reliability, durability, and consistency. If we are either in the automobile market or thinking about entering the automobile market, we need to find a group that values some characteristics that we think we can provide better than other market entrants. As you can see, the identification of a target market and the development of a value proposition that will appeal to that target market are done concurrently and iteratively. As noted above, the O&SCM function of the company is also brought in during these iterations to determine if the physical good can be manufactured or a service can be delivered in such a way that it can meet the value proposition. One important thing to remember is that in most cases, you are not your target market. What I mean by that is that you are often biased by your own knowledge and taste/preferences, and this may differ significantly from what your target market values. Remember that you are a unique individual whose preferences for a price point and evaluation of other characteristics might differ from your target market. Be sure to develop a value proposition that reflects the buying habits of your target market customers. Once you have developed a strong value proposition that you know your O&SCM can deliver upon, it is time to message that value proposition in places where your target market is present. As noted above, this aspect of our process is like “shooting fish in a barrel” for Super Bowl advertisers because all target markets are typically watching the Super Bowl. It is not so trivial for the rest of us. We need to understand what forms of media our target markets consume (e.g., television, radio, social media), but also, with each of these media, which applications or types of shows do they frequent. While most think social media skews young, and that is true for the most part, Facebook skews older, while Instagram, Snapchat, and TikTok skew much younger. On television, much of network television skew older, but there are shows like “Dancing with the Stars” and The “Bachelor” that do particularly well with younger women. Many mornings when I am getting ready for the day, I listen to “Augusta’s Morning News” on WGAC radio, and it is clear that my fellow listeners are primarily in my age demographic. My advice is to do your homework and find out where your target market is consuming media. All the work above is not very easy, but doing it right will lead to big returns. If you can identify who you want to target, based on what they value, and then be sure they get the marketing message that you have what they value, your business will succeed!

Pennsylvania Officials Highlight Snow Squall Safety

Research by Dr. Jase Bernhardt, Hofstra University associate professor of geology, environment, and sustainability, was recently highlighted during a press conference held by several state agencies in Pennsylvania on snow squall safety. The Pennsylvania Department of Transportation (PennDOT), Pennsylvania Turnpike Commission (PA Turnpike), Pennsylvania Emergency Management Agency (PEMA), Pennsylvania State Police (PSP), and the National Weather Service (NWS) highlighted investments by Governor Josh Shapiro’s administration that have led to an average of 7% fewer winter crashes and a 34% decrease in serious injuries and fatalities in those crashes. Media outlets that covered the press conference included the Times News Online.