Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

Carney Cares. The Tax Code Doesn’t.

Retirement analyst and author Sue Pimento looks more closely at the just-announced "Canada Groceries & Essentials Benefit Program" in the broader context of the country's overall tax-and-benefit system. A closer analysis of steep GIS clawbacks layered on top of taxes shows that some seniors face tax rates comparable to those of the country's highest earners. Pimento argues that we should address this “participation tax” to ensure seniors earn more without being penalized for their work. Prime Minister Mark Carney just announced the Canada Groceries and Essentials Benefit. The intent is good. The relief is welcome. The tax code, however, did not get the memo. Important Disclaimer (Please Read) This article is for educational and discussion purposes only and does not constitute financial or tax advice. Canada's tax and benefit system is complex, highly individualized, and subject to frequent changes. Before making any financial or tax decisions, consult a qualified professional familiar with seniors' benefits, including GIS, OAS, CPP, and related clawbacks. Now that we've cleared that up, let's talk… Here’s a quick overview of what was announced. What the Canada Groceries & Essentials Benefit Program Covers Bigger Benefit Cheques: About 12 million Canadians will receive relief. Food Bank Relief: $20 million to food banks through the Local Food Infrastructure Fund. Food Supply: Immediate expensing for greenhouse buildings to bolster domestic production. Food Security: A national strategy including unit price labelling and enforcement by the Competition Bureau. Business Support: $500 million in supply chain support to help businesses absorb costs rather than passing them on to consumers. These ideas aren’t bad. Some are very sensible. Taken together, the Government estimates in its announcement that these measures would "provide up to an additional $402 to a single individual without children, $527 to a couple, and $805 to a couple with two children. They go on to say that at these levels, Canada’s new government will be offsetting grocery cost increases beyond overall inflation since the pandemic." On paper, this looks helpful. Unfortunately, paper has never had to buy groceries. But… You knew there was a “but” coming. Government announcements are legally required to include one. A Little-Known Tax Reality That Makes You Shake Your Head New research shows Canada's tax-and-benefit system disadvantages low-income seniors who work. The issue? It's hidden in the tax code. On January 28, 2026, a Zoomer Radio Fight Back discussion hosted by Libby Znaimer highlighted the issue. Guests included: • Gabriel Giguère, Senior Policy Analyst, Montreal Economic Institute • Jamie Golombek, Managing Director, Tax & Estate Planning, CIBC Financial Planning & Advice Their conclusion? Canada's tax system discourages low-income seniors from working exactly when they need income the most. Many seniors discover (usually the hard way) that a small side hustle doesn't always pay off. It can lead to higher taxes and benefit clawbacks. Work a little more, and Ottawa takes a lot more. Why Seniors Are Still Working Because the math doesn't add up. Either way. More than 600,000 older adults live below the poverty line. Meanwhile, rent, food, utilities, insurance, and property taxes are increasing faster than pensions ever did. More seniors are employed, particularly GIS recipients. MEI analysis indicates that GIS recipients with work income increased by 56% from 2014 to 2022, rising to 64% among those aged 65–69. These seniors aren't working for "fun money." They're working to keep the lights on and purchase medication. Reviewing the details reminded me of a long-standing issue in my research on income and cash flow for Canadians aged 55 and over. Many Canadians can’t make ends meet and are forced to work well past 65. Yet Canada’s tax system punishes low-income seniors for working—exactly when they need income most. To understand why, we need to look at the Guaranteed Income Supplement. The Guaranteed Income Supplement (GIS) Program for Low-Income Seniors Here's how the GIS benefits work: • A non-taxable monthly benefit on top of Old Age Security for low-income seniors. • Roughly one-third of OAS recipients also receive GIS—over 2 million Canadians. • For a single senior with no other income, the maximum annual benefit is about $13,000. (Source: Government of Canada GIS website) The program has done meaningful work. Combined with OAS, CPP, and private pensions, Canada dramatically reduced senior poverty over the past half-century. But there’s a catch hiding in the design. Think of GIS as a hug that tightens when you try to stand up. The GIS Clawback Problem for Canadians GIS recipients can earn only $5,000 per year in employment income before clawbacks begin. After that, GIS takes back 50 cents of every dollar earned—before income tax and payroll deductions. A partial exemption applies to the next $10,000, where 25–37.5% is clawed back. The program helps seniors—right up until they try to help themselves. How the GIS Clawback Works Against Working Seniors Let me illustrate this. Meet Agnes. She is about to learn more about marginal tax rates than any bookstore employee should. Agnes is between 65 and 69 years old, lives alone, and receives OAS and CPP. Rising costs push her to take a job at a local used bookstore. She works about 15 hours a week at roughly minimum wage. Here annual gross employment income is about $13,000 Here’s what happens: • Her employment income triggers GIS clawbacks once she exceeds $5,000. • She pays income tax, CPP contributions, and sometimes EI premiums. • Between taxes and clawbacks, much of her earnings disappear. Simple version: Agnes works more hours but keeps far less than expected. When you keep 20 cents on the dollar, even capitalism looks confused. Agnes didn’t go back to work for the thrill of alphabetizing mystery novels. She did it to afford her prescriptions. A Canadian Tax System That Punishes the Wrong Thing If we’re going to test income, test investment income. Fine. Tax it. But employment income? Showing up? Working? The system treats that like misconduct. Once you add income tax, CPP contributions, and the loss of other credits, low-income seniors can face effective marginal tax rates of 70–80% on modest earnings. Nothing says “fairness” like taxing a bookstore clerk harder than a boardroom executive. As Gabriel Giguère of the Montreal Economic Institute has noted, "this level of taxation normally applies to wealthy Canadians—not seniors living in poverty." In a well-researched economic brief, Giguère and Jason Dean, Assistant Professor of Economics at King’s University College at Western Ontario, present a compelling argument for policy change. This comment by Giguère and Dean nicely sums up their key findings: "For various reasons, including insufficient pensions to maintain their living standards, seniors are increasingly turning to work. Yet the current tax-and-benefit system merits reform as it undermines their efforts, with the harshest effect on low-income seniors." One-Time Credits Don’t Fix Structural Problems At Davos, Mark Carney famously said, “Nostalgia is not a strategy.” Fair point. So why does our benefit system still behave as if retirement lasts ten years and ends with a gold watch? The system still thinks retirement lasts ten years and includes a gold watch. People are living longer. Many will spend 25 to 30 years in retirement. Some want to work. Many need to. A grocery credit helps. But a broken incentive structure still breaks people. Common Sense Tax Solutions the Canadian Government Should Consider 1. Raise the GIS earnings exemption The Montreal Economic Institute recommends raising it to around $30,000. Estimated cost: $544 million annually. Modest relative to the program’s size. 2. Exempt employment income from GIS clawbacks (at least partially) Keep testing investment income. Stop penalizing work. 3. Rethink retirement assumptions Policy built around “retire at 65 and earn almost nothing” no longer matches reality. None of these ideas are radical. They’re just… current. What to Ask Your Accountant About Your Tax Rate Get professional advice. Not generic advice. Not from Google. Not from your unemployed nephew. Ask specifically about: • Pension income splitting • Strategic RRSP contributions • Consulting or corporate structures where appropriate • Creative but compliant barter arrangements • CPP and OAS deferral strategies • Documentation. Lots of documentation. When clawbacks are involved, paperwork is your lifeboat. A Short, Honest Take Grocery relief is appreciated. The intent is good. But until Canada fixes a tax system that punishes low-income seniors for working, affordability will remain fragile. This isn’t about blame. It’s about aligning incentives with reality. Right now, it feels like we’re helping seniors swim by handing them bigger life jackets—while quietly drilling holes in the boat. And yes… I need to lie down. I feel another blog coming on. Apparently, exercising this much common sense counts as cardio. Sue Don't Retire...Re-Wire! Want more of this? Subscribe for weekly doses of retirement reality—no golf-cart clichés, no sunset stock photos, just straight talk about staying Hip, Fit & Financially Free.

Budget 25 – initial reactions related to personal financial wellbeing

As the director of the Aston Centre for Personal Financial Wellbeing, and a professor of taxation, I obviously take particular interest in the annual budget day as it sets a tone for much of the personal finance changes that are likely to occur in the near future. The lead up to this year’s budget had unprecedented levels of speculation with much of the press and commentators trying to get attention with ever more it seemed wilder guessing of what the chancellor might do – largely unhelpfully and worrying people and the markets unnecessarily. Almost all of this proved wide of the mark as the budget didn’t increase any of the main taxes at all, and where it might nudge National Insurance contributions (NICs) up for some, this won’t be for a few years and only in a small area (pension payments for employees) that won’t actually affect most people. Small and cautious steps to reform The reason for all this speculation of key changes needed was that everyone suspected there was a big hole in the national finances. This was shown not to be the case. In fact, predictions provided in the budget documents are we’d in fact be in budget surplus by the end of this parliament period even before the changes announced take effect. This was a surprise to many and meant the chancellor could actually focus on at least some small and cautious steps towards reforming how our tax, benefit and government spending systems work. What she proposed therefore is currently predicted will raise circa £26bn and give the government ‘head-room’ to cope with economic changes later rather than needed to fill a feared financial black hole now – good news all round! This meant what we actually got was lots of smaller changes with fewer ‘rabbit out of a hat’ big tax surprises than we have had in recent years – a welcome steadying trend I hope will continue. She also promised some short-term spending that can be paid for with a combination of extra borrowing now and with increased taxes later – again a trend of recent budgets. If these tax changes actually happen in the end, then it will be down to what happens between now and when these were proposed to commence – by no means a guarantee these will ever happen. Later budgets, or other rule changes in the future, could easily retract or counter them (all chancellors like to announce planned tax changes aren’t going to happen for obvious political gain reasons!). Income tax changes The largest share of the extra £26bn raised will come from extending the income tax thresholds for a further period – now to 2031. These have been fixed (at £12,570 for example for the point at which income tax starts to need to be paid on personal incomes) since at least 2023, some well before this. This matters, as, when wages rise due to inflation, people are not better off in reality (you get more income but things cost more), but may end up paying more tax than before as the thresholds haven’t increased with inflation to the same degree (what we call ‘fiscal drag’). As such, holding these thresholds fixed for longer will raise extra money for the government (predicted to be over £12bn a year in 2030-31 for example) – largely unnoticed as to many it doesn’t feel like the tax rise it clearly is. The threshold fixing extension announced today will mean that as many as 700,000 more people will start to pay some income tax when they wouldn’t currently, and up to 1 million more people will start to pay higher rates of tax than currently – all without being actually better off in real terms. Some call this stealth tax, but it feels very real when it starts to affect you if your total taxable incomes fall near these threshold levels. There were in total more than 70 other tax measure changes in this budget – a huge number and lots to get your head around. However, most of these will not affect most people and are relatively small in nature – targeted at making the tax system a little fairer (i.e. those on higher incomes, with more savings, dividends, receiving additional income from property they own etc – paying more taxes as a proportion of the total amount raised in tax from all sources). This is clearly welcome news (at least for those not being asked to pay this extra) in the current climate. The biggest changes for financial wellbeing As a research centre focusing on individual and family financial wellbeing, what do we think are the specifics announcements made that are most likely to affect people – several headline announcements are worth highlighting: - 1. The removal of the two-child limit on benefit eligibility is obviously a key headline – long touted as a key reason larger families are much more likely to be in poverty than smaller families. This is a key change that many Labour MPs wanted to see happen and the chancellor has delivered on it. This is very welcome news – although it won’t start to affect these families until after April 2026 to give time to bring these measures into place – but then predicted to lift 450,000 children out of poverty. 2. As part of making the tax system more progressive, a brand-new tax was announced on very expensive houses in England – to be snappily called the High Value Council Tax Surcharge (or HVCTS) – although expect it to be called the ‘mansion tax’ by everyone! The UK’s main local tax (council tax) isn’t going to be reformed as such in this change – despite being the target of much speculation that it is just too regressive to leave unreformed any longer after we haven’t revalued houses in most of the UK since 1991. This will instead be an additional tax, commencing in April 28, on those whose properties are valued (now) at £2m or more – with higher rates rising to those with properties over £5m. Clearly this will affect relatively few in most of the UK (only expected to affect 1% of properties nationally), but will affect some and will raise extra revenues (expected to raise circa £400m+ a year) to directly support provision of local services – much needed in many parts of the UK. 3. New taxes on electric cars – given fuel duty is not paid by those who drive electric cars (as they don’t buy petrol or diesel) there have been calls for new taxes to be charged to electric car drivers. While these cars may be better for the environment when driven, they continue to wear roads and contribute to congestion. The government is proposing a per mile charge from April 28 (to be called the Electric Vehicle Excise Duty or eVHD) for these vehicles which will be painful for electric car divers – not least as this cost as not known when purchase decisions were made. No-one likes a tax charged on something you have already made the decision to buy so expect this to be unpopular. It is proposed currently to cost EV drivers around £20/month – about half the rate of fuel duty on average – and expected to raise circa £2bn a year by 2030-31. I expect this tax will become more nuanced in future perhaps as technology enables perhaps different charges to be applied to use of congested city roads compared to open rural driving perhaps - we will see. 4. National Insurance deductibility for pension contributions via salary sacrifice schemes operated by many employers for their employees is to be capped at £2,000 (although only from April 29 – so no immediate effect). This now very widely used approach to making pension contributions if you are an employee that in effect avoids you having to pay NIC on this income going into your pension. For those with larger pension contributions the bit that can be made before NIC is due on the extra this will be capped in the future to £2,000 per year – again affecting those who receive higher pension contributions most and affecting those at the bottom of the income spectrum, little if at all (74% of employees are predicted not to be affected). Is this a breach of the Labour manifesto promises not to increase the main taxes? For some it certainly seems that way. What didn’t happen? There are many smaller measures to explore, or ones that are not coming into effect for the next year or more that might have been missed from the news headlines but that will almost certainly affect lots of people. To name just a few (including highlighting several things NOT going to happen – which will obvious not save people money per se, but help by not costing them more): - above inflation increases to national minimum (‘living’) wage for all age groups from April 2026 (+4.1% for those over 21)– although still not raising this to ‘real living wage’ levels. further extension of holding off on the 5p/litre fuel duty rise not increasing prescription charges (staying at £9.90 for the next year) confirming state pension rises by 4.8% from next April (worth £575/year) confirming £150 winter fuel payments again this winter to over 6 million homes freezing regulated rail fares – preventing the usual annual increases from January (the first time this has happened in 30 years) extending the government’s Help to Save scheme to more benefit recipients than previously No immediate impact for most Overall, this is therefore probably a welcome budget for many, those on lower incomes will likely get the most from these measures, if all are applied as proposed, but most won’t see much of an immediate impact immediately – and with the largest benefit likely to all on larger families in receipt of benefits from next April.

Canada's First Lifetime Fixed-Rate Reverse Mortgage: A Game-Changer or Just Another Option?

Every so often, a retirement product emerges that makes even a seasoned boomer take notice and remark, "Well, isn't that interesting?" The Globe and Mail reported that Bloom Finance has introduced Canada's first "lifetime fixed-rate reverse mortgage." What’s a Lifetime Fixed-Rate Reverse Mortgage? A Fixed Rate Reverse Mortgage is a financing option that gives you a permanently locked-in interest rate for as long as you hold the loan—not just for a typical five-year term. This could appeal to many Canadians entering retirement: It means you can unlock tax-free equity from your home without worrying that future rate hikes will eat into your cash flow or erode your long-term plans. What makes this even more appealing is the nature of a reverse mortgage itself. You’re not required to make monthly payments You retain full ownership of your home Your rate simply determines how your balance grows over time. When that rate is fixed for life, it removes one of the biggest sources of uncertainty, allowing retirees to plan confidently, protect more of their equity, and use their home as a stable financial tool rather than a source of stress. In short, a fixed-rate reverse mortgage combines the predictability retirees crave with the flexibility they need—something increasingly hard to find in today’s jittery rate environment. Bloom's New Lifetime Reverse Mortgage: Why People Are Talking Reverse mortgages allow homeowners aged 55+ to access up to roughly 55% of their home's equity without taxes, without monthly payments, and without affecting OAS or GIS. In the past, concerns have centred on the compounded interest and the uncertainty of future rates. Bloom's new Lifetime Reverse Mortgage offering aims to ease this stress by offering a fixed rate for life. Currently, that rate is 6.69%. The rates are a bit higher than other reverse mortgage products on the market. For comparison here are some current rates at the time of publication: Home Trust's (6.44% for a 5-year fixed rate) Equitable Bank (6.54%) HomeEquity Bank's (6.64%) 5-year fixed rates. Looking Beyond the Rates of Reverse Mortgages Bloom's real appeal with this new product is emotional: no more renewal surprises. For retirees on fixed incomes, the stability of a fixed rate feels different. It's like a weighted blanket for your financial nervous system. Think of it as an insurance policy against rising interest rates. And boomers love insurance. We insure our hips, luggage, vacations, eyeglasses, cell phones, and emotions (usually at the spa). So, a mortgage rate that stays stable? Yes, please. But let’s look beyond the mechanics of this product. We need to discuss a force even greater than compound interest: luck. Let's Talk About Luck (aka: The Retirement Wild Card) Here's a truth many boomers seldom admit: financial success isn't only about planning. It's about timing. It's about circumstance. And yes… pure, unfiltered luck. As humans — especially we entitled boomers — we tend to overemphasize our achievements and downplay our faults. And let's be honest: we don't like admitting when we're wrong. Society often rewards the strong and wrong more than the weak and right. (If you're unsure, just watch any political panel for 30 seconds.) Even Warren Buffett — the patron saint of rational investing — made a spectacularly poor decision when he bought Dexter Shoe for $433 million in Berkshire stock. The company later became worthless. Buffett described it as the worst deal of his life. If the Oracle of Omaha can make a mistake, the rest of us can certainly recognize how luck has influenced our real estate stories. And oh, did luck influence the boomer journey. We bought homes when they were affordable; when interest rates were character-building, and avocado appliances were peak chic. Then real estate skyrocketed. Homes doubled, tripled, quadrupled. Not because we were geniuses — but because we were standing in the right place at the right time. Let's be even more honest: A boomer's worst day in real estate is a millennial's dream day. We might not like admitting it, but it's true. And yes — boomers get to show off a little because we also carried the burden of our failures: recessions, layoffs, 19% mortgage rates, renovation disasters, and property taxes that still make us weep into our soup. But luck? She was definitely in the room. Now that we've named her, we can begin speaking honestly about how to use the equity we possess — wisely, deliberately, and with eyes wide open. Let's Discuss the Numbers (Because We Ought To) Here's where the real impact happens. Say you're 70 and you take out a $200,000 reverse mortgage at Bloom's lifetime rate of 6.69%. Over 20 years, with compounding interest and no payments, you'd owe approximately $724,000. Now, if you took out a traditional reverse mortgage at 6.54% over those same 20 years (not including rate hikes, though they're likely), you'd owe approximately $707,000. That's a $17,000 difference — not a high price to pay for lifelong comfort. But There Are Trade-Offs The early-exit penalties are steep: · 8% in year one · Decreasing until year five · Then three months' interest thereafter Penalties are waived if you downsize, move to assisted living, or pass away. But if you leave for other reasons? You're responsible for the costs. Translation: Only select this reverse mortgage product if you genuinely plan to stay put. Zooming Out: The Full Menu of Equity Options This lifetime reverse mortgage is just one tool in a broad (and expanding) equity-release toolkit. Others include: ADUs (Accessory Dwelling Units): Build a suite, rent it out, house a caregiver, or create multigenerational living. Offers independence and income potential. Downsizing: The classic move. Big house to small house to building a solid cash cushion. Emotionally complex, financially empowering. HELOCs (Home Equity Lines of Credit): Offer flexible, interest-only repayment options. Manulife One: The Swiss Army knife of HELOCs. Perfect for disciplined retirees. HESA (Home Equity Sharing Agreements): No payments or interest — you exchange future house appreciation for cash today. Traditional Reverse Mortgages: Similar to Bloom in structure but without the lifetime rate. And yes — boomers have more equity-access options than any generation in Canadian history. Not arrogance. Just facts. And increasingly relevant ones. Research shows that 91% of older adults in Canada prefer to age at home rather than move to an institution, with 92.1% of Canadian seniors currently living in private dwellings in the community. Honest Questions to Ask Yourself Before Signing for Any Type of Loan Wondering if you should take the leap? Before you even consider signing anything, pour yourself something warm (or stronger) and ask a few honest questions. · Am I emotionally ready, or just tired of worrying about money? · Am I genuinely content to remain in this home forever, or am I romanticizing the past? · Where are interest rates heading — and how will that affect my comfort level? · What exactly do I need cash flow for — income, essentials, opportunities, legacy, or "finally something for ME"? · Have I thought about how this decision might affect my children and inheritance? · What future choices could this create — or prevent? · And the biggest question of all: if Plan A fails, is Plan B truly realistic… or just wearing yoga pants and pretending? Because here's the real truth: the happiest retirees aren't the ones who got lucky — they're the ones who used their luck with purpose, timing, and emotional clarity. Bloom's lifetime reverse mortgage isn't a miracle cure, nor is it a trap. It's simply one tool — and for the right person, it provides emotional stability and financial predictability. Here's What Matters Before you sign for a reverse mortgage, HELOCs, or anything else with an acronym and a sales commission attached, here's my professional advice: Get the full picture so you can make decisions that truly work for your life — not merely to meet someone else's sales quota. The "best" financial move isn't the one that appears impressive on a spreadsheet. It's the one that allows you to sleep peacefully at night. The one that grounds you emotionally and supports you financially. Retirement isn't the end of the story. It's the chapter where you finally get to blend strategy with self-awareness, confidence with clarity, and luck with a bit of laughter. And if life insists on being unpredictable? Then outsmart it, outlaugh it, and choose the equity tools that help your future self say, "Nice move." Love, Aunt Equity" aka Sue "Don't Retire… ReWire!!!" Want to become an expert on serving the senior demographic? Just message me to be notified about the next opportunity to become a "Certified Equity Advocate" — mastering solution-based advising that transforms how you work with Canada's fastest-growing client segment.

Federal Budget 2025: What's In It for Canadian Seniors?

Let's be honest: the word "budget" probably makes you want to take a nap. Or pour a stiff drink. Maybe both. We spent decades pinching pennies, brown-bagging lunches, and watching every dollar so we could finally retire and stop thinking about money every waking minute. Now here I am, telling you to read about a government budget. I know. I'm sorry. But stick with me—I promise to make this as painless (and possibly entertaining) as possible. Why You Should Care About the 2025 Federal Budget (Even If You Really Don't Want To) Some of you hate talking about money. I get it. But here's the thing: information is power, and denial isn't just a river in Africa (give it a second to land)—it creates unnecessary ignorance and real missed opportunities to regain some control over your financial life. Plus, this budget affects your kids and grandkids too. So even if you're sitting pretty, the people you love might not be. The Economy Right Now: A Very Quick Explainer You've probably noticed everything costs more. A lot more. Welcome to inflation, courtesy of today's tariff-happy trade wars. (And if you want a deeper dive into how inflation affects more than just your wallet, check out my earlier piece: "Inflation: It's not just for prices anymore".) Here's the short version: When governments slap tariffs on imported goods (think: "You want to sell your stuff here? Pay up!"), Companies pass those costs directly to you at checkout. Your grocery bill goes up. Your heating costs rise. Even that new garden hose costs more because, apparently, everything comes from somewhere else now. So when you're living on a fixed income—CPP, OAS, maybe some RRIF withdrawals—and prices keep climbing while your income stays flat, that's a problem. A big one. Enter: the federal budget. It's basically Ottawa's financial to-do list: where they'll spend money, what they'll cut, and (theoretically) how they plan to make your life easier. Or at least less expensive. What's Actually In This Federal Budget Thing (The Good Parts Only) I've waded through the charts, jargon, and multi-billion-dollar announcements so you don't have to. Here's what matters to you: 1. Your House: Now it's a Potential ATM Remember when turning your basement into a rental suite sounded expensive and complicated? Ottawa heard you. The Secondary Suite Loan Program is expanded: Borrow up to $80,000 at 2% interest (15-year term) to build a basement apartment, garden suite, or in-law unit. The refinancing rules are also relaxed: You can now refinance up to 90% of your home's post-renovation value to fund these projects. Translation: You can turn unused space into monthly rental income, house a caregiver, or create a spot for family—all while boosting your property value. It's like your house went to entrepreneurship school. For more on Additional Dwelling Units (ADUs), check out this post. 2. Slightly Less Painful Tax Season Ottawa is cutting the base federal tax rate for modest-income earners and cancelling the consumer carbon price on heating fuels. Translation: If you're still working part-time or living on CPP + OAS + RRIF withdrawals, expect slightly lower deductions and cheaper heating bills starting this winter. We're talking maybe $30–$50 more per month—not a windfall, but enough to buy groceries without wincing at the checkout. 3. Health Care: Maybe, Possibly, Getting Better The budget includes more money for provinces to spend on health care and long-term care reform. The goal? Shorter wait times and expanded home-care programs. Translation: The government says they're helping seniors age at home with dignity. Whether that actually happens depends on your province not blowing the money on consultants and photo ops. Keep your eyes on provincial announcements for new or expanded home-care subsidies. 4. Your Savings: Slightly Less Likely to Evaporate Budget 2025 confirmed Canada has the lowest debt-to-GDP ratio in the G7. They're also cracking down on bank fraud and scams targeting seniors. Translation: Lower national debt helps keep interest rates and inflation under control, protecting the real value of your fixed income. And Ottawa is finally recognizing that scammers love targeting retirees. (If you haven't already, read my piece on The Rise in Grandparent Scams—it's eye-opening.) About time. Watch for my upcoming article on a recent senior scam making the rounds—and my assessment of how banks can do much more to protect seniors. 5. $60 Billion in "Savings" (Don't Panic) You'll hear politicians bragging about cutting $60 billion. Before you worry they're gutting CPP or OAS, relax. They're trimming their own bureaucracy—less middle management, more digital tools, fewer wasteful meetings about meetings. Translation: They're supposedly spending less on themselves so they can spend more on things that matter—like housing, health care, and infrastructure. Whether they actually pull this off remains to be seen, but at least they're talking about it. So What Does All This Actually Mean? Look, I won't pretend this budget is a game-changer. It's not. But it does offer a few smart moves if you're willing to act. And let's remember: this is Carney's first budget. Changing financial policy and spending priorities takes time—and some patience on our part. Rome wasn't built in a day, and neither is a functional federal budget that actually helps everyday Canadians. Review your home equity. Could an ADU loan help you age in place and generate income? Audit your expenses annually. Cutting $100/month in spending equals roughly $1,500 in pre-tax income. That's real money. Stay vigilant against scams. Government protection is nice, but it starts with you not clicking sketchy emails and text messages. Ask about tax credits. Low-income seniors may qualify for increased refundable credits under provincial top-ups this year. This isn't a flashy budget. There are no big checks in the mail. But it does signal a shift toward pragmatism: help Canadians stay housed, healthy, and financially secure while Ottawa tightens its own belt. For Canadians 55+, that means: Slightly lower everyday costs More options to create income from your home Continued investment in health and home care A more stable economy to protect your savings Progress? Maybe. One cautious, bureaucratic step at a time. Your Next Move Take 30 minutes this week to think through how these programs could fit into your life. Could an ADU loan make aging in place possible? Could refinancing free up cash flow? Small adjustments now = big peace of mind later. And that's what being hit, fit, and financially free is all about. And hey—you just read an entire article about a government budget. Voluntarily. That deserves recognition. Go ahead, brag about it. You've earned it. Now go enjoy your retirement. You've definitely earned that too. Sue Don’t Retire…Re-Wire!!!

Beyond the Repo Headlines: What the Liquidity Signals are Really Saying

In late October and early November 2025, usage of the Federal Reserve's Standing Repo Facility (SRF) reached elevated levels exceeding $50 billion at month-end -- the highest utilization since March 2020. Simultaneously, the Overnight Reverse Repo (ON RRP) facility has collapsed to approximately $24 billion, down from peak levels exceeding $2 trillion in 2023. This combination signals structural stress in U.S. money markets extending beyond seasonal factors. These two facilities serve opposite functions in the Fed's monetary policy framework. The SRF is an emergency lending facility where banks can borrow reserves overnight by pledging Treasury or agency securities as collateral, paying the SRF rate (currently 4.50%). It acts as a ceiling on overnight rates. The ON RRP works in reverse: money market funds and other institutions lend cash to the Fed overnight, earning the ON RRP rate (currently 4.30%). It provides a floor on rates. The depletion of ON RRP removes a critical shock absorber. When the facility held trillions in 2021-2023, it functioned as a deployable liquidity reservoir. During stress events, as repo rates in private markets rose above the ON RRP rate, money market funds would withdraw their cash from the Fed and deploy it into higher-yielding private repo markets. This automatic flow of liquidity would stabilize rates without Fed intervention. With ON RRP now depleted to $24 billion, this reservoir is empty. When liquidity shocks occur, there is no pool of cash to flow into stressed markets. Instead, all pressure falls directly on bank reserves, currently at approximately $2.8 trillion. The elevated SRF usage indicates that despite aggregate reserves appearing adequate, banks are unable to efficiently reallocate liquidity across the system. The core problem is that banks with surplus reserves face prohibitive costs to intermediating due to post-2008 regulations, particularly the Supplementary Leverage Ratio (SLR) and G-SIB capital surcharges. The SLR requires capital against all balance sheet assets, including reserves. For a large bank to lend $1 billion overnight, it expands its balance sheet by that amount, increasing SLR denominators and potentially triggering higher surcharge brackets. The capital costs of holding additional assets on the balance sheet often exceed repo market spreads, rendering arbitrage unviable. Banks with surplus reserves therefore park them at the Fed rather than lending to institutions that need them. Current conditions reveal that while dealer behavior around period-ends follows established patterns, the magnitude of rate effects has grown substantially. Recent Federal Reserve research documents that SOFR rose as much as 25 basis points above the ON RRP rate at recent quarter-ends, far exceeding the 5-10 basis point moves typical in 2017. The Fed's analysis attributes this to "growing tightness in the repo market and a diminishing elasticity of supply and demand" as reserves decline. Critically, the research shows that dealer quarter-end behavior -- reducing triparty borrowing and shifting to central clearing -- has remained "remarkably stable," yet rate impacts have intensified. This indicates the problem is not changing behavior but deteriorating underlying conditions. The pattern mirrors 2018-2019, when similar dynamics preceded the September 2019 crisis. Academic work from that episode documented that foreign banks reached minimum reserve levels while domestic G-SIBs maintained surpluses but declined to intermediate due to balance sheet constraints.¹ November 2025 differs critically from September 2019: the ON RRP buffer is now depleted. In 2021-2023, that buffer absorbed surpluses and prevented repo rate collapse. Its near-zero level means the system lacks this stabilizer precisely when QT has reduced reserves and Treasury issuance remains elevated. Additional liquidity pressure falls directly on reserves, leaving repo markets vulnerable to quarter-end dynamics, tax payments, or Treasury settlement volatility. Chairman Powell announced that QT will slow dramatically, with Treasury runoff ending while mortgage-backed securities continue maturing. However, this addresses only aggregate levels, not the structural issues driving period-end stress. The question remains whether current reserve levels are sufficient given elevated post-pandemic deposits, outstanding credit line commitments, tighter balance sheet constraints, and the expired Bank Term Funding Program. What do these signals indicate? Three interpretations emerge. The most likely is that quarterend and month-end rate effects will continue intensifying as reserves decline further, with the spread between SOFR and ON RRP at period-ends serving as a barometer of underlying tightness. Federal Reserve research suggests that as Treasury issuance continues and reserves decline, "the repo market is likely to tighten further and the effects of quarter- or month-ends on repo rates may grow, providing another potential indicator that reserves are becoming less abundant." This would manifest as larger SRF usage at period-ends and persistent elevated Fed facility usage, though system functioning would remain generally stable between these events. A more adverse interpretation sees a triggering event during an already-stressed period-end causing broader repo market seizure, forcing the Fed to resume asset purchases and confirming that meaningful balance sheet normalization is impossible under current structures. An optimistic interpretation requires regulatory reform -- SLR exemptions for reserves or changes to quarter-end reporting requirements -- to reduce incentives for balance sheet window dressing, though this appears politically unlikely. For banks, the implication is that reserve buffers need to be higher than pre-2019 benchmarks, and the ratio of demandable claims to liquid assets requires closer monitoring. For investors, continued volatility in short-term interest rates should be expected, particularly around periodends. The Fed's weekly H.4.1 release tracking SRF and ON RRP levels provides leading indicators. Money market fund flows have outsized impact as their allocation decisions directly affect system liquidity buffers. The transformation underway represents a fundamental shift from bank-intermediated to partially Fed-intermediated money markets. Post-2008 regulations strengthened individual bank resilience but broke private intermediation chains. The central bank now serves as both lender and borrower of last resort, with private markets unable to efficiently connect flows. September 2019, March 2020, March 2023, and November 2025 episodes demonstrate a pattern: reserves appear adequate until buffers thin, after which modest events trigger outsized disruptions. 1. Bostrom, E., Bowman, D., Rose, A., and Xia, A. (2025), "What Happens on Quarter-Ends in the Repo Market," FEDS Notes, Board of Governors of the Federal Reserve System; Copeland, A., Duffie, D., and Yang, Y. (2021), "Reserves Were Not So Ample After All," Federal Reserve Bank of New York. 2. Du, W. (2022), "Bank Balance Sheet Constraints at the Center of Liquidity Problems," Jackson Hole Economic Symposium.

Gig worker protection law boosted overall earnings but dropped hourly pay

A 2020 California law designed to protect gig workers by classifying them as regular employees, rather than contractors, ended up increasing their earnings by about 8%. However, their hourly pay dropped by 1.6% as companies offset the higher costs of benefits. Workers’ increased earnings came from working longer hours in order to qualify for and reap benefits like employer tax sharing. These findings come from a study led by Liangfei Qiu, Ph.D., a professor in the University of Florida’s Warrington College of Business, which examined nearly 400,000 monthly work records from about 41,000 freelancers on Upwork, one of the world’s largest online labor platforms. That trove of data let the researchers ask what actually happened when the law, known as AB5, took effect. Qiu’s is the first study to reveal how AB5 affected workers’ income and comes as other states consider passing similar laws. Liangfei Qiu is an expert in social technology, including social media and social networks, as well as artificial intelligence. View his profile here “It highlights some unintended consequences,” Qiu said. “If the labor market competition is similar to what we observe in California, then you might get lower hourly rates for gig economy workers and longer working hours.” “But it’s nuanced. In surveys, gig workers said they were willing to work longer hours because they had better benefits. The outcome depends on how involved someone is in the gig economy,” Qiu added. AB5 was designed to correct what labor advocates saw as widespread misclassification of a company’s essential employees as independent contractors, who don’t typically earn any benefits. This classification gives companies a cheaper workforce, and provides maximum flexibility for workers, but doesn’t allow workers to earn any sick leave, vacation or health insurance. Self-employed contractors must also pay the full share of Social Security and Medicare taxes, which works out to about 15% of gross income. Gig economy companies fought back against the AB5 regulations. A company-sponsored ballot referendum, Prop 22, exempted well-known giants like Uber, Lyft and DoorDash from the law later in 2020. And the California legislature provided further carve outs for professions like doctors, lawyers and photographers. The law still applies to contractors used by delivery companies like FedEx, UPS or Amazon, home-service companies like Angi or Rover as well as online freelance platforms like TaskRabbit. The study is forthcoming in the journal Information Systems Research. Qiu collaborated on the analysis with researchers at Baylor University, Santa Clara University and Stony Brook University. Looking to know more about the 'gig economy' and how it impacts the workforce? Connect with Liangfei Qiu today and click is icon now to arrange a time to talk.

20 Days Into the Government Shutdown: What’s the Impact on Your Wallet?

"Government shutdowns create a cascading financial impact that begins with federal workers but quickly spreads throughout the economy, with effects intensifying the longer the shutdown persists. Approximately 2 million federal civilian employees face direct financial disruption during shutdowns. Essential personnel in national security and public safety continue working without immediate pay, while non-essential workers are furloughed entirely. Although Congress typically authorizes back pay after shutdowns end, families must navigate weeks or months without regular income, forcing them to drain savings, incur debt, or miss critical payments like mortgages and utilities. Federal contractors face even greater uncertainty, as they often receive no compensation for shutdown periods, creating immediate cash flow crises for businesses of all sizes that depend on government work. The financial impact extends well beyond federal employees through several key transmission mechanisms. Reduced consumer spending from affected workers hits local businesses particularly hard, especially in areas with high concentrations of federal employment like Washington D.C. and military communities. Small businesses face additional challenges through delayed government contract payments and suspended access to Small Business Administration (SBA) loan processing. Critical financial services experience significant disruptions. Federal Housing Administration (FHA) and Veterans Affairs (VA) mortgage approvals slow or halt entirely, delaying home closings and affecting real estate markets. The Internal Revenue Service (IRS) may delay tax refunds and income verification services, further constraining household cash flow and complicating loan applications. Financial markets typically experience increased volatility during shutdown periods, as uncertainty about government stability affects investor confidence. Consumer confidence also tends to decline, particularly during prolonged shutdowns, leading to reduced spending that can amplify economic impacts. Credit rating agencies have historically warned that extended shutdowns could threaten the nation's credit rating, potentially raising borrowing costs across the economy. For most Americans whose income doesn't flow through federal channels, immediate wallet impact remains modest initially. However, the longer shutdowns persist, the more likely average citizens will experience effects through delayed services, financing complications, reduced economic confidence, and broader market softness. The cumulative impact grows exponentially with duration, making swift resolution critical for maintaining economic stability."

Why Brokers Are Canada’s New Mortgage Rockstars

There’s a quiet revolution happening in Canadian mortgage lending—well, as “quiet” as anything can be when two-thirds of Canadians are shouting, “We’d rather deal with a broker than a bank!” According to the most recent Mortgage Professionals Canada (MPC) Consumer Survey, 67% of Canadians now say they’d rather work with a mortgage broker than a bank. Among those who already have? A whopping 81% would do it again. That’s not just a statistic. That’s a standing ovation. The Great Mortgage Broker Boom According to recent MPC data, broker market share reached 33% in 2024—a four-point increase in just two years. Nearly half of all borrowers now choose brokers. The message is clear: Canadians are tired of sales reps; they want advocates who speak human, not policy manual. And who can blame them? With 1.2 million mortgages renewing in 2025 and average payments increasing by $513 a month, people aren’t just rate-shopping anymore—they’re seeking guidance, reassurance, and maybe a bit of hope. Let’s face it: they want their cake and still be able to heat their home too. Why This Matters—Especially for Seniors I work with Canadians aged 55+ every day, and about three-quarters of them are homeowners. They’ve done everything right: worked hard, paid off debt, raised families, and built wealth through their homes. But now, many feel… trapped by them. Here’s the reality: Mortgage renewals are costing hundreds more monthly (some facing 15–20% jumps) Inflation is eating into fixed incomes; and downsizing, aging in place, or tapping into home equity all feel like high-stakes decisions. Almost 80% of Canadians over 55 say their savings and pensions aren’t enough. (Source: Home Equity Bank Ipsos Survey) According to this same survey, half of respondents believe home equity is crucial for retirement—yet 76% feel pressured to downsize even if they’d rather not trade their garden for a balcony (or their favourite hairdresser for whoever’s closest to the condo). What they don’t need: A one-size-fits-all sales pitch from someone who thinks “retirement” means early-bird specials and Sudoku marathons. What they do need: A mortgage broker who listens, educates, compares options, and helps them sleep at night—not just sign on the dotted line. The Missing Link: Transactional vs. Conversion Sales Traditional mortgages are what we call commodities, sold using a transactional method. In this approach, the need is obvious—the customer wants a mortgage—and the focus is on competing for the best price and terms. It’s fast, efficient, and, let’s be honest, a little impersonal. It’s the classic hammer-and-nail approach: every client looks like a nail, and the broker just keeps swinging rates and terms until something sticks. That may work for a first-time buyer chasing the cheapest five-year fix—but for seniors? It’s about as effective as putting a Band-Aid on a broken arm. The 55+ demographic doesn’t want a hammer. They want a conversation. They want to understand how to stretch their pension income, cover rising expenses, and prepare for life’s curveballs—like healthcare costs or home repairs—without feeling like they’re going backwards financially. That’s why this is not a transactional sale; it’s a conversion sale. A transactional sale happens when someone already wants what you’re selling—you’re just facilitating the purchase. A conversion sale, however, is when the client doesn’t yet believe they need or want what you’re offering. You’re not closing a deal; you’re changing a mindset. And that’s the secret sauce for brokers working with older Canadians. You’re not selling debt—you’re offering financial flexibility. You’re helping people reframe home equity from a “last resort” into a retirement resource. How Brokers Can Shift the Conversation Lead with empathy, not economics. Ask about life goals, not loan size. Do they want to age in place, help kids, or reduce financial stress? Start with why, then move to how. Rebrand the conversation. Words matter. “Mortgage” can feel like failure. Try “home-equity strategy” or “retirement cash-flow plan.” You’re not adding debt—you’re unlocking options. Talk cash flow, not contracts. Focus on income versus expenses, inflation resilience, and emergencies. Discuss how home equity can supplement pensions, create predictable, guaranteed income (like our parents had), and—most importantly—boost that all-important sleep score. Include the family. Adult children often play a major role. Involve them early—these are emotional, multi-generational conversations, not just financial ones. Educate, don’t sell. Show examples, calculators, and real-life case studies. Transparency earns trust—and trust is the true currency in a conversion sale. When brokers shift from “rate pitching” to “retirement planning,” they go from hammer-swingers to problem-solvers—and that’s where the real magic (and business growth) happens. What Mortgage Brokers Bring to the Table The broker market is projected to grow at a 5% CAGR through 2030, driven by consumers demanding personalization over cookie-cutter lending. And the reverse-mortgage space just got a serious glow-up. Home Trust Bank has just entered the market, announcing its new Equity Access Reverse Mortgage product at this week's Mortgage Professionals Conference in Ottawa. That brings the total to four active lenders in Canada’s reverse-mortgage space: HomeEquity Bank, Equitable Bank, Home Trust Bank, and Bloom Finance Company. More lenders mean more credibility—or, as I like to call it, street cred for seniors. The kind that lets retirees walk down the street (or the fairway) with a little swagger, knowing their financial toolkit has options. With more players in the mix comes more choice, sharper pricing, and—most importantly—a sense that reverse mortgage products have finally crossed over from “fringe” to financially fashionable. Reverse mortgages are no longer the “we-don’t-talk-about-that” cousin at the financial family dinner—they’re sitting proudly at the adult table. The product is being normalized—treated as the legitimate, strategic retirement tool it has always been. So, brokers—be honest. Isn’t it time you caught up to the trend? Reverse mortgages have gone from taboo to totally credible. And if your clients still say, “We’re just not reverse-mortgage people,” that’s your cue to help them unpack that posture of financial marginalization. Because what they often mean is, “We don’t want to feel old, desperate, or dependent.” That’s not who they are—and that’s not what this product is. It’s not about retreating; it’s about reframing. Helping them see home equity as strength, not surrender. Because empowering clients to live comfortably, confidently, and cash-flow secure isn’t just good business—it’s the kind of advocacy that gives everyone involved a little swagger. Older Canadians Need Advocates—Not Just Advisors As a spokesperson for this group, I urge brokers to master Equity Literacy—the ability to explain complex tools like reverse mortgages and HELOCs in plain language. It’s about helping retirees access equity wisely, preserve benefits, and create peace of mind. Canadian reverse-mortgage debt reached $8.2 billion in mid-2024—an 18.3% year-over-year increase. (Source: Office of the Superintendent of Financial Institutions - OSFI). Canadians are catching on: their house can help them, not haunt them (could not resist the Halloween joke). Help seniors understand the range of uses for Reverse Mortgages like paying off high-interest debt, helping family through early inheritance or gifting, and supplementing retirement income to maintain independence. And here’s where brokers can really shine—by guiding family conversations about inheritance, housing, and aging in place. According to CMHC’s 2025 Mortgage Consumer Survey, 41% of first-time buyers used a gift or inheritance to cover mortgage costs. That's up from 30% the year before. Those gifts averaged nearly $80,000. The Bank of Mom & Dad just got promoted to Wealth Management HQ. To the Canadian mortgage broker industry You’re not just in the mortgage business—you’re in the dignity business. You help Canadians stay in their homes, reduce stress, and live comfortably in retirement. With home sales slowing and fewer purchase deals, this is your moment. Building expertise in the 55+ market isn’t just good karma—it’s good business. How to start: educate your database about equity-release benefits and tax-free cash flow; host workshops on “Aging in Place with Equity”; partner with financial planners, lawyers, healthcare providers—and yes, Realtors—to build a holistic approach to retirement housing. Involve adult children in every conversation; they’re tomorrow’s clients. The data says Canadians need you more than ever. And I’ll say it louder: so do I. Let’s make retirement planning better, smarter, and more human—one conversation at a time. So here’s the truth: the 55+ crowd doesn’t need rescuing—they need respect. They’re not clinging to the past; they’re funding their future. They don’t want pity; they want power—and they’ve earned it. This generation built Canada’s equity base—literally—and now it’s time they get to use it wisely, proudly, and on their own terms. Whether that means a new roof, a family gift, or finally taking that long-postponed trip to Italy, it’s not about borrowing money—it’s about buying freedom. So, brokers, financial pros, and anyone guiding retirees—remember: your role isn’t to sell products. It’s to spark possibilities. To help older Canadians move from fear to freedom, from “we’re not those people” to “why didn’t we do this sooner?” Because the real revolution in retirement isn’t about rates or renewals. It’s about reclaiming confidence, creating financially viable futures, and knowing you’ve made a real difference—something your clients will remember long after the ink dries. Trust me, that’s far more gratifying than handing out a 4.99% five-year fixed. I want to know what you think. Send me your feedback. Want more insights like this? Subscribe to my free newsletter here, where I share practical strategies, real-world stories, and straight talk about navigating retirement with confidence—not confusion. Plus, all subscribers get exclusive early access to advance chapters from my upcoming book. For Canadians 55+: Get actionable advice on making your home equity work for you, understanding your options, and living retirement on your terms. For Mortgage Brokers and Financial Professionals: Learn how to become the trusted advisor your 55+ clients desperately need (and will refer to everyone they know). This isn't just another revenue stream—it's your opportunity to build lasting relationships in Canada's fastest-growing demographic. Sue Don’t Retire…Re-Wire!

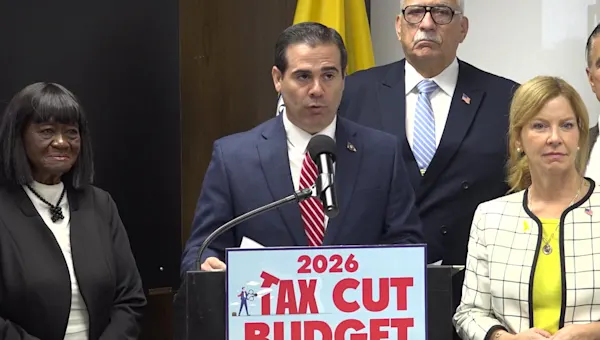

Hempstead Supervisor Announces Tax Cuts

Lawrence Levy, associate vice president and executive dean of the National Center for Suburban Studies, spoke to News 12 Long Island about Hempstead Town Supervisor John Ferretti proposing an 18% tax cut to the general fund for 2026, that he says would result in $5 million savings. Helping to fund the cut would be a reduction in the town’s workforce. “This could be a good thing if the reduction is the result of sound fiscal practices. It could be a bad thing if it’s the result of fiscal gimmicks,” Levy said. “We’re talking about – at best – dollars in savings, not hundreds of dollars, except for the most expensive of properties.

Government Shutdown: LSU Experts Available

As the federal government shutdown continues, LSU finance and economics experts are available to provide insight into its potential consequences—from effects on markets and small businesses to broader economic stability and consumer confidence. Rajesh Narayanan Dr. Narayanan is a leading expert on banking and financial markets whose research and commentary regularly inform policy discussions at central banks and regulatory agencies worldwide. Del Wright Prof. Wright’s research focuses on tax, finance, business, securities, entrepreneurship, and in the last few years, crypto and blockchain regulation.