Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

How the Class of 2026 can keep resumes out of the digital black hole

Students set to graduate this May are entering a job market where the rules of engagement are being rewritten in real-time. AI is both friend and foe, and ghosting has become the norm. University of Delaware career expert Jill Panté shares how college students can navigate these challenges in a rapidly shifting economy. Panté, director of the Lerner Career Services Center at UD, can apply her expertise to the following: The AI recruitment gap • How to prevent resumes from falling into the "digital black hole" of automated tracking systems. • Current recruitment in 2026 is heavily filtered by AI. If resumes don't mirror the language of the job description, a human might never even see it. • In 2026, AI is the gatekeeper. Students who aren’t using AI for assistance are working twice as hard for half the results. However, the goal is to use it as a co-pilot, not an autopilot. Beat the bots (tailor your content) • Use tools like Resume Worded or Generative AI like Microsoft Co-Pilot or Gemini to see how resumes stack up against specific job postings. • It is better to send five highly tailored, thoughtful applications than 50 generic ones that get auto-rejected by an algorithm. • Use AI to run a mock interview based on the job description and company. The "hidden” job market • If a "job search" consists solely of clicking "Easy Apply" on LinkedIn for six hours a day, it’s not searching; it’s just doom-scrolling with a resume. Roughly 80% of your time should be spent talking to humans. The other 20% should be spent on applications and research. • Find the recruiter or a department head on LinkedIn. Send a brief (2-3 sentence) note reiterating your interest. • Leverage alumni networks through LinkedIn. Narrative branding • Especially for Gen Z: Hiring managers don't just want to know what you did; they want to know the impact you made. • Instead of saying "Responsible for social media,” say "Increased engagement by 40% over 3 months by implementing a new video strategy." • Always lead with results (LinkedIn, resume, Interviews) to showcase the value you bring. Workforce anxiety • Managing the mental toll of the modern, high-speed job search and the professional "ghosting" epidemic. • Establish a personal "Board of Directors" to provide a balance of support, accountability and feedback. • Maintain momentum by volunteering, attending local networking events and learning new skills on platforms like LinkedIn Learning and Coursera. To reach Jill Panté directly and arrange an interview, visit her profile and click on the “contact” button.

Energy Shocks, Consumer Pullback, and the Long Road Back

As Americans scale back spending on luxuries and some necessities — from dining out and live entertainment to home and auto maintenance — the ripple effects are being felt across the broader economy. Daniel Burnside, clinical professor of finance at the Simon Business School, says the trend reflects more than just belt-tightening and signals deeper structural pressures tied to energy markets. “Higher energy prices push inflation up and growth down, putting monetary policymakers in a bind,” Burnside says, explaining the current situation as being beyond a typical price spike. “This isn’t just a price shock, it’s a capacity shock,” he says. “You can’t just flip a switch back to normal because a lot of energy infrastructure has been destroyed. That distinction matters. Because energy costs are embedded in nearly every good and service, rising prices squeeze consumers beyond the gas pump. The result is reduced discretionary spending at venues like sporting and live music events, restaurants, and leisure destinations. Looking ahead, Burnside says a rapid rebound in discretionary spending is possible but unlikely. “If, by some miracle, energy prices quickly return to prewar levels, you would see a sharp run-up in discretionary stocks,” he says. “But that’s precisely because expectations are so low.” For now, markets are signaling that a swift return to pre-crisis conditions isn’t on its way, Burnside says. Until energy supply stabilizes, the pressure on both consumers and the businesses that rely on it is likely to persist. Burnside regularly fields inquiries from journalists looking for his insight on personal money matters and investing. Contact him by clicking on his profile.

Covering Cuba? Augusta has one of the leading experts ready to help with your coverage

Cuba is facing one of its most severe crises in decades, as compounding economic and energy challenges continue to strain everyday life on the island. Persistent fuel shortages have led to rolling blackouts, transportation disruptions, and reduced industrial output, while inflation and shortages of basic goods have eroded purchasing power for ordinary Cubans. Tourism, once a critical source of foreign exchange, has struggled to fully recover, and the country continues to grapple with declining productivity and limited access to international capital. These pressures have contributed to rising public frustration, increased migration, and a government response that blends cautious economic reforms with efforts to maintain stability. Paolo Spadoni is an ideal expert for journalists covering this evolving situation. As a specialist in Cuba’s political economy, his work focuses on the island’s external sector, including foreign investment, remittances, tourism and the impact of international sanctions. He brings a rare ability to connect on-the-ground developments – such as energy shortages or policy changes, to the broader structural realities shaping Cuba’s economy. With deep academic research and ongoing analysis of current reforms, Spadoni offers clear, credible insight into whether Cuba’s latest measures signal meaningful transformation or simply short-term responses to a prolonged crisis. Paolo Spadoni, PhD, is a widely recognized expert on Cuba and its international relations. He is a tri-lingual political economist with a specialization in international relations and a focus on Latin America’s political and business environments. His research focuses on international relations theories, Cuba's economy and business market, foreign investment in Cuba and U.S.-Cuba relations. View his profile Since this crisis escalated, Spadoni has been the 'go-to' expert for reporters with media from across North America like Reuters, Bloomberg and The New York Times connecting with him for his expertise, input and perspective on the situation. LA TERCERA: “The Cuban tourism sector was already struggling before the Covid pandemic. The best year for international tourism in Cuba was 2017 in terms of foreign exchange earnings. That was the year in which $3.3 billion was collected, and tourism represented 10% of Cuba's GDP at that time. In terms of employment, it provided 120,000 direct jobs and roughly 500,000 indirect jobs. So it played a significant role. That was the best year for international tourism in Cuba, which coincidentally ended in November of that year with the sanctions imposed by the first Trump administration. From then on, tourism from North American visitors began to decline, but European and Canadian visitors were already decreasing,” Spadoni explained to La Tercera. CBC NEWS: "Most of those investments are real estate investments more than tourism investments, meaning the Cuban military has taken possession of prime locations in the best tourism areas of Cuba," said Paolo Spadoni, an associate professor at Augusta University in Augusta, Ga., and co-author of the 2025 book The Cuban Tourism Industry: Evolution, Challenges and Prospects. Columbia Law School: "While seeking to finalize an economic agreement with Cuba, the Trump administration could secure deals across various sectors of the economy. However, tourism holds the most promising opportunities in the short term." Global News (Canada):

Iran Conflict Intensifies Focus on Affordability

Professor of Finance Anoop Rai spoke to Newsday about economic fallout from the Iran campaign, which is refocusing attention on rising costs at a time when affordability was already a top concern, locally and nationally. If the economy cools down, it could reduce the state’s tax revenues, and any actions lawmakers take to further help with affordability could lead to greater deficits, said Dr. Rai. “Then it becomes more like a philosophy. Do you help now during bad times and then try to recover later, or stick to your principles and say ‘tough luck’?”

MEDIA RELEASE: Manitobans paying more for vehicle repairs as CAA Worst Roads campaign launches

Submitted photo of Saskatchewan Avenue, Winnipeg’s Worst Road in 2025. Manitobans are paying more out of pocket to fix their vehicles as concerns about road conditions continue to grow, according to new survey data released as CAA Manitoba launches its annual CAA Worst Roads Campaign. The survey found 92 per cent of Manitobans are concerned about the state of roads in the province and are spending an average of $944 to repair vehicle damage caused by poor road conditions. This is $122 more than last year, when the average repair cost was $882. As Winnipeg grows and congestion worsens, fixing key trade and connector routes isn’t just about road conditions; it’s about protecting the economy, keeping our city moving, and prioritizing affordability. “Most of the roads people flag as priorities are the same routes our supply chain depends on, they’re how goods get in, out, and across the province,” says Ewald Friesen, manager, government and community relations for CAA Manitoba. “With Manitoba’s growing population, especially in Winnipeg, there is a need for improved infrastructure.” At the same time, the rising cost of living has made consumers more mindful of their spending, and people are opting to keep their cars longer rather than buy a new one. Poor roads increase the wear and tear of tires, lead to higher fuel consumption, and increase the risk of other costly repairs. Nearly half of drivers (45 per cent) reported experiencing vehicle damage due to poor road conditions, with potholes cited as the leading cause, accounting for 86 per cent of damage. Most drivers (75 per cent) are paying for repairs out of pocket; 12 per cent filed a claim with Manitoba Public Insurance. Another 14 per cent said they chose not to repair the damage, up six per cent from last year. Despite widespread frustration, the survey suggests most concerns are not reaching decision-makers. It found that 85 per cent of Manitobans commonly complain about road conditions to a spouse, coworker or mechanic rather than to the governments responsible for road maintenance. Manitobans encouraged to nominate roads most in need of repair “The Worst Roads campaign is a proven platform that gives Manitobans a voice and helps governments identify the roads causing the most frustration,” says Friesen. “We know it works because we see governments prioritize budgets and move up road repairs every year after appearing on the list.” Manitobans can nominate any road for issues, including potholes, congestion, faded road markings, poor signage, traffic light timing, and pedestrian or cycling infrastructure. CAA Manitoba is encouraging all road users to participate. Nominations are open at www.caaworstroads.com from March 17 to April 10. Once nominations close, CAA Manitoba will release a list of the top 10 worst roads in the province, along with regional lists. CAA conducted an online survey with 649 CAA Manitoba Members between January 6 to 14, 2026. Based on the sample size and the confidence level (95 per cent), the margin of error for this study was +/-3 per cent.

Retirement Maxxing: How Small Decisions Help You Build a Better Future

The basic idea is to pick a corner of your life and optimize it ruthlessly. Sleep maxxing. Health maxxing. Productivity maxxing. In its more extreme corners, people are attempting to optimize their actual physical features. Go ahead and Google "looksmaxxing" if you are curious and have a strong constitution. One influencer named Clavicular — a 20-year-old from Hoboken who claims to have taken a literal hammer to his face to coax a chiselled jawline — has become the reigning king of this particular rabbit hole. Medical experts would prefer you not try that at home. The Globe and Mail published a comprehensive explainer on the whole phenomenon. The Republican National Committee put out a press release praising Donald Trump for "jobsmaxxing" the economy. The Department of Defence posted a soldier with the caption "lethality maxxing." It has become, as one writer put it, the suffix that just will not quit. Retirement Maxxing: because chin waxing, I mean maxxing, was already taken. And yet, buried beneath all the absurdity, the underlying impulse is not entirely ridiculous. Humans want to optimize things. We always have. The real question is whether we are optimizing the right things. Then, as these things sometimes happen, three articles landed in my inbox in the same week and refused to leave my mind. Maxxing. The psychology of future selves. A golfer named Max Greyserman, who sits just one-tenth of a stroke from the top of his sport. I am not a woman who ignores signs. The connection was obvious once I saw it: retirement might be the most important time to apply this kind of thinking. Not the obsessive version involving ice baths and fourteen supplements before breakfast. The practical version. Thoughtful maxxing that quietly stacks the odds in your favour over decades. Retirement isn't just one decision; it's hundreds made over the years, each guiding your future self toward either financial dignity or a Shaggy tribute tour you never signed up for. The “Shaggy Problem”: How Your Retirement Decisions Today Determine Your Financial Security Tomorrow You remember Shaggy. The reggae artist. Enormous hit. "It Wasn't Me." When it comes to retirement, it absolutely was you. Every decision you make today is writing a letter to your future self. Some of those letters are generous and thoughtful. Others arrive decades later, like a bill you forgot to pay, from a creditor with excellent memory and zero sympathy. The seventy-five-year-old version of you hopes the fifty-five-year-old paid attention. The eighty-five-year-old version would very much like functioning knees, a dignified income, and the ability to say "I planned for this" rather than "I did not think it would go this fast." It went that fast. That's why the most useful habit you can develop right now is what I call the future-self test. Before making a major financial or lifestyle decision, pause and ask: how will this look from the other end? Will I still think this tattoo is a good idea when I’m ninety? Will I regret staying in a house that is too large and too expensive for another decade? Will my future self thank me for delaying CPP, or curse me for taking it early because waiting felt uncomfortable? Or as the Beatles asked rather memorably: “when I'm sixty-four, will you still need me, will you still feed me?” The song is charming. The financial planning version is considerably less so if you have not thought it through. The future-self test is not complicated. It is just the habit of writing better letters. What Sports Analytics Can Teach Us About Smarter Retirement Decisions Speaking of decisions that come back to haunt you, let's discuss probabilities. A recent New York Times article about golfer Max Greyserman stopped me mid-scroll (Lindgren, 2026). Not because of the golf — though the golf is fascinating — but because of what it revealed about the gap between what the data says and what people actually do when the stakes are high. Greyserman's scoring average is less than one-tenth of a stroke per round away from the elite level. One-tenth of a stroke. Not a full swing, a putting mistake, or a collapse on the eighteenth. The difference between obscurity and greatness in pro golf is about the time it takes to find your reading glasses. Which, as we've established, were on your head the entire time. Hockey analytics have demonstrated that teams trailing late in a game should often pull the goalie much earlier than the traditional last-ninety-seconds rule. Research indicates that pulling the goalie around the eight-minute mark can significantly boost the chances of scoring, as the extra attacker alters the odds. However, most coaches still wait until the final minute or two. Why? Because if you pull the goalie at eight minutes and lose badly, it can look like you lost your mind. The math checks out, but the optics are terrifying. Soccer offers a similarly uncomfortable example. A widely cited study analysing thousands of penalty kicks found that about one-third of kicks are aimed straight down the middle of the net, yet goalkeepers stay in the centre only around six percent of the time (Chiappori, Levitt, & Groseclose, 2002). Shooting directly down the middle often provides good odds because the keeper has already committed to diving one way or the other. But if the goalkeeper stays put and makes the save, the kicker seems to have tried to outsmart the odds and failed. The math checks out. The optics, however, are still terrifying. Retirement is filled with these moments. And most people make their decisions based on the optics. Common Retirement Decisions Canadians Get Wrong — And What the Data Actually Says: Working a couple of extra years often delivers significantly better retirement outcomes, yet people retire early because they feel emotionally ready. Delaying CPP can greatly increase guaranteed lifetime income, yet many choose to claim early because waiting seems risky. Downsizing can free up cash and lessen financial stress, yet people stay in large homes because selling feels like giving up. Using home equity wisely can boost retirement income, yet many retirees dismiss this option because of a stigma rooted in outdated beliefs rather than current data. In each case, the emotionally comfortable choice is not the one with the best long-term odds. Fear of loss, fear of regret, fear of looking foolish — those emotions sprint ahead of rational thinking every single time. That is why the future-self test matters. Math is universal, but money is deeply personal, and the goal is to let one inform the other before it is too late. The Psychology of Retirement Saving: Why We Treat Our Future Self Like a Stranger The second New York Times article examined the psychology of how we connect with our future selves (The New York Times, 2026). The findings are humbling. Psychologists have discovered that people often see their future self almost like a stranger, which explains why saving for retirement can seem somewhat punishing. It feels less like helping yourself and more like sending a cheque to someone who shares your cheekbones but whose problems seem distant and abstract. Research led by Hal Hershfield found that when people feel more connected to their future selves, they save more and make consistently better long-term financial decisions (Hershfield, 2011). Retirement planning is not just about spreadsheets and withdrawal rates. It is about being genuinely generous towards the person you are becoming. It is a love letter, written in small decisions, over a very long time. So, write a good one. Your future self is counting on you. How to Optimize Your Retirement: A Practical Framework for Canadians If retirement maxxing were a lifestyle trend — and I am formally proposing that it should be — it wouldn’t involve bone-smashing or extreme jawline enhancement. It would look more like this. Health Maxxing: Why Strength and Mobility Are Financial Assets Move your body. Lift weights now and then. Walk up hills. Muscle strength is one of the most underrated assets for retirement that nobody discusses at dinner parties. Research from the National Institute on Aging confirms that strength training improves mobility, balance, and healthy longevity (National Institute on Aging, 2023). These are the very factors that influence whether your later years feel like a gift or a burden. People hesitate over the cost of a gym membership while ignoring the significant long-term benefit of staying upright, independent, and capable. Skipping exercise to save a few dollars is like stepping over a hundred-dollar bill to find a quarter. As Aunt Equity likes to say: be careful not to get out over your skis. (Yes, that was an exercise metaphor. You’re welcome.) Income Maxxing: How to Build Reliable Cash Flow That Lasts Build reliable income streams so you can sleep at night without one eye on the market. Pensions, annuities, dividends, home equity, and carefully structured withdrawals — these all play a role in a well-crafted retirement income plan. The goal isn’t to maximize a single number – it’s to reduce the worry behind all of them. If your retirement plan currently makes you watch financial news at midnight while eating crackers over the sink, something has gone wrong and we should talk. Purpose Maxxing:Why It Matters for Your Health and Longevity Retirement is not a forty-year holiday. Humans need purpose, connection, and something worth getting out of bed for — especially on days when nobody expects you anywhere and the morning is entirely, terrifyingly yours. NIH research consistently shows that social engagement and a sense of purpose are linked to better health and longer life (National Institute on Aging, 2023). Purpose is what makes a retirement that feels like freedom different from one that feels like a long Sunday afternoon with nowhere to go. Somewhere along the way, society decided that aging meant quietly fading into the background. Retirement is when you finally have permission to dye your hair a vibrant colour, volunteer somewhere meaningful, start a project that genuinely excites you, or do all three at once and totally surprise your grandchildren. Purpose is not optional. It is the foundation. Decision Maxxing: How to Overcome Emotional Bias Use data when the stakes are high. Emotions are useful for choosing dessert but much less reliable for planning a thirty-year income. Don't swat away analytics like a fly at a family picnic just because they suggest something uncomfortable. Run projections. Stress-test your plan. Understand probabilities. Pull the goalie early if the math indicates so, even if it looks odd at the moment. Because appearing odd now and being wrong later are not the same thing. Not even close. The Ending That Brings It All Together: Small Decisions That Compound Over Time Here’s what three articles about “maxxing” our future selves, and golf, taught me about retirement. Clavicular is out there taking a hammer to his face in pursuit of optimization. Max Greyserman is grinding for one-tenth of a stroke. Hal Hershfield is reminding us that we treat our future selves like strangers when we should treat them like people we love. And somewhere between all three of them is the retirement insight that really matters: the best decisions compound quietly. Tiny improvements in health, income strategy, purpose, and decision-making build up into dramatically different outcomes over decades. Not because of one dramatic move, but because of many small, sensible ones made with the future in mind. Your future self isn't a stranger waiting to judge you. They are the person you are intentionally becoming, shaped by every decision you make today. Perform the future-self test before making risky decisions like pulling the goalie, shooting down the middle, or getting a tattoo that might lead to an awkward chat with your colonoscopy technician (this is for you, JK). Consider whether your fifty-five-year-old self is being kind to your seventy-five-year-old self. Look at what the data says, not just what feels right. Retirement maxxing isn't about perfection. It's about making small, sensible decisions consistently and thoughtfully over time. Think of it as compound interest for your future self. Einstein allegedly called compounding the most powerful force in the universe. He was talking about money, but he might as well have been talking about the small, steady choices that create a retirement worth living. Your future self will be deeply grateful—having functional knees, a dignified income, and a tattoo they still absolutely love. And when you turn sixty-four, and someone asks how you got there so gracefully, you won't need to channel your inner Shaggy. You just smile and say: It was me! Sue Don’t Retire…ReWire! P.S. Aunt Equity approves. Ready to start retirement maxxing? Here are two things you can do today. Run the future-self test on one financial decision you have been avoiding. Just one. Write down what your seventy-five-year-old self would think of the choice you are leaning toward. You might be surprised what comes up. Move your body and find your people. Join a pickleball club, a walking group, a trivia night, or a bridge league. Laugh often. Sweat occasionally. Your future self needs both, and your colonoscopy technician will be thrilled. Want more insights like this? Subscribe to my free newsletter here, where I share practical strategies, real-world stories, and straight talk about navigating retirement with confidence—not confusion. Plus, all subscribers get exclusive early access to advance chapters from my upcoming book. For Canadians 55+: Get actionable advice on making your home equity work for you, understanding your options, and living retirement on your terms. For Mortgage Brokers and Financial Professionals: Learn how to become the trusted advisor your 55+ clients desperately need (and will refer to everyone they know). This isn't just another revenue stream—it's your opportunity to build lasting relationships in Canada's fastest-growing demographic.

War in Iran: Impact on Oil Prices

As global markets respond to escalating tensions in Iran, energy prices are once again at the center of international concern. For insight into what this conflict could mean for oil markets, consumers and the broader economy, media can turn to Greg Upton, executive director and associate research professor at the LSU Center for Energy Studies. An expert at the intersection of energy and environmental economics, Upton studies how geopolitical disruptions, supply constraints and policy decisions influence oil prices and downstream economic impacts. As instability in the Middle East threatens global supply chains, he can provide context on potential price volatility, implications for Louisiana’s energy sector and what higher crude prices may mean for gasoline costs and inflation in the United States. Upton has contributed to more than 40 academic publications and has presented his research to over 200 industry, government and academic audiences. He has testified before committees in both chambers of the Louisiana Legislature and a subcommittee of the U.S. House of Representatives. A frequent voice in national and local media, Upton has been quoted or cited more than 250 times, including by the The Wall Street Journal, The New York Times, USA Today and NPR. In addition to his research, Upton teaches in LSU’s MBA program and in the Department of Economics and Environmental Sciences, helping prepare the next generation of leaders to navigate complex energy and environmental challenges. For timely, data-driven analysis on the impact of oil price fluctuations amid the ongoing conflict in Iran, Dr. Greg Upton is available for interviews and expert commentary.

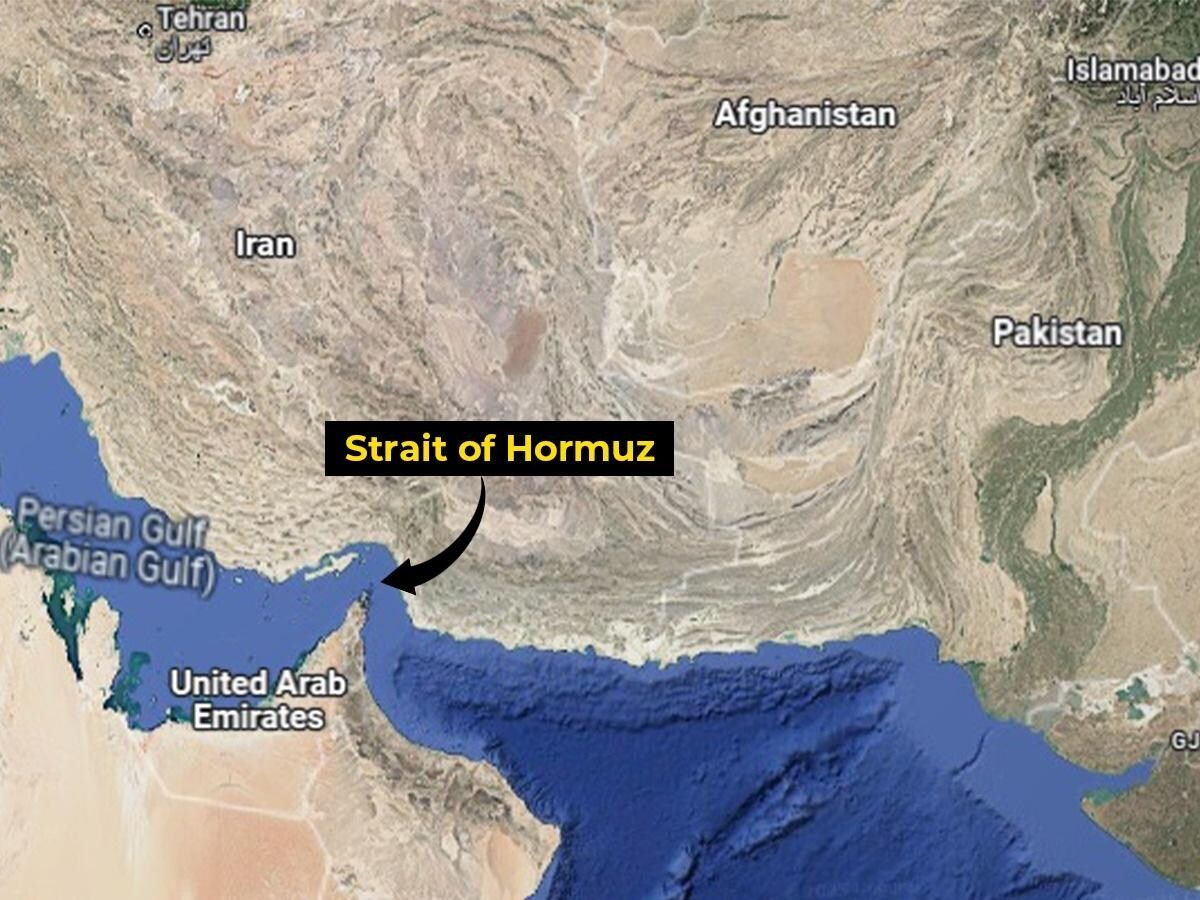

ExpertSpotlight: Why the Strait of Hormuz Matters: The World’s Most Critical Chokepoint

The Strait of Hormuz is one of the most strategically vital waterways on Earth. Just 20 miles wide at its narrowest point, with shipping lanes only a few miles across in each direction, this narrow channel connects the Persian Gulf to the Gulf of Oman and the Arabian Sea. Through it flows roughly one-fifth of the world’s petroleum supply, along with vast quantities of liquefied natural gas, particularly from Qatar. For global markets, the Strait is more than geography, it is a pressure point. Any disruption, even the threat of one, can send oil prices surging and rattle financial markets worldwide. A History Shaped by Empire and Energy For centuries, the Strait served as a maritime corridor linking Mesopotamia, Persia, India, and East Africa. Control over it shifted between regional powers, colonial empires, and eventually modern nation-states. In the 16th century, the Portuguese seized nearby islands to dominate regional trade routes. Later, British naval power asserted influence during the height of imperial shipping dominance. In the 20th century, however, the Strait’s importance expanded dramatically with the rise of oil exports from Gulf states. After the 1979 Iranian Revolution, tensions surrounding the Strait intensified. During the Iran-Iraq War in the 1980s, particularly the so-called “Tanker War” phase, commercial vessels were targeted, highlighting how vulnerable global energy supplies could be. Since then, periodic confrontations between Iran, the United States, and regional powers have kept the Strait at the centre of geopolitical risk. Why It Is So Important Today 1. Energy Security Major oil producers including Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar rely heavily on this route. Even short-term closures could disrupt millions of barrels per day in global supply. 2. Global Economic Stability Because oil is globally traded and priced, disruptions in the Strait impact fuel costs, inflation, shipping, and consumer prices worldwide — including in North America and Europe. 3. Military Strategy The Strait is bordered primarily by Iran to the north and Oman to the south. Iran has periodically threatened to close the passage in response to sanctions or military pressure. The U.S. Navy and allied forces maintain a consistent presence to ensure freedom of navigation. 4. Modern Geopolitical Flashpoint Recent decades have seen drone seizures, tanker detentions, and naval standoffs. Each incident reinforces how fragile global energy logistics can be when concentrated in a single corridor. The Strait as a Symbol of Interdependence The Strait of Hormuz underscores a central truth of globalization: the world’s economies are deeply interconnected and geographically vulnerable. A narrow stretch of water in the Middle East can influence gasoline prices in Ontario, manufacturing costs in Germany, and energy security debates in Asia. It is both a trade artery and a geopolitical lever — a reminder that geography still shapes global power. Expert Angles for Media An expert in geopolitics, energy economics, or maritime security could explore: How vulnerable is the global economy to a prolonged closure? Can alternative pipelines realistically replace Hormuz traffic? What role do regional alliances play in deterring conflict? How does the Strait shape Iran’s negotiating power? What would insurance and shipping markets do in a crisis? The Strait of Hormuz is not simply a map feature — it is one of the world’s most consequential strategic chokepoints. Its stability underpins global energy flows, economic predictability, and international security. If tensions rise there, the world feels it. Our experts can help! Connect with more experts here: www.expertfile.com

Exploring everyday finance, gender, and the future of pensions

Money in everyday life For Dr Hayley James, finance isn’t just numbers on a balance sheet - it’s woven into the realities of everyday life. From saving and borrowing to the challenge of long-term pension planning, her work at Aston University’s Centre for Personal Financial Wellbeing (CPFW) explores how financial decisions are shaped by family, gender, life stage, and stability of income. Her research stems from her PhD, which examined how people make decisions after being automatically enrolled into workplace pensions - a starting point that sparked her continuing focus on pensions and everyday financial behaviour. “Finance is often portrayed as objective, but in reality, our money decisions are tied up with all the other meaningful factors in our lives.” – Hayley James At CPFW, Dr. James and her colleagues have observed a shift in policy and industry thinking. Where once the focus was on pushing people to act in “rational” financial ways, attention is now turning to redesigning systems that reflect how people actually manage money. Gender and the pension gap A key focus of Dr. James’ research has been pensions, particularly how gender and life events shape saving habits. She has found that parenthood has very different impacts on men and women’s retirement planning: Motherhood often discourages pension saving - reducing both capacity and perceived importance. Fatherhood often encourages saving - reinforcing traditional financial roles. While many assume household specialisation balances out, reality shows otherwise: separation or divorce often leaves women financially disadvantaged. These insights underpin her book Pension Saving in a Gendered Lifecourse (2025), which argues for pension systems that move beyond gender neutral models to become gender friendly - systems that acknowledge the very different realities men and women face across their life course. Tracking real lives: the “Real Accounts” project Beyond pensions, Dr James has led research into how people actually manage day-to-day finances. In the Real Accounts project, she and colleagues followed UK households for 10 months, recording income and spending in real time. The findings reveal how income volatility — sudden drops, irregular hours, unexpected bills — creates stress and undermines financial stability. These insights are helping policymakers and providers rethink how products like pensions, credit, and debt advice are designed. Collaboration and impact Dr. James’ work bridges academia, policy, and practice. Partnerships include: Nest Insight – public-benefit research centre, co-leads on Real Accounts. Glasgow Caledonian University – joint research on household finances. Christians Against Poverty – literature review on measuring the impact of debt advice, aimed at improving frontline support for the most vulnerable. Through these collaborations, her findings are already shaping practical change in how organisations design support for households under financial strain. Looking ahead With her British Academy Innovation Fellowship concluding, Dr. James is turning to new questions: How do diverse households — across sexuality, ability, ethnicity, and household structure — navigate finance? How can financial systems evolve to reflect real lives, not abstract models? Her book sets out a roadmap for rethinking pensions through a gendered lens — offering policymakers, providers, and households a new way to understand and prepare for later life. Selected publications For readers who want to explore her research in more depth, here are a few recent publications: • James, H. (2022). Everyday finance and the politics of financial subjectivity. Review of International Political Economy. • James, H. (2022). Financial wellbeing and the lived experience of income volatility. New Political Economy. • James, H. (2023). Household finance and the gendered lifecourse: Reframing pensions research. In Handbook on Everyday Finance (Edward Elgar). Available via RePEc. ⸻ About Dr. Hayley James Dr. Hayley James is a Senior Research Fellow at Aston University’s Centre for Personal Financial Wellbeing. Her research spans pensions, household finance, and the social context of money. She has published widely and works closely with policy and community partners to translate research into action. To explore more of the Centre’s work and access project reports, visit the CPFW Projects page at Aston University. Connect with Hayley by clicking the profile icon below.

Need a tourism expert? Connect with Florida Atlantic today

Tourism is a cornerstone of both Florida’s and America’s economy. In Florida alone, visitor spending exceeds $100 billion annually and supports roughly one in every ten jobs statewide, making it one of the state’s largest industries. The ripple effect extends far beyond hotels and attractions, fueling restaurants, retail, transportation, construction, real estate, and public tax revenues that help fund infrastructure and services. Nationally, tourism contributes hundreds of billions to U.S. GDP each year and serves as a key indicator of consumer confidence and economic momentum. When travel demand rises or falls, it signals broader shifts in spending behavior, business investment, and workforce stability , which is why tourism remains a critical economic beat for journalists. Peter Ricci is Clinical Associate Professor & Director, Hospitality Management Programs at Florida Atlantic University. He is a hospitality industry veteran with over 20 years of managerial experience in segments including: food service, lodging, incentive travel, and destination marketing and is considered an expert in food service, lodging, incentive travel, and destination marketing. View his profile Peter offers research-based insight into visitor trends, workforce dynamics, and destination strategy. His expertise helps media connect travel patterns to economic impact, providing clear analysis of how tourism shapes Florida’s economy and influences broader industry trends across the United States. Recent media coverage: South Florida Sun Sentinel Peter Ricci, director of the hospitality and tourism management program at Florida Atlantic University’s College of Business, cited the openings of the 801-room Omni Hotel next to the county convention center in Fort Lauderdale, the revamped Pier Sixty-Six Resort nearby and a variety of high-profile events as reasons for promising visitor traffic this year. “South Florida should expect to have a relatively strong 2026 with major events in the area [PGA Tournament, Formula 1, et al] and the Southern White House of Mar-a-Lago enhancing higher average daily rates in The Palm Beaches,” he said by email. “Broward is perfectly positioned to capture demand both to its south and north and I expect that hotels and restaurants will have a good year ahead,” he added. Newsweek "The tariffs, staffing shortage, perception of it being difficult to emigrate to the USA, and any possible anti-USA sentiment all go into the 'ingredients of the soup' as I call it," Peter Ricci, Director of Florida Atlantic University's Hospitality and Tourism program, told Newsweek. South Florida Sun Sentinel This is actually a complicated process behind the scenes, said Peter Ricci, director of the hospitality and tourism management program at Florida Atlantic University in Boca Raton. “Restaurant profit margins are slim, so training and development are often not a part of the process,” he said. “Also, one must recognize that restaurant front-of-house roles are somewhat high-turnover compared to other industries. With higher turnover, there is less likelihood for development of training, knowledge of all the systems (which can lead to dissatisfaction among guests), and a ‘new face’ every time regular guests return to the venue.” The Daytona Beach News-Journal When asked if Florida is experiencing a "restaurant apocalypse," Ricci said, "I don't see that as the case. I don't see it like a disaster, but I have seen more (restaurant) closures the past six months. The reasons include operating costs that are higher than ever in an industry with low (profit) margins to begin with." "Closures are being driven by rising rent, rising costs of labor, rising costs of goods (food, glassware, supplies, cleaning services, deep cleaning surcharges, et al.), and changing consumer habits." Orlando Sentinel Peter Ricci, director of the hospitality and management program at Florida Atlantic University’s College of Business, said he has not heard of hoteliers suddenly losing foreign nationals from their staff. But it’s the confusion that is perplexing many. “I hear frustration and confusion of what changes will occur on a regular basis for owners, operators and managers,” Ricci said. “It’s more of the unknown that’s disconcerting than, ‘I’m now worried about losing workers in my hotel or restaurant.’”