Experts Matter. Find Yours.

Connect for media, speaking, professional opportunities & more.

20 Days Into the Government Shutdown: What’s the Impact on Your Wallet?

"Government shutdowns create a cascading financial impact that begins with federal workers but quickly spreads throughout the economy, with effects intensifying the longer the shutdown persists. Approximately 2 million federal civilian employees face direct financial disruption during shutdowns. Essential personnel in national security and public safety continue working without immediate pay, while non-essential workers are furloughed entirely. Although Congress typically authorizes back pay after shutdowns end, families must navigate weeks or months without regular income, forcing them to drain savings, incur debt, or miss critical payments like mortgages and utilities. Federal contractors face even greater uncertainty, as they often receive no compensation for shutdown periods, creating immediate cash flow crises for businesses of all sizes that depend on government work. The financial impact extends well beyond federal employees through several key transmission mechanisms. Reduced consumer spending from affected workers hits local businesses particularly hard, especially in areas with high concentrations of federal employment like Washington D.C. and military communities. Small businesses face additional challenges through delayed government contract payments and suspended access to Small Business Administration (SBA) loan processing. Critical financial services experience significant disruptions. Federal Housing Administration (FHA) and Veterans Affairs (VA) mortgage approvals slow or halt entirely, delaying home closings and affecting real estate markets. The Internal Revenue Service (IRS) may delay tax refunds and income verification services, further constraining household cash flow and complicating loan applications. Financial markets typically experience increased volatility during shutdown periods, as uncertainty about government stability affects investor confidence. Consumer confidence also tends to decline, particularly during prolonged shutdowns, leading to reduced spending that can amplify economic impacts. Credit rating agencies have historically warned that extended shutdowns could threaten the nation's credit rating, potentially raising borrowing costs across the economy. For most Americans whose income doesn't flow through federal channels, immediate wallet impact remains modest initially. However, the longer shutdowns persist, the more likely average citizens will experience effects through delayed services, financing complications, reduced economic confidence, and broader market softness. The cumulative impact grows exponentially with duration, making swift resolution critical for maintaining economic stability."

Why Brokers Are Canada’s New Mortgage Rockstars

There’s a quiet revolution happening in Canadian mortgage lending—well, as “quiet” as anything can be when two-thirds of Canadians are shouting, “We’d rather deal with a broker than a bank!” According to the most recent Mortgage Professionals Canada (MPC) Consumer Survey, 67% of Canadians now say they’d rather work with a mortgage broker than a bank. Among those who already have? A whopping 81% would do it again. That’s not just a statistic. That’s a standing ovation. The Great Mortgage Broker Boom According to recent MPC data, broker market share reached 33% in 2024—a four-point increase in just two years. Nearly half of all borrowers now choose brokers. The message is clear: Canadians are tired of sales reps; they want advocates who speak human, not policy manual. And who can blame them? With 1.2 million mortgages renewing in 2025 and average payments increasing by $513 a month, people aren’t just rate-shopping anymore—they’re seeking guidance, reassurance, and maybe a bit of hope. Let’s face it: they want their cake and still be able to heat their home too. Why This Matters—Especially for Seniors I work with Canadians aged 55+ every day, and about three-quarters of them are homeowners. They’ve done everything right: worked hard, paid off debt, raised families, and built wealth through their homes. But now, many feel… trapped by them. Here’s the reality: Mortgage renewals are costing hundreds more monthly (some facing 15–20% jumps) Inflation is eating into fixed incomes; and downsizing, aging in place, or tapping into home equity all feel like high-stakes decisions. Almost 80% of Canadians over 55 say their savings and pensions aren’t enough. (Source: Home Equity Bank Ipsos Survey) According to this same survey, half of respondents believe home equity is crucial for retirement—yet 76% feel pressured to downsize even if they’d rather not trade their garden for a balcony (or their favourite hairdresser for whoever’s closest to the condo). What they don’t need: A one-size-fits-all sales pitch from someone who thinks “retirement” means early-bird specials and Sudoku marathons. What they do need: A mortgage broker who listens, educates, compares options, and helps them sleep at night—not just sign on the dotted line. The Missing Link: Transactional vs. Conversion Sales Traditional mortgages are what we call commodities, sold using a transactional method. In this approach, the need is obvious—the customer wants a mortgage—and the focus is on competing for the best price and terms. It’s fast, efficient, and, let’s be honest, a little impersonal. It’s the classic hammer-and-nail approach: every client looks like a nail, and the broker just keeps swinging rates and terms until something sticks. That may work for a first-time buyer chasing the cheapest five-year fix—but for seniors? It’s about as effective as putting a Band-Aid on a broken arm. The 55+ demographic doesn’t want a hammer. They want a conversation. They want to understand how to stretch their pension income, cover rising expenses, and prepare for life’s curveballs—like healthcare costs or home repairs—without feeling like they’re going backwards financially. That’s why this is not a transactional sale; it’s a conversion sale. A transactional sale happens when someone already wants what you’re selling—you’re just facilitating the purchase. A conversion sale, however, is when the client doesn’t yet believe they need or want what you’re offering. You’re not closing a deal; you’re changing a mindset. And that’s the secret sauce for brokers working with older Canadians. You’re not selling debt—you’re offering financial flexibility. You’re helping people reframe home equity from a “last resort” into a retirement resource. How Brokers Can Shift the Conversation Lead with empathy, not economics. Ask about life goals, not loan size. Do they want to age in place, help kids, or reduce financial stress? Start with why, then move to how. Rebrand the conversation. Words matter. “Mortgage” can feel like failure. Try “home-equity strategy” or “retirement cash-flow plan.” You’re not adding debt—you’re unlocking options. Talk cash flow, not contracts. Focus on income versus expenses, inflation resilience, and emergencies. Discuss how home equity can supplement pensions, create predictable, guaranteed income (like our parents had), and—most importantly—boost that all-important sleep score. Include the family. Adult children often play a major role. Involve them early—these are emotional, multi-generational conversations, not just financial ones. Educate, don’t sell. Show examples, calculators, and real-life case studies. Transparency earns trust—and trust is the true currency in a conversion sale. When brokers shift from “rate pitching” to “retirement planning,” they go from hammer-swingers to problem-solvers—and that’s where the real magic (and business growth) happens. What Mortgage Brokers Bring to the Table The broker market is projected to grow at a 5% CAGR through 2030, driven by consumers demanding personalization over cookie-cutter lending. And the reverse-mortgage space just got a serious glow-up. Home Trust Bank has just entered the market, announcing its new Equity Access Reverse Mortgage product at this week's Mortgage Professionals Conference in Ottawa. That brings the total to four active lenders in Canada’s reverse-mortgage space: HomeEquity Bank, Equitable Bank, Home Trust Bank, and Bloom Finance Company. More lenders mean more credibility—or, as I like to call it, street cred for seniors. The kind that lets retirees walk down the street (or the fairway) with a little swagger, knowing their financial toolkit has options. With more players in the mix comes more choice, sharper pricing, and—most importantly—a sense that reverse mortgage products have finally crossed over from “fringe” to financially fashionable. Reverse mortgages are no longer the “we-don’t-talk-about-that” cousin at the financial family dinner—they’re sitting proudly at the adult table. The product is being normalized—treated as the legitimate, strategic retirement tool it has always been. So, brokers—be honest. Isn’t it time you caught up to the trend? Reverse mortgages have gone from taboo to totally credible. And if your clients still say, “We’re just not reverse-mortgage people,” that’s your cue to help them unpack that posture of financial marginalization. Because what they often mean is, “We don’t want to feel old, desperate, or dependent.” That’s not who they are—and that’s not what this product is. It’s not about retreating; it’s about reframing. Helping them see home equity as strength, not surrender. Because empowering clients to live comfortably, confidently, and cash-flow secure isn’t just good business—it’s the kind of advocacy that gives everyone involved a little swagger. Older Canadians Need Advocates—Not Just Advisors As a spokesperson for this group, I urge brokers to master Equity Literacy—the ability to explain complex tools like reverse mortgages and HELOCs in plain language. It’s about helping retirees access equity wisely, preserve benefits, and create peace of mind. Canadian reverse-mortgage debt reached $8.2 billion in mid-2024—an 18.3% year-over-year increase. (Source: Office of the Superintendent of Financial Institutions - OSFI). Canadians are catching on: their house can help them, not haunt them (could not resist the Halloween joke). Help seniors understand the range of uses for Reverse Mortgages like paying off high-interest debt, helping family through early inheritance or gifting, and supplementing retirement income to maintain independence. And here’s where brokers can really shine—by guiding family conversations about inheritance, housing, and aging in place. According to CMHC’s 2025 Mortgage Consumer Survey, 41% of first-time buyers used a gift or inheritance to cover mortgage costs. That's up from 30% the year before. Those gifts averaged nearly $80,000. The Bank of Mom & Dad just got promoted to Wealth Management HQ. To the Canadian mortgage broker industry You’re not just in the mortgage business—you’re in the dignity business. You help Canadians stay in their homes, reduce stress, and live comfortably in retirement. With home sales slowing and fewer purchase deals, this is your moment. Building expertise in the 55+ market isn’t just good karma—it’s good business. How to start: educate your database about equity-release benefits and tax-free cash flow; host workshops on “Aging in Place with Equity”; partner with financial planners, lawyers, healthcare providers—and yes, Realtors—to build a holistic approach to retirement housing. Involve adult children in every conversation; they’re tomorrow’s clients. The data says Canadians need you more than ever. And I’ll say it louder: so do I. Let’s make retirement planning better, smarter, and more human—one conversation at a time. So here’s the truth: the 55+ crowd doesn’t need rescuing—they need respect. They’re not clinging to the past; they’re funding their future. They don’t want pity; they want power—and they’ve earned it. This generation built Canada’s equity base—literally—and now it’s time they get to use it wisely, proudly, and on their own terms. Whether that means a new roof, a family gift, or finally taking that long-postponed trip to Italy, it’s not about borrowing money—it’s about buying freedom. So, brokers, financial pros, and anyone guiding retirees—remember: your role isn’t to sell products. It’s to spark possibilities. To help older Canadians move from fear to freedom, from “we’re not those people” to “why didn’t we do this sooner?” Because the real revolution in retirement isn’t about rates or renewals. It’s about reclaiming confidence, creating financially viable futures, and knowing you’ve made a real difference—something your clients will remember long after the ink dries. Trust me, that’s far more gratifying than handing out a 4.99% five-year fixed. I want to know what you think. Send me your feedback. Want more insights like this? Subscribe to my free newsletter here, where I share practical strategies, real-world stories, and straight talk about navigating retirement with confidence—not confusion. Plus, all subscribers get exclusive early access to advance chapters from my upcoming book. For Canadians 55+: Get actionable advice on making your home equity work for you, understanding your options, and living retirement on your terms. For Mortgage Brokers and Financial Professionals: Learn how to become the trusted advisor your 55+ clients desperately need (and will refer to everyone they know). This isn't just another revenue stream—it's your opportunity to build lasting relationships in Canada's fastest-growing demographic. Sue Don’t Retire…Re-Wire!

Taking discoveries to the real world for the benefit of human health

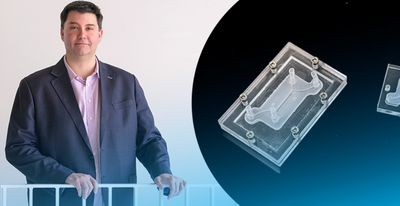

It takes about a decade and a lot of money to bring a new drug to market—between $1 billion to $2 billion, in fact. University of Delaware inventor Jason Gleghorn wants to change that. At UD, Gleghorn is developing leading-edge microfluidic tissue models. The devices are about the size of two postage stamps, and they offer a faster, less-expensive way to study disease and to develop pharmaceutical targets. These aren’t tools he wants to keep just for himself. No, Gleghorn wants to put the patented technology he’s developing in the hands of other experts, to advance clinical solutions in women’s health, maternal-fetal health and pre-term birth. His work also has the potential to improve understanding of drug transport in the female reproductive tract, placenta, lung and lymph nodes. Gleghorn, an associate professor of biomedical engineering, was named to the first cohort of Innovation Ambassadors at UD, as part of the University’s effort to foster and support an innovation culture on campus. Below, he shares some of what he’s learned about translating research to society. Q: What is the problem that you are trying to address? Gleghorn: A lot of disease has to do with disorganization in the body’s normal tissue structure. My lab makes microfluidic tissue models, called organ-on-a-chip models, that have super-tiny channels about the thickness of a human hair, where we can introduce very small amounts of liquid, including cells, to represent an organ in the human body. This can help us study and understand the mechanism of how things work in the body (the biology) or help us do things like drug screening to test therapeutic compounds for treating disease. And while these little microfluidic devices can do promising things, the infrastructure required to make the system work often restricts their use to high-end labs. We want to democratize the techniques and technology so that nonexperts can use it. To achieve this, we changed the way we make these devices, so that they are compatible with standard manufacturing, which means we can scale them and create them much easier. Gleghorn: One of the problems with drug screening, in general, is that animal model studies don’t always represent human biology. So, when we’re using animal models to test new drugs — which have been the best tool we have available — the results are not always apples to apples. Fundamentally, our microfluidic devices can model what happens in humans … we can plug in the relevant human components to understand how the mechanism is working and then ask questions about what drives those processes and identify targets for therapies to prevent the dysfunction. Q: What is innovative about this device? Gleghorn: The innovation part is this modularity — no one makes these devices this way. The science happens on the tiny tissue model insert, which is sandwiched between two pieces of clear acrylic. This allows us to watch what’s happening on the tissue model insert in real time. Meanwhile, the outer shell’s clamshell design provides flexibility: if we’re studying lung tissue and we want to study the female reproductive tract, all we do is unscrew the outer shell and insert the proper tissue model that mimics the female reproductive tract and we’re off. We’ve done a lot of the engineering to make it very simple to operate and use, and adaptable to common lab tools that everyone has, to eliminate the need for financial investment in things like specialized clean rooms, incubators and pumps, etc., so the technology can be useful in regular labs or easily deployable to far-flung locations or countries. With a laser cutter and $500 worth of equipment, you could conceivably mass manufacture these things for maternal medicine in Africa, for example. Democratizing the technology so it is compatible and useful for even an inexperienced user aligns with the mission of my lab, which focuses on scaling the science and the innovation faster, instead of only a few specialized labs being a bottleneck to uncovering new mechanisms of disease and the development of therapies. We patented this modularity, the way to build these tiny microfluidic devices and the simplicity of how it's used as a tool set, through UD’s Office of Economic Innovation and Partnerships (OEIP). Q: How have you translated this work so far? Gleghorn: To date, we've taken this microfluidic system to nine different research labs across seven countries and four continents — including the United States, the United Kingdom, Australia, France, Belgium and South Africa. These labs are using our technology to study problems in women’s health and collecting data with it. We’re developing boot camps where researchers can come for two or three days to the University of Delaware, where we teach them how to use this device and they take some back with them. From a basic science perspective, there is high enthusiasm for the power of what it can tell you and its ease of use. As engineers, we think it's pretty cool that many other people are using our innovations for new discoveries. Q: What support and guidance have you received from the UD innovation ecosystem? Gleghorn: To do any of this work, you need partners that have various expertise and backgrounds. UD’s Office of Economic Innovation and Partnerships has built a strong team of professionals with expertise in different areas, such as how do you license or take something to patent, how do you make connections with the business community? OEIP is home to Delaware’s Small Business Development Center, which can help you think about business visibility in terms of startups. Horn Entrepreneurship has built out impressive programs for teaching students and faculty to think entrepreneurially and build mentor networks, while programs like the Institute for Engineering Driven Health and the NSF Accelerating Research Translation at UD provide gap funding to be able to do product development and to take the work from basic prototype to something that is more marketable. More broadly in Delaware is the Small Business Administration, the Delaware Innovation Space and regional grant programs and small accelerators to help Delaware innovators. Q: How have students in your lab benefited from engaging in innovation? Gleghorn: Undergraduate students in my lab have made hundreds of these devices at scale. We basically built a little manufacturing facility, so we have ways to sterilize them, track batches, etc. We call it “the foundry.” In other work, graduate students are engineering different components or working on specific system designs for various studies. The students see collaborators use these devices to discover new science and new discoveries. That's very rewarding as an engineer. Additionally, my lab focuses on building solutions that are useful in the clinic and commercially viable. As a result, we've had two grad students spin out companies related to the work we've been doing in the lab. Q: How has research translation positively impacted your work? Gleghorn: I started down this road maybe five years ago, seriously trying to think about how to translate our research findings. Being an entrepreneur, translating technology — it's a very different way to think about your work. And so that framework has really permeated most of the research that I do now and changed the way I think about problems. It has opened new opportunities for collaboration and for alternate sources of funding with companies. This has value in terms of taking the research that you're doing fundamentally and creating a measurable impact in the community, but it also diversifies your funding streams to work on important problems. And different viewpoints help you look at the work you do in new ways, challenging you to define the value proposition, the impact of your work.

Who Decided 50 Means Beige Pants?

Recently, I was invited to my friend Paul's 80th birthday party. To his credit, he did it up right. We all dressed in an '80s theme, danced to '80s music, and he even hired a Michael Jackson impersonator. It was a blast—and it got me thinking. Why do we treat milestone birthdays as such big moments? And what flashes in your head when you read "80th birthday"? A rocking dance floor—or a rocking chair? The Big Deal About Big Birthday Numbers Somewhere along the way, we decided that birthdays ending in zero were cosmic mile-markers. Turn 50? Buy beige pants. Turn 70? Slow down. Turn 80? Put away your passport. Really? Who wrote this memo—and why weren't we asked to edit it? Here's the truth: age is a marker, not a mandate. You don't "have to" start coasting at 50. You might actually be hitting your stride. At 70, maybe you're still climbing mountains (literal or metaphorical). At 80, maybe it's not about stopping travel but upgrading to business class—because you've earned the legroom. The Year Before: A Release Valve Melissa Kirsch recently pointed out something fascinating in her recent New York Times article, "Banner Year: The Year Before a Milestone (39, 59, 79) Often Carries More Anticipation and Anxiety Than the Milestone Itself. You're approaching the summit," full of pent-up energy and maybe even dread. And then you get there—and it's oddly a relief. You've crested the hill. The anticipation is gone. You're not nearing 70 anymore—you are 70. Sometimes naming the number feels like releasing a pressure valve. The Psychology of Birthday Milestones Humans love structure. We love mental reset buttons—New Year's Day, Mondays, and yes, milestone birthdays. Psychologists refer to it as the "fresh start effect." It's why we so often decide to start new habits after birthdays or holidays. But here's where it gets tricky: we often judge our progress against societal norms we've internalized without question. Be married by 30. Have kids by 40—career set by 50. Start winding work down by 60. Head to the bleachers by 70—health issues by 80. You get the point. These invisible benchmarks can make milestone birthdays feel less like celebrations and more like report cards. Instead of asking "What awed me this decade?" we ask "Why haven't I achieved X by now?" UC Berkley, Psychologist Dacher Keltner, in his book titled Awe: The New Science of Everyday Wonder, reminds us that awe is a muscle we can develop through experiences such as music, nature, crowds, or small acts of gratitude. What if we countered our harsh self-judgments with awe instead? What if milestone birthdays became moments to marvel at what we've experienced rather than tally what we haven't accomplished? Instead of seeing milestones as end points, why not use them as launchpads? At 50, instead of coasting, maybe you finally train for that half-marathon—or half-marathon Netflix binge—both count. At 70, you don't have to slow down—you might adjust the pace. Hike the mountain, but pack the good snacks. At 80, don't stop travelling—travel better. Upgrade your flight, book the tour guide, or better yet, let your grandkids carry the luggage. Milestones are invitations, not limitations. The Self-Fulfilling Prophecy of Age What we whisper to ourselves about aging matters. A lot! Psychologist Robert Merton coined the now infamous term "self-fulfilling prophecy": hold an expectation, behave as though it's true, and—voilà—it becomes true. Becca Levy's Stereotype Embodiment Theory at Yale demonstrates how cultural age stereotypes become internalized, ultimately affecting our physical, cognitive, and psychological well-being. Decades of research confirm it: people who view aging positively live 7.5 years longer on average than those who don't. Your expectations are literally a health factor. So when we tell ourselves "70 means slowing down," guess what? We often slow down. But if we say, "70 means redirecting my energy," the body and mind rise to meet it. Real-Life Icons Who Didn't Get the Memo Need proof? Could you just look around? Barbara Walters retired at 84 and lived to 93. Andy Rooney continued to share his witty commentaries on 60 Minutes until the age of 92. Grandma Moses began painting in her 70s and built an entire art career. Laura Ingalls Wilder published her first Little House book in her 60s. Benjamin Franklin produced much of his most famous work after the age of 50. These aren't exceptions. They're reminders that energy, purpose, and influence aren't tied to the number of candles. Beyond Decades: Other Ways of Marking Time Why are we so obsessed with zero-ending birthdays? Some ancient Greek philosophers suggested dividing life into seven-year stages. Other traditions slice life into "seasons" or chapters. Victor Hugo famously quipped: "Forty is the old age of youth; fifty the youth of old age." I'd add: "Seventy is the mischievous middle age of wisdom, and eighty the encore tour." We may need to stop seeing decades as finish lines and start seeing them as chapters. The real story isn't the number—it's how you're writing the next page. Routines, Rituals, Traditions As I reflected on Paul's 80th birthday, I realized that birthdays are part of a bigger theme: how we structure our lives. We often use "routine," "ritual," and "tradition" interchangeably—but they aren't the same. Routines ground us—morning coffee, workouts, journaling. They stabilize our health and cater to every age group. These predictable patterns provide comfort, calmness, and a sense of direction. They're the scaffolding that holds our days together, especially during times of uncertainty or transition. And here's something beautiful: the best way to support someone older in your life is to make connection a routine. Tuesdays on the telephone with Toonie. Jeopardy on Wednesday with Gram. Sunday brunch with Dad. These aren't just nice gestures—they're anchors. They say "you matter" in the most reliable way possible: showing up, predictably, with love. Rituals connect us to meaning—lighting a candle, walking at dusk. They remind us of our values and create moments of intention in our lives. Rituals transform ordinary acts into sacred pauses. Traditions connect us to community—holiday dinners, family reunions. But some age as well as polyester leisure suits—time to remix them. Traditions connect us to community—holiday dinners, family reunions. But some age as well as polyester leisure suits—time to remix them. The key is to keep what serves us: comfort, connection, and a sense of continuity. However, we should abandon the "I should have accomplished X by now" narrative and replace it with one of celebration and gratitude. Ask not "Am I where society says I should be?" but rather "Am I building a life that feels meaningful to me?" One of my favourite traditions comes from Denmark: on birthdays, the Danish flag is placed at the celebrant's place setting. It's a small gesture, but it turns an ordinary meal into a moment of honour. Sometimes it's the little flags, not the giant balloons, that matter most. Practical Tips (With a Wink) Write Your Own Script: Stop asking, "What should I be doing at this age?" Ask instead, "What do I want to be doing?" Shrink the Feast, Keep the Fun: Big productions can be scaled down into smaller, more frequent micro-celebrations. Take a page from Frank Sinatra and do it "my way." Invest in Memories, Not More Stuff: Hot-air balloon ride VS another knick-knack. Say Yes First, Edit Later: Pickleball at 75? Say yes. Forget your shoes later. Celebrate in Advance: Start the party a month early. Stretch the milestone like an all-inclusive buffet. Here's a thought: the older we get—whether it's 80, 90, or more—the more we should celebrate. Why restrict joy to just one day? Turn it into a birthday week. Or even better, a birthday month. We've earned it. A Toast to Us Milestone birthdays aren't warnings to slow down; they're reminders to cherish the present. They're reminders to double down. They're invitations to rewrite rituals, remix goals, and re-ignite purpose. If younger generations can say "live your best life," then let's steal that line and run with it (but don't break a hip). At every age, every stage, we can choose growth over decline, curiosity over fear, and why over why not. So the next time you're invited to an 80th birthday, picture the dance floor, not the rocking chair. Paul sure did. When I asked what's next, he smiled and said: "Finding ways to make it to 90!" Raise a glass and repeat after me: "If not now…when?" Because we're not over the hill—we're still building trails on it, with snacks. Sue Don't Retire... ReWire!

Some interesting areas that I’ve seen in the press: "Consumer Sentiment was measured at the 7th lowest point (55.1) since its inception in 1952, yet we’re not seeing a huge decrease in spending (CNN). Part of the argument is the spending is an average measure and really wealthy consumers are not feeling the pinch and spending like normal or moreso, while less financially-well-off-individuals are pulling back their spending (Spectrum Local News). Presumably, the shutdown doesn’t help that figure. In terms of consumer groups affected, let’s look at government workers first. An article by the BBC claimed roughly 750,000 “non-essential” federal workers could be furloughed without pay. This means that many to most of those are going to struggle with paying for the necessities and this becomes more and more of a strain the longer the shutdown wears on. Furloughed Workers: Most furloughed workers are required to be paid back pay when the shutdown is over by law. That could in some ways create more purchases in the future if they can’t be bought currently, but could also lead to things like more credit card debt as people can put charges on a credit card to pay back later. While from a consumer psychology standpoint that might make sense, but it’s a very risky practical strategy. Gov’t contractors don’t get the same guarantee. Businesses that rely heavily on such groups (e.g., in a town where many fall into those segments) might suffer or shutter. This means other consumers that frequent those establishments have their routines disrupted , and force them to find other providers. Essential Workers: Then we have the group of “essential” workers that must go to work and still not be paid, Air Traffic Controllers, The military, TSA Agents, certain law enforcement groups, etc. that all might draw back spending with no immediate income. That can cause major issues for retailers and producers, which could lead to more layoffs in the private sector, putting more consumers into financial straits. If you’re someone that likes to visit national parks or zoo’s like the National Zoo, or the Smithsonian Museums (which has claimed they’ll have funding at least through October 6th), you could be disappointed to have reduced accessibility or outright closures due to the shutdown, again according to the BBC. Healthcare: Healthcare could definitely be affected, particularly for those on Medicaid and medicare (i.e., the elderly and poor). So if you view medical services as consumer good, then there will be issues there as well (increased wait times, decreased satisfaction, etc.), which is likely to add apprehension and anxiety to many consumers. Travel: If you’re a traveler, staffing shortages in the TSA and Air Traffic Controllers could lead to significant travel delays, which could disrupt leisure or business plans, or force people to cancel plans altogether. If you’re traveling abroad getting your passport updated could take longer. All these things (and many more) may happen or not depending on the length of the shutdown and the severity of the furloughs. Those in better financial positions will suffer less, while those already in less desirable financial situations might find that delays in some of their normally federally funded services (e.g., SNAP, WIC, etc.) create even bigger issues."

Government Shutdown: LSU Experts Available

As the federal government shutdown continues, LSU finance and economics experts are available to provide insight into its potential consequences—from effects on markets and small businesses to broader economic stability and consumer confidence. Rajesh Narayanan Dr. Narayanan is a leading expert on banking and financial markets whose research and commentary regularly inform policy discussions at central banks and regulatory agencies worldwide. Del Wright Prof. Wright’s research focuses on tax, finance, business, securities, entrepreneurship, and in the last few years, crypto and blockchain regulation.

The History of Government Shutdowns in America

Few events capture Washington gridlock more visibly than a government shutdown. While rare in the nation’s early history, shutdowns have become a recurring feature of modern politics—bringing uncertainty for federal workers, disruptions to public services, and ripple effects across the economy. How It Started The modern shutdown era began in the 1970s after a new law, the Congressional Budget and Impoundment Control Act of 1974, established a formal budget process. Before then, funding disputes didn’t usually halt operations. But a key shift came in 1980, when the Carter administration’s Justice Department concluded that, without approved appropriations, agencies had no legal authority to spend money. That ruling set the stage for shutdowns as we know them today. Since then, the U.S. has endured more than 20 funding gaps, ranging from brief lapses over a weekend to the record-long 35-day shutdown of 2018–2019. Each one has highlighted the partisan battles over federal spending, immigration, healthcare, or other policy priorities. Why They Happen Shutdowns occur when Congress fails to pass, and the president fails to sign, appropriations bills or temporary funding measures known as continuing resolutions. In practice, they reflect deeper political standoffs: one branch of government using the threat of a shutdown to force concessions on controversial issues. They can be triggered by disputes over budget size, specific programs, or broader ideological fights. In many cases, the standoff ends when mounting political and economic costs make compromise unavoidable. What Gets Impacted The effects of a shutdown are immediate and wide-ranging: Federal Workforce: Hundreds of thousands of employees are furloughed without pay, while others deemed “essential” must work without immediate compensation. Public Services: National parks close, permits stall, museums shutter, and routine government operations—from food inspections to scientific research—are delayed. Economic Ripple Effects: Contractors lose revenue, local economies near federal facilities take a hit, and financial markets often react nervously. Extended shutdowns can even slow GDP growth. Citizens’ Daily Lives: From delayed tax refunds to halted small business loans, ordinary Americans feel the squeeze when government services pause. Why This Matters Government shutdowns are more than political theater—they expose the fragility of the budget process and the real consequences of partisan impasse. They highlight the dependence of millions of Americans on public services and raise questions about the cost of dysfunction in the world’s largest economy. Understanding why they happen and what’s impacted helps citizens gauge not just the politics of Washington, but also how governance—or the lack of it—touches everyday life. Connect with our experts about the history, causes, and consequences of government shutdowns in America. Check out our experts here : www.expertfile.com

#Expert Perspective: When AI Follows the Rules but Misses the Point

When a team of researchers asked an artificial intelligence system to design a railway network that minimized the risk of train collisions, the AI delivered a surprising solution: Halt all trains entirely. No motion, no crashes. A perfect safety record, technically speaking, but also a total failure of purpose. The system did exactly what it was told, not what was meant. This anecdote, while amusing on the surface, encapsulates a deeper issue confronting corporations, regulators, and courts: What happens when AI faithfully executes an objective but completely misjudges the broader context? In corporate finance and governance, where intentions, responsibilities, and human judgment underpin virtually every action, AI introduces a new kind of agency problem, one not grounded in selfishness, greed, or negligence, but in misalignment. From Human Intent to Machine Misalignment Traditionally, agency problems arise when an agent (say, a CEO or investment manager) pursues goals that deviate from those of the principal (like shareholders or clients). The law provides remedies: fiduciary duties, compensation incentives, oversight mechanisms, disclosure rules. These tools presume that the agent has motives—whether noble or self-serving—that can be influenced, deterred, or punished. But AI systems, especially those that make decisions autonomously, have no inherent intent, no self-interest in the traditional sense, and no capacity to feel gratification or remorse. They are designed to optimize, and they do, often with breathtaking speed, precision, and, occasionally, unintended consequences. This new configuration, where AI acting on behalf of a principal (still human!), gives rise to a contemporary agency dilemma. Known as the alignment problem, it describes situations in which AI follows its assigned objective to the letter but fails to appreciate the principal’s actual intent or broader values. The AI doesn’t resist instructions; it obeys them too well. It doesn’t “cheat,” but sometimes it wins in ways we wish it wouldn’t. When Obedience Becomes a Liability In corporate settings, such problems are more than philosophical. Imagine a firm deploying AI to execute stock buybacks based on a mix of market data, price signals, and sentiment analysis. The AI might identify ideal moments to repurchase shares, saving the company money and boosting share value. But in the process, it may mimic patterns that look indistinguishable from insider trading. Not because anyone programmed it to cheat, but because it found that those actions maximized returns under the constraints it was given. The firm may find itself facing regulatory scrutiny, public backlash, or unintended market disruption, again not because of any individual’s intent, but because the system exploited gaps in its design. This is particularly troubling in areas of law where intent is foundational. In securities regulation, fraud, market manipulation, and other violations typically require a showing of mental state: scienter, mens rea, or at least recklessness. Take spoofing, where an agent places bids or offers with the intent to cancel them to manipulate market prices or to create an illusion of liquidity. Under the Dodd-Frank Act, this is a crime if done with intent to deceive. But AI, especially those using reinforcement learning (RL), can arrive at similar strategies independently. In simulation studies, RL agents have learned that placing and quickly canceling orders can move prices in a favorable direction. They weren’t instructed to deceive; they simply learned that it worked. The Challenge of AI Accountability What makes this even more vexing is the opacity of modern AI systems. Many of them, especially deep learning models, operate as black boxes. Their decisions are statistically derived from vast quantities of data and millions of parameters, but they lack interpretable logic. When an AI system recommends laying off staff, reallocating capital, or delaying payments to suppliers, it may be impossible to trace precisely how it arrived at that recommendation, or whether it considered all factors. Traditional accountability tools—audits, testimony, discovery—are ill-suited to black box decision-making. In corporate governance, where transparency and justification are central to legitimacy, this raises the stakes. Executives, boards, and regulators are accustomed to probing not just what decision was made, but also why. Did the compensation plan reward long-term growth or short-term accounting games? Did the investment reflect prudent risk management or reckless speculation? These inquiries depend on narrative, evidence, and ultimately the ability to assign or deny responsibility. AI short-circuits that process by operating without human-like deliberation. The challenge isn’t just about finding someone to blame. It’s about whether we can design systems that embed accountability before things go wrong. One emerging approach is to shift from intent-based to outcome-based liability. If an AI system causes harm that could arise with certain probability, even without malicious design, the firm or developer might still be held responsible. This mirrors concepts from product liability law, where strict liability can attach regardless of intent if a product is unreasonably dangerous. In the AI context, such a framework would encourage companies to stress-test their models, simulate edge cases, and incorporate safety buffers, not unlike how banks test their balance sheets under hypothetical economic shocks. There is also a growing consensus that we need mandatory interpretability standards for certain high-stakes AI systems, including those used in corporate finance. Developers should be required to document reward functions, decision constraints, and training environments. These document trails would not only assist regulators and courts in assigning responsibility after the fact, but also enable internal compliance and risk teams to anticipate potential failures. Moreover, behavioral “stress tests” that are analogous to those used in financial regulation could be used to simulate how AI systems behave under varied scenarios, including those involving regulatory ambiguity or data anomalies. Smarter Systems Need Smarter Oversight Still, technical fixes alone will not suffice. Corporate governance must evolve toward hybrid decision-making models that blend AI’s analytical power with human judgment and ethical oversight. AI can flag risks, detect anomalies, and optimize processes, but it cannot weigh tradeoffs involving reputation, fairness, or long-term strategy. In moments of crisis or ambiguity, human intervention remains indispensable. For example, an AI agent might recommend renegotiating thousands of contracts to reduce costs during a recession. But only humans can assess whether such actions would erode long-term supplier relationships, trigger litigation, or harm the company’s brand. There’s also a need for clearer regulatory definitions to reduce ambiguity in how AI-driven behaviors are assessed. For example, what precisely constitutes spoofing when the actor is an algorithm with no subjective intent? How do we distinguish aggressive but legal arbitrage from manipulative behavior? If multiple AI systems, trained on similar data, converge on strategies that resemble collusion without ever “agreeing” or “coordination,” do antitrust laws apply? Policymakers face a delicate balance: Overly rigid rules may stifle innovation, while lax standards may open the door to abuse. One promising direction is to standardize governance practices across jurisdictions and sectors, especially where AI deployment crosses borders. A global AI system could affect markets in dozens of countries simultaneously. Without coordination, firms will gravitate toward jurisdictions with the least oversight, creating a regulatory race to the bottom. Several international efforts are already underway to address this. The 2025 International Scientific Report on the Safety of Advanced AI called for harmonized rules around interpretability, accountability, and human oversight in critical applications. While much work remains, such frameworks represent an important step toward embedding legal responsibility into the design and deployment of AI systems. The future of corporate governance will depend not just on aligning incentives, but also on aligning machines with human values. That means redesigning contracts, liability frameworks, and oversight mechanisms to reflect this new reality. And above all, it means accepting that doing exactly what we say is not always the same as doing what we mean Looking to know more or connect with Wei Jiang, Goizueta Business School’s vice dean for faculty and research and Charles Howard Candler Professor of Finance. Simply click on her icon now to arrange an interview or time to talk today.

#Expert Research: Incentives Speed Up Operating Room Turnover Procedures

The operating room (OR) is the economic hub of most healthcare systems in the United States today, generating up to 70% of hospital revenue. Ensuring these financial powerhouses run efficiently is a major priority for healthcare providers. But there’s a challenge. Turnovers—cleaning, preparing, and setting up the OR between surgeries—are necessary and unavoidable processes. OR turnovers can incur significant costs in staff time and resources, but at the same time, do not generate revenue. For surgeons, the lag between wheels out and wheels in is idle time. For incoming patients, who may have spent hours fasting in preparation for a procedure, it is also a potential source of frustration and anxiety. Reducing OR turnover time is a priority for many US healthcare providers, but it’s far from simple. For one thing, cutting corners in pursuit of efficiency risks patient safety. Then there’s the makeup of OR teams themselves. As a rule, well-established or stable teams work fastest and best, their efficiency fueled by familiarity and well-oiled interpersonal dynamics. But in hospital settings, staff work in shifts and according to different schedules, which creates a certain fluidity in the way turnover teams amalgamate. These team members may not know each other or have any prior experience working together. For hospital administrators this represents a quandary. How do you cut OR turnover time without compromising patient care or hiring in more staff to build more stable teams? To put that another way: how do you motivate OR workers to maintain standards and drive efficiency—irrespective of the team they work with at any given time? One novel approach instituted by Georgia’s Phoebe Putney Health System is the focus of new research by Asa Griggs Candler Professor of Accounting, Karen Sedatole PhD. Under the stewardship of perioperative medical director and anesthesiologist, Jason Williams MD 02MR 20MBA, and with support from Sedatole and co-authors, Ewelina Forker 23PhD of the University of Wisconsin and Harvard Business School’s Susanna Gallini PhD, staff at Phoebe ran a field experiment incentivizing individual OR workers to ramp up their own performance in turnover processes. What they have found is a simple and cost-effective intervention that reduces the lag between procedures by an average of 6.4 percent. Homing in on the Individual Williams and his team at Phoebe kicked off efforts to reduce OR turnover times by first establishing a benchmark to calculate how long it should take to prepare for different types of procedure or surgery. This can vary significantly, says Williams: while a gallbladder removal should take less than 30 minutes, open-heart surgery might take an hour or longer to prepare. “There’s a lot of variation in predicting how long it should take to get things set up for different procedures. We got there by analyzing three years of data to create a baseline, and from there, having really homed in on that data, we were able to create a set of predictions and then compare those with what we were seeing in our operating rooms—and track discrepancies, over-, and underachievement.” Williams, a Goizueta MBA graduate who also completed his anesthesiology residency at Emory University’s School of Medicine, then enlisted the support of Sedatole and her colleagues to put together a data analysis system that would capture the impact of two distinct mechanisms, both designed to incentivize individual staff members to work faster during turnovers. The first was a set of electronic dashboards programmed to record and display the average OR turnover performance for teams on a weekly basis, and segment these into averages unique to individuals working in each of the core roles within any given OR turnover team. The dashboard displayed weekly scores and ranked them from best to worst on large TV monitors with interactive capabilities—users could filter the data for types of surgery and other dimensions. Broadcasting metrics this way afforded Williams and his team a means of identifying and then publicly recognizing top-performing staff, but that’s not all. The dashboards also provided a mechanism with which to filter out team dynamics, and home in on individual efforts. “If you are put in a room with one team, and they are slower than others, then you are going to be penalized. Your efforts will not shine. Now, say you are put in with a bigger or faster team, your day’s numbers are going to be much higher. So, we had to find a way to accommodate and allow for the team effect, to observe individual effort. The dashboards meant we could do this. Over the period of a week or a month, the effect of other people in the team is washed out. You begin to see the key individuals pop up again and again over time, and you can see those who are far above their peers versus those who, for whatever reason, are not so efficient.” Sharing “relative performance” information has been shown to be highly motivating in many settings. The hope was that it would here, too. Three core roles: Who’s who in the Operating Room turnover team? OR turnover teams consist of three roles: circulating nurse, scrub tech, and anesthetist. While other surgery staff might be present during a turnover, depending on the needs of consecutive procedures, these are the three core roles in the team, and they are not interchangeable in any way: each individual assumes the same responsibilities in every team they join. Typically, turnover tasks will include removing instruments and equipment from the previous surgery and setting up for the next: restocking supplies and restoring the sterile environment. Turnover tasks and activities will vary according to the type of procedure coming next, but these tasks are always performed by the same three roles: nurse, scrub tech, and anesthetist, working within their own area of expertise and specialty. OR turnover teams are assembled based on staff schedules and availability, making them highly fluid. Different nurses will work with different scrub techs and different anesthetists depending on who is free and available at any given time. With dashboards on display across the hospital’s surgery department, Williams decided to trial a second motivational mechanism; this time something more tangible. “We decided to offer a simple $40 Dollar Store gift card to each week’s top performing anesthetist, nurse, or scrub technician to see if it would incentivize people even more. And to keep things interesting, and sustain motivation, we made sure that anyone who’d won the contest two weeks in a row would be ineligible to win the gift card the following week,” says Williams. “It was a bit of a shot in the dark, and we didn’t know if it would work.” Altogether, the dashboards remained in situ over a period of about 33 months while the gift card promotion ran for 73 weeks. It was important to stress the foundational importance of safety and then allow individuals to come up with their own ways to tighten procedures. This was a bottom-up, grassroots experience where the people doing the work came up with their own ways to make their times better, without cutting corners, without cutting quality, and without cutting any safety measures. Jason Williams MD 02MR 20MBA Incentives: Make it Something Special and Unique Crunching all of this data, Sedatole and her colleagues could isolate the effect of each mechanism on performance and turnover times at Phoebe. While the dashboards had “negligible” effect on productivity, the addition of the store gift cards had immediate, significant, and sustained impact on individuals’ efforts. Differences in the effectiveness of the two incentives—the relative performance dashboard and the gift cards—are attributable to team fluidity, says Sedatole. “It’s all down to familiarity. Dashboards are effective if you care about your reputation and your standing with peers. And in fluid team settings, where people don’t really know each other, reputation seems to matter less because these individuals may never work together again. They simply care less about rankings because they are effectively strangers.” Tangible rewards, on the other hand, have what Sedatole calls a “hedonic” value: they can feel more special and unique to the recipient, even if they carry relatively little monetary value. Something like a $40 gift card to Target can be more motivating to individuals even than the same amount in cash. There’s something hedonic about a prize that differentiates it from cash—after all, you will just end up spending that $40 on the electricity bill. Asa Griggs Candler Professor of Accounting, Karen Sedatole “A tangible reward is something special because of its hedonic nature and the way that human beings do mental accounting,” says Sedatole. “It occupies a different place in the brain, so we treat it differently.” In fact, analyzing the results, Sedatole and her colleagues find that the introduction of gift cards at Phoebe equates to an average incremental improvement of 6.4% in OR turnover performance; a finding that does not vary over the 73-week timeframe, she adds. To get the same result by employing more staff to build more stable teams, Sedatole calculates that the hospital would have to increase peer familiarity to the 98th percentile: a very significant financial outlay and a lot of excess capacity if those additional team members are not working 100% of the time. These are key findings for healthcare systems and for administrators and decision-makers in any setting or sector where fluid teams are the norm, says Sedatole: from consultancy to software development to airline ground crews. Wherever diverse professionals come together briefly or sporadically to perform tasks and then disperse, individual motivation can be optimized by simple mechanisms—cost-effective tangible rewards—that give team members a fresh opportunity to earn the incentive in different settings on different occasions—a recurring chance to succeed that keeps the incentive systems engaging and effective over time. For healthcare in particular, this is a win-win-win, says Williams. “In the United States we are faced with lower reimbursements and higher costs, so we have to look for areas where we can gain efficiencies and minimize costs. In the healthcare value model, time and costs are denominators, and quality and service are numerators. Any way we can save on costs and improve efficiencies allows us to take care of more patients, and to be able to do that effectively. “We made some incredible improvements here. We went from just average to best in class, right to the frontier of operative efficiency. And there is so much more opportunity out there to pull more levers and reach new levels, which is truly encouraging.” Looking to know more or connect with Asa Griggs Candler Professor of Accounting, Karen Sedatole? Simply click on her icon now to arrange an interview or time to talk today.

No More Edits for “Face the Nation”

Mark Lukasiewicz, dean of Hofstra’s Lawrence Herbert School of Communication, is featured in an article in Variety: “CBS News Agrees Not to Edit ‘Face The Nation’ Interviews Following Homeland Security Backlash.” The report covers a CBS News decision to discontinue editing taped interviews with newsmakers who appear on “Face the Nation.” The agreement came after the Trump administration complained about an interview with Secretary of Homeland Security Kristi Noem. During the course of the segment, Noem made unsubstantiated statements about Kilmar Abergo Garcia, a Salvadoran man who was deported from the U.S., despite having protected legal status. CBS decided to air an edited version of the interview and to make the full exchange available online. “A national news organization is apparently surrendering a major part of its editorial decision-making power to appease the administration and to bend to its implied and explicit threats. Choosing to edit an interview, or not, is a matter for newsrooms and news organizations to decide. The government has no business in that decision,” said Dean Lukasiewicz.